- Weak steel margins cap upside, keep market range-bound

- Australian premium hard coking coal rises by $3/t w-o-w

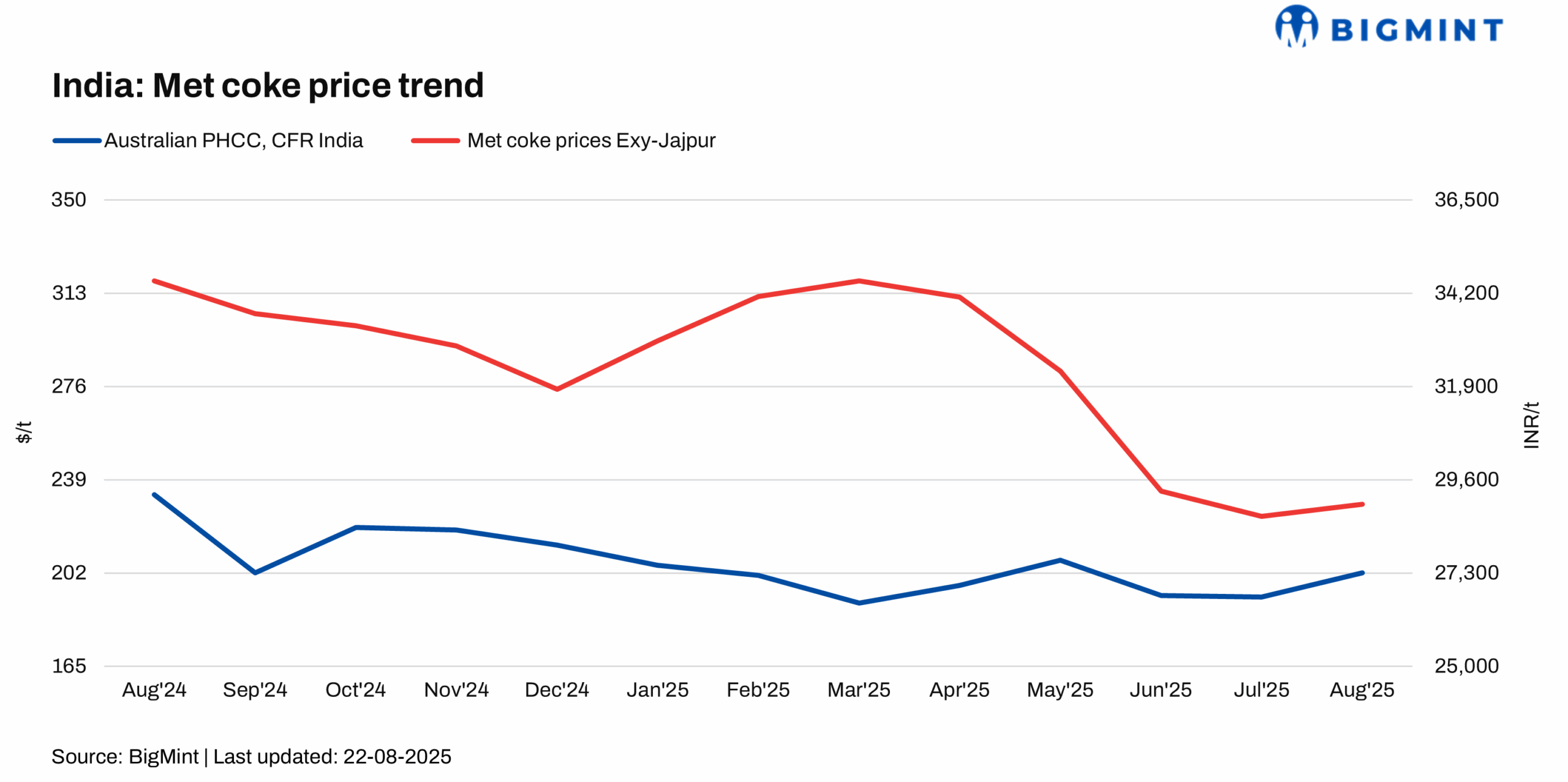

The Indian metallurgical coke (met coke) market remained stable w-o-w during the week ending 22 August 2025, supported by constrained domestic availability and firm input costs.

In eastern India, BF-grade (25-90 mm) met coke was assessed at INR 29,000/tonne (t) ex-Jajpur, while in western India, ex-works Gandhidham prices held at INR 30,000/t.

Market activity was largely steady, with trades beginning to pick up as consumers sought to secure volumes in expectations of limited supply in the near term.

Supply constraints, firm coal costs provide support

Tight domestic supply, coupled with delays in import arrivals, continued to underpin market stability. Indian buyers were cautious but had little room to push prices lower, given limited spot availability. On the cost side, firm coking coal prices added further support. Australian premium hard coking coal rose by $3/t w-o-w to $188/t, reflecting sustained demand in seaborne markets and reinforcing cost pressures for Indian coke producers.

China’s market dynamics influence sentiment

Regional sentiment was also shaped by developments in China, the world’s largest coke consumer. On 20 August, Chinese producers attempted to implement a seventh consecutive round of price hikes, but steel mills showed resistance amid stable supply, adequate inventories, and weak finished steel margins.

Demand for coke remained underpinned by steady molten iron output, though procurement stayed cautious. Meanwhile, coking coal markets in China displayed mixed trends: gas coal prices in Shaanxi softened on weak buying, while a mine accident in Shanxi curtailed high-sulphur coal output, tightening supply and lending localised price support.

Pig iron market shows weakness

In contrast, India’s pig iron market registered mild weakness. Steel-grade pig iron ex-Durgapur dropped by INR 200/t w-o-w to INR 32,500/t. The decline was attributed to tepid demand from steelmakers, who remained under pressure from falling finished steel prices and cautious end-user demand. This weakness highlighted the difficulty for mills to absorb additional raw material cost increases, limiting the upward potential for coke prices.

Outlook

The Indian met coke market is likely to stay range-bound in the near term, supported by firm coking coal costs and tight domestic supply. Improving trade activity could provide mild strength, but weak pig iron and steel margins, alongside mill resistance to higher costs, limit upside. Market direction will depend on coal price trends, import arrivals, and steel demand, with upside possible if coal prices stay firm or imports face delays, and downside if supply eases or costs soften.

Leave a Reply