- Festive demand likely to lift finished segment

- Ferro molybdenum surges on supply shortages

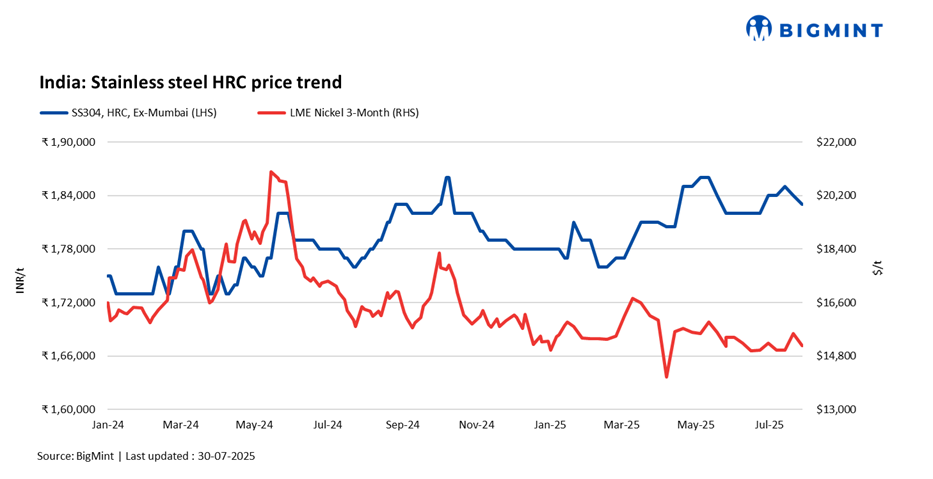

India’s stainless steel market witnessed fluctuations this week, with finished flats showing mixed price movements and longs remaining range-bound w-o-w, amid limited trading activity.

BigMint’s benchmark assessment for 304 series hot-rolled coils (HRCs) dropped marginally by INR 1,000/tonne (t) w-o-w to INR 183,000/t ex-Mumbai. Meanwhile, 304L black round bars (25-100 mm) inched up to INR 157,000/t w-o-w, amid weak buying activity.

BigMint’s assessment for SS 316 HRCs stood at INR 330,000/t and for 316 cold-rolled coils (CRCs) at INR 334,000/t ex-Mumbai, both steady w-o-w.

Market updates

According to participants, the Indian market showed some signs of positivity amid the approaching festive season. Consequently, demand is likely to pick up for finished products.

However, the market remained cautious about rising molybdenum prices, a key raw material for the 316 grade, which is expected to lift prices.

European stainless steel 304 CRC NW was heard traded at $2,710-2,775/t, while 316 CRC NW was heard at $4,330-4,550/t.

The European stainless steel market was also subdued due to cautious sentiment this week (end of July 2025). This could be attributed to a typical summer lull. Prices continued to show weakness due to low end-user demand, especially in construction and consumer goods, and ongoing heavy import competition.

LME nickel drops, Asian NPI flat w-o-w

At the time of reporting, three-month nickel prices on the London Metal Exchange (LME) stood at $15,145/t, down by 3% w-o-w. Nickel stocks in LME-registered warehouses stood at 204,912 t, down slightly compared to 206,580 t in the previous week.

Chinese portside prices of nickel pig iron (NPI) (grade 13%>Ni>10%) remained firm w-o-w at RMB 917/t ($128/t). Meanwhile, Indonesian FOB prices of NPI (grade 13%>Ni>10%) stood at $109/t, steady w-o-w.

Chinese stainless steel prices steady

In China, prices of domestic stainless steel 304-grade CRCs stood at RMB 13,450/t ($1,873/t) exw, stable w-o-w, while FOB tags of 304-grade CRCs were firm at $1,910/t.

Prices in late July were stable overall, with small gains from hikes by mills tempered by weak downstream demand and ongoing market oversupply. This kept any meaningful price recovery in check.

As August approaches, the stainless steel market showed signs of bottoming out. This steady trend was supported by rising stainless steel futures in China, firmer global nickel prices, and higher export offers from Indonesia’s Tsingshan. Buyer sentiment began to improve, leading to increased restocking, while government support measures, production cuts, and higher mill prices all contributed to market stability. If these positive trends continue, especially with robust futures and nickel markets, further price increases are possible in the near term.

Raw material scenario

Ferro molybdenum: Indian ferro molybdenum prices witnessed an increase of INR 80,000/t ($916/t) as compared to the previous assessment on 23 July. Prices increased to over a two-year high due to the tight supply of molybdenum oxide and robust demand globally.

As per BigMint’s assessment on 30 July, ferro molybdenum prices were at INR 2,980,000/t ($34,137/t) exw-India. Deals for around 55 t were heard by BigMint last week in the price range of INR 2,750,000-3,000,000/t ($31,502-34,366/t) exw. Similar prices were last seen in September 2023, as per data maintained by BigMint.

Molybdenum oxide, a key raw material of ferro molybdenum, was available in limited quantities in the domestic market. As a result, sellers lifted ferro molybdenum offers to around INR 3,000,000/t ($34,366/t) exw.

Ferro silicon: Indian ferro silicon (70%) prices witnessed a hike of INR 11,700/t ($135/t) in comparison to the previous assessment on 21 July. Prices rose sharply, as offers from sellers increased amid the news of electricity supply cuts to Meghalaya plants and the rise in imported silicon metal prices from China.

As per BigMint’s assessment on 28 July, ferro silicon prices in India were at INR 97,400/t ($1,122/t) exw-Guwahati. In Bhutan, prices surged by INR 12,100/t ($139/t) w-o-w to INR 98,400/t ($1,134/t) exw.

Ferro chrome: Indian high-carbon ferro chrome (HC60%, Si:4%) prices were at INR 99,700/t ($1,137/t) exw-Jajpur, range-bound w-o-w.

Ferrous scrap: India’s imported scrap market showed signs of improvement in the past 2-3 days. UK-origin shredded was offered at $365-370/t CFR Nhava Sheva, while fresh EU-origin shredded offers stood at $370-375/t. UK-origin HMS was quoted at $340-345/t.

Firming iron ore and sponge iron prices boosted sentiment in the scrap market. Expectations of iron ore price hikes and rising coal costs could lift August steel prices, with the impact likely extending to the scrap market.

Outlook

India’s stainless steel market is expected to pick up in the upcoming month, with the monsoon departing and the festive season set to commence. Consequently, demand and sales will pick up in the upcoming months.

Leave a Reply