- 15% country cap lifting to benefit UK, Turkiye, Korea

- India put in “pooled category”, with mere 12,555 t

The European Union has formally notified the World Trade Organization (WTO) of proposed adjustments to its safeguard measures on certain steel products, in a significant shift in its import policy, particularly for items like angles, shapes and sections of iron or non-alloy steel (Category 17). The proposed changes, aimed at preserving traditional trade flows and addressing unintended consequences, are slated to take effect on 1 July 2025.

The notification, circulated on 11 June 2025, outlines a “Correcting Act” that will primarily impact Category 17, a segment that saw its quotas “globalised” in 2022 following Russia’s invasion of Ukraine. This globalisation had merged country-specific quotas for the UK, Türkiye, and Korea with a residual quota, creating a single quota for all origins.

The recent functioning review of the measure had introduced a 15% cap on the share of the overall volume that could be provided by any single exporting country in Category 17. However, the European Commission has acknowledged that this cap has inadvertently restricted traditional trade for certain partners, pushing their duty-free access below historical levels.

Key proposed adjustments:

- Removal of 15% country-cap in Category 17: The most impactful change is the proposed removal of the 15% country-cap for Category 17, effective 1 July 2025. This move is intended to safeguard the historical trade relationships of key exporting partners.

- Reinstatement of Country-Specific Quotas: To prevent undue crowding out of traditional suppliers while preserving historical trade, the EU plans to re-introduce country-specific quotas for the United Kingdom, Türkiye, and Korea.

- Reinstatement of residual quota: Concurrently, the residual quota will be reinstated. Notably, no cap will apply to this residual quota.

- Limited access to residual quota: Country-specific quota holders will not have access to the residual quota during the last quarter of a safeguard year.

- Correction of inaccuracies: The notification also addresses minor technical corrections, including the removal of a cap in Category 4B and a correction to footnote 2 in Annex IV.1.

The duration of the overall safeguard measure remains unchanged, extending until 30 June 2026, with a continued progressive liberalization rate of 0.1% yearly.

The European Union has extended an invitation for consultations with WTO Members having a substantial interest as exporters of the product concerned. These consultations are scheduled to take place virtually or in person in Brussels from 12 June to 19 June 2025. The main exporting countries directly impacted by these adjustments are the United Kingdom, Türkiye, and Korea.

Impact on India:

India, along with countries like China and Vietnam, will share a limited import quota of just 12,555 t (tonnes), beyond which a 25% safeguard duty will be levied. This move, despite the EU’s claims of rectifying quota imbalances, effectively relegates India to a “second-tier access regime” without dedicated duty-free quotas, unlike major exporters such as Ukraine, UK, Türkiye, and South Korea, which are benefiting from the re-introduction of country-specific quotas.

This decision poses a significant challenge for Indian steel exporters, as it risks rapid quota exhaustion due to competition from larger exporters in the pooled category. It also raises concerns about potential discriminatory trade policy, particularly as India and the EU are in the final stages of Free Trade Agreement (FTA) negotiations, where such unilateral restrictive measures could erode mutual trust. India is expected to engage in immediate diplomatic consultations and push for binding commitments on non-discriminatory treatment within the FTA, advocating for the reinstatement of country-specific quotas and exploring WTO dispute settlement options as a last resort.

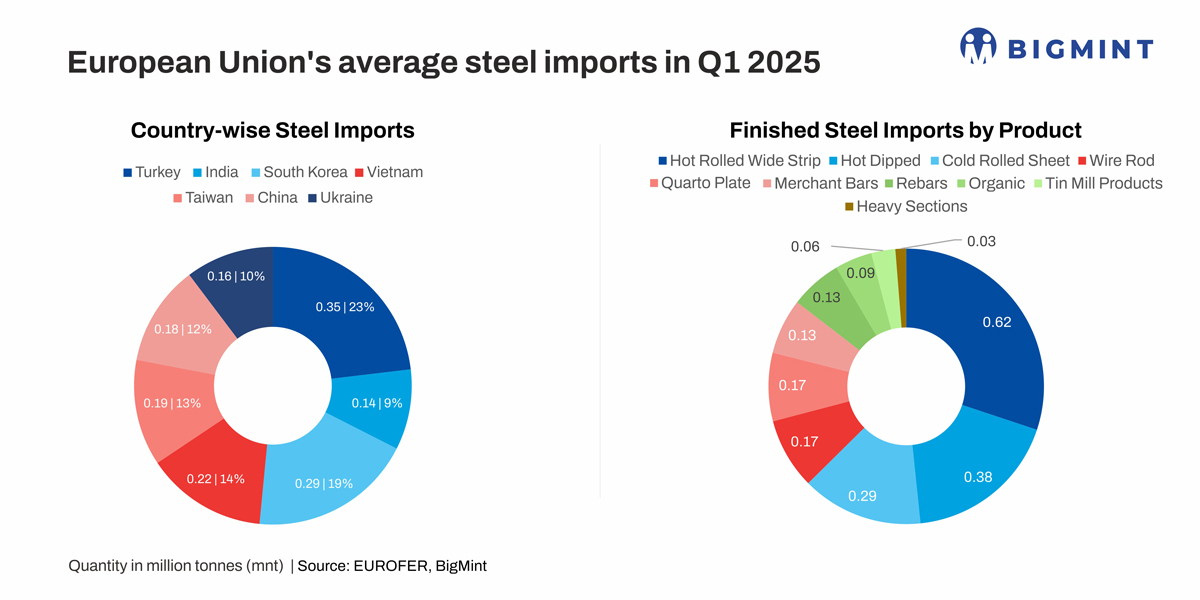

EU’s steel imports show mixed trends in Q1, 2025

In Q1 2025, total steel imports (including semis) into the EU decreased by 9% y-o-y. Imports of finished products slightly decreased by 1%, with flat products declining by 4%, while long products saw an increase of 7%.

During the same period, the main countries of origin for finished steel imports were Turkiye (16.4% share), South Korea (13.5%), Vietnam (10%), Taiwan (8.8%), and China (8.3%), collectively accounting for 87% of total arrivals.

While imports of finished products recorded the sharpest increase from China (+42%), they also surged from South Korea (+28%), Turkiye (+20%), and Vietnam (+14%). In contrast, imports of finished products plunged from India (-56%), Japan (-39%), and Taiwan (-3%).

Within the flat product segment, imports of most products increased, with the exception of hot-rolled wide strip (-25%). Notably, imports of hot dipped (+5%), coated sheets (+9%), organic (+24%), cold rolled sheets (+26%), and quarto plate (+17%) all rose. For long products, imports decreased for wire rods (-22%), but increased for rebars (+21%), heavy sections (+42%), and particularly merchant bars (+61%).

Outlook

The recent adjustments by the European Union to its steel safeguard measures, aimed at fine-tuning import policies and protecting traditional trade flows for specific nations like the UK, Türkiye, and Korea, present a challenging outlook for India. By reinstating country-specific quotas for these major players and removing the 15% country-cap in Category 17, the EU is effectively prioritizing certain trade relationships.

Meanwhile, India finds itself in a ‘pooled quota’ with other nations, facing a significantly limited duty-free volume before a 25% safeguard duty kicks in. This ‘second-tier’ treatment, coupled with the ongoing India-EU FTA negotiations, necessitates a robust diplomatic response from India to safeguard its steel exports, ensure a level playing field, and prevent the erosion of mutual trust, while simultaneously exploring market diversification.

Leave a Reply