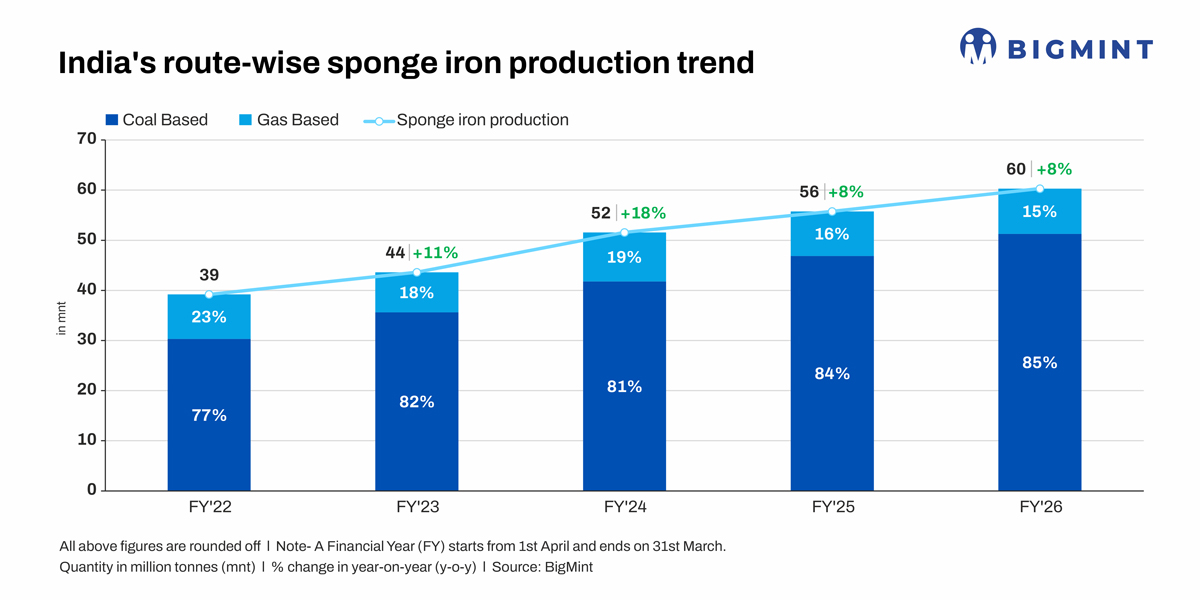

- Output hits record high in FY26, coal-based share rises to 85%

- Higher iron ore, coal output, scrap constraints drive DRI growth

- Waste heat recovery cuts power costs, reduces emissions intensity

Data Deep Dive: India’s direct reduced iron (DRI or sponge iron) production rose 8% y-o-y to an all-time high of 60.3 million tonnes (mnt) in FY’26, according to BigMint data. Coal-based facilities accounted for 85% of total output, up from 77% in FY’22, even as concerns over carbon emissions intensify. In contrast, gas-based production has remained largely stagnant at around 9 mnt, leading to a steady decline in its share.

Coal-based DRI, particularly when used in induction furnace (IF) steelmaking, remains among the most carbon-intensive routes. Emissions from the DRI-EIF route are estimated at 2.7-3.1 tonnes of CO2 per tonne of crude steel (tCO2/tcs), compared with India’s average of 2.54 tCO2/tcs. Gas-based DRI routes are lower at around 1.4-1.6 tCO2/tcs. This divergence raises a key question: why does coal-based DRI continue to expand?

Factors supporting coal-based DRI production

Crude steel production mix shifts, DRI gains in share: Over the past five years, India’s crude steel production mix has gradually tilted towards induction furnaces (IFs). IF-based crude steel output rose to 64 mnt in FY’26 from 36 mnt in FY’22, taking its share of the total to about 38% from 30% over this period. This route has overtaken the electric arc furnace segment, which has remained broadly stagnant at around 28-32 mnt. This has directly supported DRI consumption, with its contribution to crude steel production rising to about 28% in FY’26 from roughly 26% in FY’22.

Lower initial capital investments and a roughly INR 4,000-4,500/t lower Opex compared to the EAF enabled rapid proliferation of IF units, particularly in eastern and central India. These plants are typically smaller, decentralised, and suited to regional demand centres, making them attractive for secondary steel producers. Additionally, IFs offer operational flexibility, as they can operate on variable mixes of DRI and scrap, allowing producers to manage cost and quality dynamically.

Easy raw material availability underpins cost advantage: The growth of coal-based DRI has been enabled by strong domestic availability of iron ore and non-coking coal. Around 60% of sponge iron production is concentrated in Odisha, Chhattisgarh and West Bengal, which have proximity to both resources.

India’s production of both has increased sharply over FY’22-26: iron ore by 24% to 314 mnt and coal by 34% to 1,041 mnt. Accordingly, pellet output has grown 46% to around 117 mnt in FY’26. India’s DRI production is heavily pellet-based, accounting for over 60-65% of total production. Additionally, DRI producers have gradually reduced their usage of South African non-coking coal in their feed, leading to lower dependence on imported coal. In the benchmark production hub of Raipur, 60-70% domestic and 30-40% imported coal are blended, according to sources.

Conversely, limited domestic gas supply, high imported LNG costs, and a small producer base have constrained gas-based capacity additions. Meanwhile, the capital-intensive nature of BF-BOF production set-ups, as well as heavy dependence on imported coking coal, are major obstacles to growth, although the integrated sector has lined up a series of investments.

Similarly, limited or inconsistent availability of high-quality scrap, as well as import dependence, has constrained the expansion of EAF-based production, where feedstock substitution is not as flexible. In fact, traditional scrap-based clusters, including those in northern (Mandi Gobindgarh, Ludhiana) and southern regions, have increasingly shifted towards DRI due to tightening scrap availability. Major steelmakers have also announced plans to raise the ratio of scrap in their charge mix to 30% from 8-10%, given that this is the most convenient way to reduce carbon emissions in BOF production. This will tighten scrap availability even further in the coming decade.

Scrap imports are also unlikely to bridge the supply gap. Several countries including major suppliers such as the EU are either considering or imposing restrictions on scrap exports to secure domestic availability and as part of efforts to decarbonise steel production.

BigMint projects that India’s total scrap consumption could reach 60-65 mnt by FY’30 against domestic availability of around 45 mnt, implying a 15-20 mnt structural gap that will need to be met through imports and alternative metallics. The growth of coal-based DRI has been enabled by strong domestic availability of iron ore and non-coking coal. Around 60% of sponge iron production is concentrated in Odisha, Chhattisgarh and West Bengal, which have proximity to both resources.

Waste heat recovery strengthens economics: Coal-based sponge iron economics are increasingly supported by waste heat recovery systems. Using a waste heat recovery boiler (WHRB), a 350 tonnes per day (tpd) sponge iron kiln can generate around 7-9 megawatts (MW) of power in central and eastern India using domestic coal and up to 10 MW in the southern regions, where imported coal usage is higher. As a general benchmark, a 100 TPD kiln can produce approximately 2 MW, depending on coal quality and blend composition (typically 60-70% domestic and 30-40% imported coal).

Power generated through WHRB costs around INR 1.50-2.50 per unit, compared with INR 6.50-8.50 per unit from state electricity boards or open market suppliers, depending on contract terms and load usage. This creates a significant cost arbitrage, allowing producers to reduce operating expenses and support downstream operations such as ferro alloy production. Significantly, factoring in the carbon credit accrued due to power generation from waste heat, the total CO2 profile becomes much more competitive for coal-based producers compared with the natural gas-based producers of sponge iron.

Emissions remain a concern but mitigations emerging

Regulatory approvals are now largely limited to larger DRI kilns of around 300-350 tpd, with smaller 50-100 tpd units facing increasing restrictions. Several state pollution control boards, supported by central policy direction through circulars, have made it clear that future capacity additions will prioritise larger, more efficient reactors. When these larger kilns are integrated with WHRBs, their emissions intensity declines materially. Additionally, certain other measures such as ore pre-heating in the kiln, efficient cooling and lining systems lead to further efficiency improvements.

Another significant factor is the integration of solar power, either through captive sources or open access, in the coal based DRI-EIF route to mitigate emissions from steel melting even further, thereby reducing the overall footprint of this route. This shifts the narrative around coal-based DRI. While the route has historically been criticised for its high emissions, it is unlikely to be phased out in the near term. Instead, the sector is undergoing a process of technological upgrading rather than total displacement even as fuel switch technologies lie further in the future. As a result, coal-based DRI is expected to remain a core component of India’s steel ecosystem over the next decade or longer, even as decarbonisation pressures increase.

Outlook

The core policy question remains whether the continued growth of coal-based DRI production will align with India’s 2070 carbon neutrality target. BigMint believes that the sector will continue to grow resiliently over the next decade, supported by raw material availability, consolidation, scrap supply constraints, favourable cost structures, and strong linkage with induction furnace steelmaking.

India is advancing carbon market mechanisms, including a carbon trading platform that would require high emitters to purchase credits while allowing low emitters to monetise reductions. For 253 steel mills under the compliance framework of the Carbon Credit Trading Scheme (CCTS), emissions mitigation targets have been given for the couple three fiscals. However, market watchers believe that the targets are not too stiff, and given the efficiency measures and consolidation in the coal-based DRI sector, producers are likely to continue operating at scale over the next 10 years without significant cost penalties.

Leave a Reply