- Bid-offer disparity prevents pellet export deals

- Market awaits China’s Politburo meeting outcome

Indian pellet export prices witnessed a decline this week, mirroring the fall in global iron ore prices and growing uncertainty surrounding the outcome of the Chinese Politburo meeting. Market participants report sluggish export activity, with deals stalling due to a widening bid-offer gap, leaving most Indian pellet producers to pivot toward the domestic market, where margins remain more attractive.

Price update

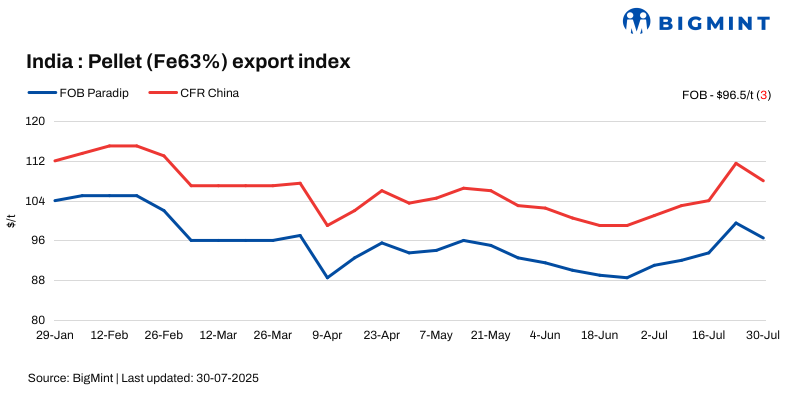

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index (FOB east coast) fell by $3/tonne (t) w-o-w to $96.5/t on 30 July 2025 against 23 July. Notably, no confirmed pellet export deal was reported from India’s eastern coast this week.

Meanwhile, a few sources mentioned that around 75,000 tons of pellet export deals were concluded from Odisha in mid-July. The cargo was booked by South Korean buyers, but the trade could not be confirmed by the transacted parties.

An India-based pellet maker concluded an export deal for 50,000 t of material (Fe63%, Al2O3+SiO2: 8%) through a tender scheduled at the end of last week. The deal was heard concluded at $109-109.5/t FOB India, as per sources.

Market comments

A pellet supplier based in eastern India remarked, “Domestic prices are currently better in terms of realisations. We are managing to conclude deals in selective pockets, tailored to buyers’ requirements.”

Another producer said, “The export target of $115/t CFR China is still distant from current achievable prices. Some bulk domestic tenders are offering relatively stable and lucrative margins, hence the preference shift.”

Meanwhile, despite sluggish export deals, Indian low-alumina pellet tenders continue to receive a decent response in the seaborne market. However, Chinese mills are also exploring alternative high-grade, low-alumina pellet options from other global suppliers, adding pressure on Indian exporters.

The market remains in a wait-and-watch mode. Exporters and traders are hopeful that prices may improve post the Chinese Politburo meeting, which is expected to provide clearer direction for the country’s economic and industrial policy. Historically, announcements from the Politburo regarding stimulus or infrastructure investment have had a direct impact on steel demand, thereby influencing raw material imports.

Until then, the likelihood of export deals materializing from India’s east coast remains limited, with producers favouring domestic sales to maintain profitability amidst global uncertainties.

Domestic vs export gap widens

Domestic prices exceeded export offers by around INR 1,800/t ($21/t), widening by INR 500-600/t with a rise in domestic and fall in export prices. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8.250/t ($94/t) exw, rising INR 350/t ($4/t) w-o-w. Meanwhile, the ex-plant realisation in exports from Barbil was firm w-o-w at INR 6,450/t ($74/t) exw.

Rationale

- No confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was not taken into consideration for today’s price calculations and accorded 0% weightage in the index calculation. Click here for the detailed methodology.

- Twelve (12) indicative prices were received, and eight (8) were considered for the calculation of the index and given 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices fall w-o-w: The benchmark iron ore fines index dropped $3/t w-o-w at $102/t CFR China on 29 July. The decline occurred ahead of the forthcoming Politburo meeting, as fresh trades focused on medium-grade fines. Market attention is now on the potential for new stimulus policies. Chinese port-stock iron prices dropped too, attributed to a cooling off of last week’s positive market sentiment.

DCE iron ore futures down w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract decreased by RMB 25.5/t ($4/t) w-o-w to RMB 789/t ($110/t) on 30 July.

Outlook

According to BigMint’s analysis, exporters may look forward to newer opportunities in the coming days following key Chinese policy-related meetings.

Leave a Reply