- Vietnamese mills resist high offers, prefer domestic scrap

- Tokyo Steel cuts prices at Kyushu, Takamatsu, Okayama

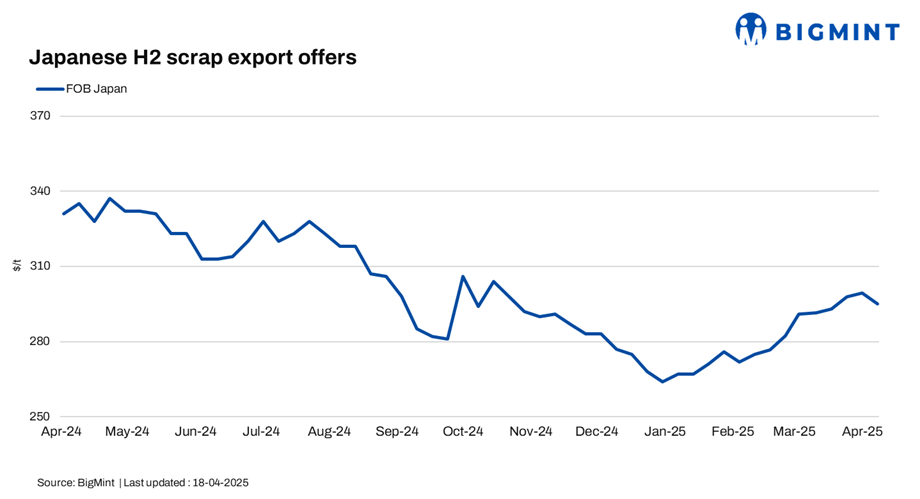

The Japanese H2 scrap export market remained under pressure this week, with BigMint’s weekly assessment of H2 scrap prices decreasing by JPY 800/tonne (t) ($6/t) to JPY 42,000/t ($295/t) FOB Tokyo Bay in comparison to JPY 42,800/t ($301/t) last week.

Prices fell amid weak demand and cautious buyer sentiment. A stronger JPY, uncertainty over tariff policies, and a wide bid-offer gap kept spot liquidity thin. Mills slowed purchases, awaiting greater price clarity.

Offers to Vietnam stayed range-bound at $335-340/t CFR, while bids dropped below $325/t CFR as buyers preferred cheaper domestic scrap.

Additionally, Tokyo Steel announced its fourth scrap purchase price revision this month, effective 18 April 2025, with the last adjustment on 10 April. In this latest round, prices dropped by up to JPY 500/t ($4/t) at Kyushu, Takamatsu, and Okayama while remaining unchanged at other plants. The overall monthly price decline at these plants in April stands at up to JPY 3,000/t ($21/t). Revised prices are as follows:

- Kyushu, Okayama: JPY 42,000/t ($295/t)

- Takamatsu: JPY 40,000/t ($281/t)

Moreover, scrap iron (H2) prices in Japan rose for the third consecutive week, according to data from the Japan Iron and Steel Association. For the second week of April, the average price across three key regions touched JPY 39,200/t ($275/t), marking a JPY 400/t ($3/t) increase from the prior week. Regionally, the central area saw the sharpest rise, climbing up by JPY 1,000/t ($7/t) to JPY 37,800/t ($265/t). Meanwhile, prices in the Kanto and Kansai regions held steady w-o-w at JPY 48,000/t ($337/t) and JPY 38,900/t ($273/t), respectively.

Other market updates

Vietnam: Vietnam’s imported scrap market remained quiet, with only moderate demand returning as construction activity picked up after March. Trade was limited due to a wide bid-offer gap and buyers’ resistance to higher prices. Japanese H2 offers held steady at $335-340/t CFR Vietnam, while bids remained lower at $322-325/t, reflecting a cautious sentiment.

Competitive domestic scrap prices led mills to prioritise local sourcing over imports.

Deep-sea offers from the US and Australia found little interest, as buyers pushed back on elevated levels. During the week, US-origin deep-sea cargoes were offered at $360/t CFR, while Australian-origin material was heard at $355/t CFR.

South Korea: South Korea’s imported scrap market remained under pressure amid rising inventories and weak domestic demand. Major steelmakers announced a KRW 10,000/t ($7/t) reduction in scrap purchase prices across all grades, with some mills applying smaller cuts for specific materials.

Rebar demand stayed sluggish, pushing scrap inventories above 900,000 t – the highest since December 2023.

Meanwhile, imported scrap inflows remained steady at key ports, with over 30,000 t arriving in the second week of April. Gunsan and Dangjin saw the highest volumes, mostly H2 and Shindachi grades. Persistent import arrivals, despite low prices and subdued demand, added further downside pressure to domestic scrap suppliers.

Taiwan: Taiwan’s imported scrap market softened, as global scrap prices declined and local steel demand remained weak. Feng Hsin Steel, the island’s top rebar producer, slashed rebar list prices by TWD 300/t and cut local scrap buying prices by TWD 500/t from end-March levels.

The mini-mill cited falling imported scrap prices as a key driver, with US-origin HMS 80:20 down $10/t to $308/t CFR Taiwan and Japanese H2 scrap falling to $325/t CFR.

Amid sluggish construction demand post-Qingming holidays and heightened global trade tensions, mills such as Feng Hsin held off major moves, instead monitoring market volatility and weak regional steel trends for further cues.

Leave a Reply