- BF rebar tags drop, HRCs stable w-o-w

- Billet prices decline by up to INR 900/t

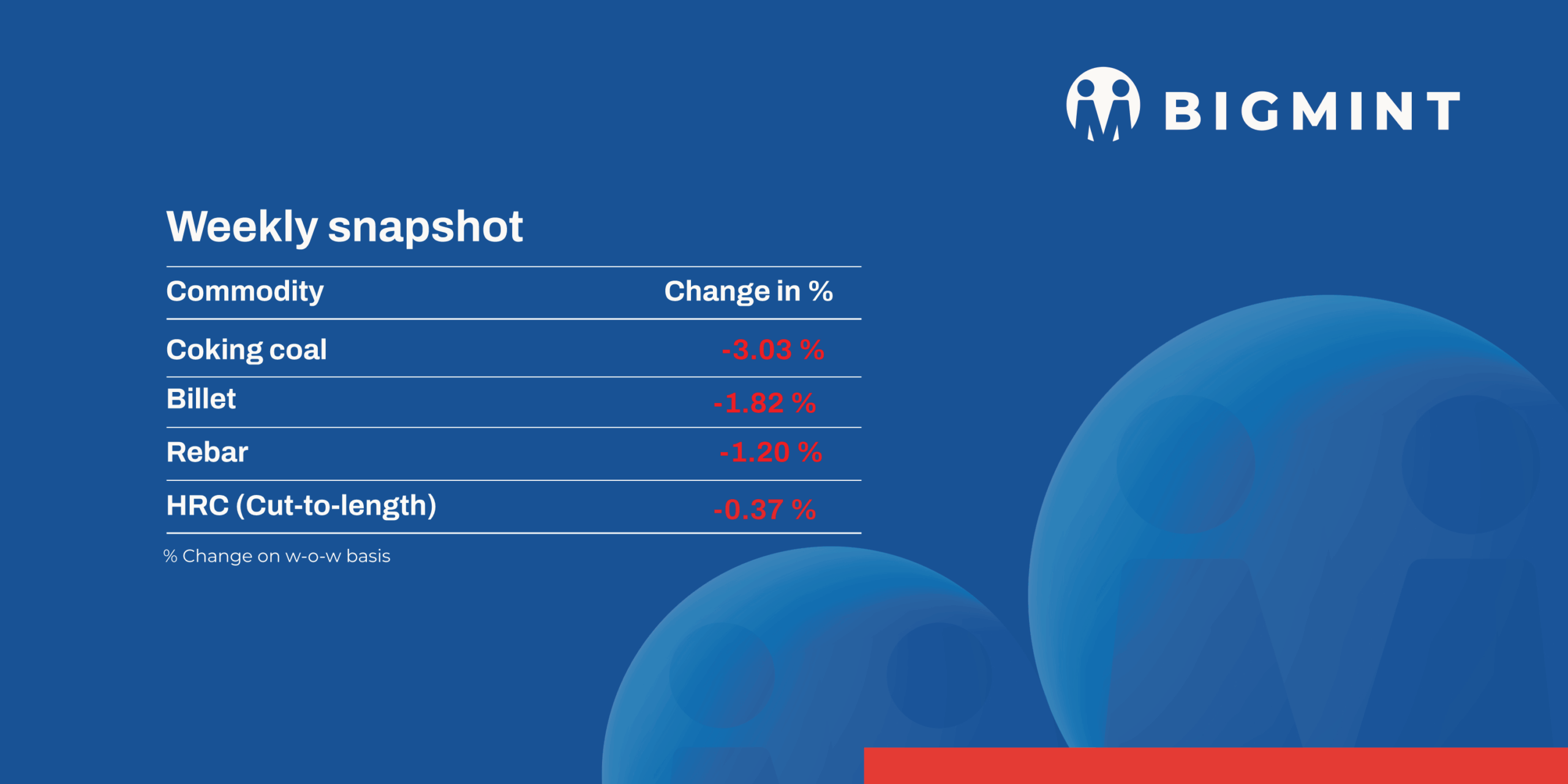

The domestic steel and raw material markets remained under pressure this week, with weak demand dragging down prices in various segments. Among finished steel, while price tags of induction furnace (IF) route finished longs decreased by INR 200-1,200/tonne (t) w-o-w, trade reference values for hot-rolled coils (HRCs) were stable in most markets.

Iron ore, pellets

- BigMint’s bi-weekly domestic pellet (Fe63%) index inched down by INR 50/t w-o-w to INR 9,200/t ($108/t) DAP Raipur on 13 June. Raipur-based pellet producers kept offers for Fe 62/63% (+/- 0.5%) at INR 9,000-9,100/t ($105-106/t) exw. Trades for around 40,000 t took place this week in the Raipur region by local suppliers.

- In NMDC Chhattisgarh’s auction on 13 June, 4,000-t Baila-sized lumps (10-20 mm, Fe 65.5%) were sold at the base price of INR 6,500/t; 21,500-t DRCLO (10-40 mm, Fe 67%) and 86,000-t fines (Fe 64%) received no bids. Prices were on FOR basis, inclusive of royalty, DMF, and NMET.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched up by $1/t w-o-w to $60/t FOB east coast on 12 June. The increase in prices was boosted by decent buying interest from market participants. Deals for around 165,000 t of Fe 56-57% fines were concluded at $70-72/t CFR China in this publishing window, while a deal for 80,000 t of Fe 54% fines was closed on the eastern coast.

Coal

- South African thermal coal prices at Indian ports declined again this week due to weak demand, better domestic availability, and freight pressure from rising crude oil prices. RB2 (5500 NAR) fell by INR 100/t w-o-w to INR 7,700/t at Gangavaram, while RB3 (4800 NAR) dropped by INR 50/t to INR 6,800/t. At Vizag, RB2 was assessed at INR 7,650/t and RB3 at INR 6,650/t. Around 55,000 t of RB2 were traded at INR 7,450-7,600/t at Dhamra and Gangavaram. Port stocks were steady w-o-w at 15.35 mnt. The decline came amid falling sponge iron prices and sluggish billet and steel market trends.

- Domestic coal prices were under pressure this week, as demand remained weak and availability was sufficient. According to BigMint’s assessment, 5000 GCV grade coal prices dropped by INR 50/t to INR 4,700/t ex-Bilaspur, while the 4500 GCV grade held firm at INR 4,250/t. Recent SECL auctions saw lower bids, indicating limited interest from buyers amid ongoing market sluggishness.

- Met coke prices in India dropped sharply this week, with the blast furnace grade down INR 1,300/t to INR 29,500/t ex-Jajpur – the lowest in five years. In western India’s Gandhidham, prices also fell INR 1,100/t to INR 29,500/t, marking a five-month low. Sluggish steel demand, falling pig iron prices, and reduced procurement weakened sentiment. Regulatory uncertainty regarding quota restrictions and anti-dumping duties further added to market caution. Meanwhile, China saw its third consecutive met coke price cut due to high inventories and poor demand. Prices are likely to stay weak, especially during the monsoon slowdown.

Ferrous scrap

- India’s imported scrap market remained sluggish throughout the week due to falling steel prices, monsoon disruptions, and the availability of cheaper domestic alternatives. UK shredded fell by 1% w-o-w to $361/t CFR, with most tradable levels at $355-360/t. HMS 80:20 offers from West Africa and Brazil drew limited interest, as buyers held bids below $340/t CFR.

- Weak steel demand, especially in the rebar segment with prices at multi-year lows, kept sentiment muted. Mills preferred domestic sponge iron, DRI, and competitively priced Iranian HBI due to better availability. Seasonal construction slowdown and weak auto demand added to the cautious mood. Even distressed and high-grade cargoes saw limited interest. With expectations of further softening, most buyers stayed on the sidelines.

- Last week, an estimated 3,500-4,500 t of imported scrap were booked by Indian traders. This included approximately 1,500-2,000 t of HMS 80:20 and 2,000-2,500 t of shredded.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) witnessed a slight decline of INR 450/t ($5/t) w-o-w to INR 70,900-71,300/t ($822-827/t) in the key regions of Durgapur, Raipur and Vizag. The price drop stemmed mainly from intensified selling pressure and muted trade volumes, compelling sellers to reduce offers to remain competitive.

- Ferro manganese: Indian ferro manganese (HC 70%) prices witnessed a slight rise of INR 200/t ($2/t) w-o-w to INR 72,300/t ($828/t) exw in Durgapur. However, prices, exw-Raipur, stayed static at INR 72,250/t ($838/t). The slight rise in ferro manganese prices was primarily due to tight supply conditions, leading to upward pressure on prices despite steady demand.

- Ferro silicon: Indian ferro silicon prices slid by INR 1,600/t ($19/t) w-o-w to INR 90,400/t ($1,048/t) exw-Guwahati. Concurrently, Bhutanese prices also softened by INR 1,100/t ($13/t) to INR 90,900/t ($1,054/t) exw. Bulk bookings remained limited due to cautious buyer sentiment and subdued demand, leading to reduced market activity and downward pressure on ferro silicon prices.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices inched up by INR 200/t ($2/t) w-o-w to INR 101,000/t ($1,171/t) exw-Jajpur. Prices remained firm amid stagnant market conditions, as buyer resistance and weak stainless steel demand capped gains.

- Additionally, Vedanta-FACOR’s ferro chrome auction closed at INR 100,400-100,600/t ($1,164-1,166/t) exw for 10-150 mm material, indicating price stability compared to the previous auction. Market direction remains uncertain, with clearer trends expected following OMC’s chrome ore auction next week.

Semi finished

- Indian semi-finished steel prices declined, as per BigMint’s assessment. Domestic billet prices decreased by INR 200-900/t across regions, with Jalna recording a steep drop of INR 800/t.

- Meanwhile, sponge iron prices moved down by INR 100-600/t, with the sharpest decrease of INR 600/t seen in Jharsugda. However, Durgapur and Raipur prices were up by INR 300/t and 500/t, respectively.

- Indian direct reduced iron (DRI) export offers decreased by $2/t for Nepal to $320/t CPT Raxaul, while those for Bangladesh also dropped by $2/t to $330/t CPT Benapole.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for 15,000 t on 10 June 2025. However, only 5,200 t were booked at an average price of INR 31,500/t (by road). However, management approval is still pending. In the previous approved auction, held on 22 May 2025 for 2,000 t, the entire quantity was booked at an average price of INR 32,600/t (by road).

Finished long steel

- IF rebar: India’s IF-route rebar prices continued to face pressure this week, recording further declines. Trading activity was sluggish across most regions, with buyers only purchasing based on immediate needs. The gap between bids and offers led manufacturers to reduce their quotes to stimulate sales. Mills faced sales pressure amid huge inventories. Current stocks at mills stood at 10-15 days. Overall, market participants expect prices to remain range-bound in the short term.

- On a w-o-w basis, rebar prices declined by INR 100-1,200/t across regions, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route for 10-25 mm size were assessed at INR 41,000-41,400/t exw-Raipur and INR 44,400-45,000/t exw-Jalna.

- Trade reference prices of heavy structural steel for base size 150-mm channels stood at INR 42,800-43,300/t exw-Raipur.

- Trade reference prices of wire rods hovered at INR 41,800-42,300/t ex-Raipur.

- BF rebar: Trade-level blast furnace (BF) rebar prices continued to decline this week across major Indian markets. Buyers postponed their purchases amid ongoing price corrections and market uncertainty. Distributors remained in destocking mode, while major mills reduced list prices amid weak market sentiments.

- Trade-level BF rebar prices declined by INR 1,100/t w-o-w to INR 53,200/t exy-Mumbai, as per BigMint’s assessment on 13 June 2025. Prices are exclusive of GST at 18%.

- Weak demand and cautious sentiment kept trade muted, with most buyers moving to the sidelines. In the projects segment, prices slipped further to INR 52,000-52,500/t FOR Mumbai, as slower construction activity and negative outlook weighed on procurement decisions.

Flat steel

- HRC prices in India remained stable w-o-w at INR 51,000-52,800/t ($596-616/t), while CRC prices showed mixed trends at INR 57,000-60,900/t ($659-718/t).

- Distributors held prices steady despite losses, as market rates were below mills’ offers. No price support was offered by mills for May 2025.

- Demand was weak too. Buyers purchased only as needed, avoiding stockpiling due to falling prices and concerns over monsoon-related disruptions.

- India imported 45,882 t of HRCs and plates by 7 June 2025, with another 129,277 t expected by the month-end (BigMint data).

- Indian HRC export offers to the EU dropped $15/t w-o-w to $620-625/t CFR Antwerp, but demand stayed weak due to sluggish local markets and seasonal holidays.

- In the Middle East, post-Eid demand stayed low, affected by the summer slowdown and higher US import duties, as per a BigMint source.

Leave a Reply