- Grade shortages trigger rallies despite elevated port inventories

- Low port storage fees encourage stockpiling over selling at low prices

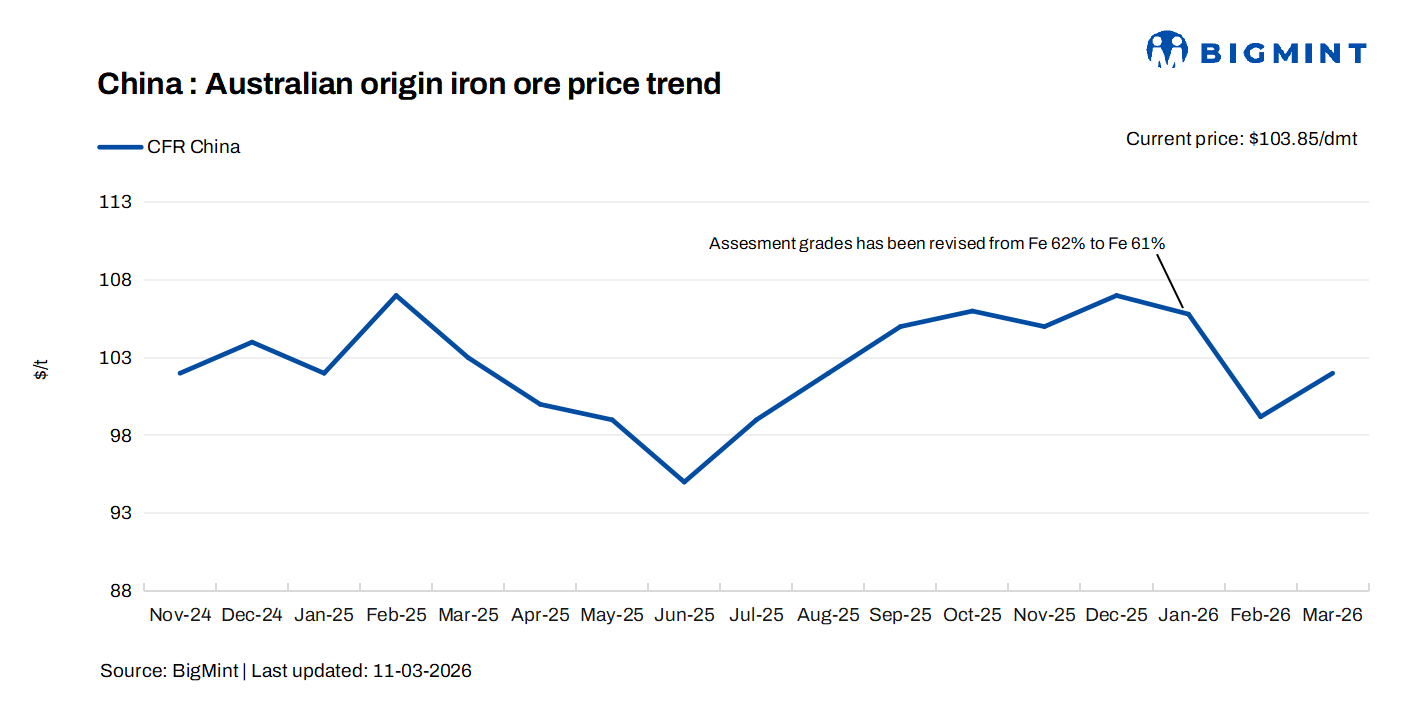

Mysteel Global: To date, China’s imported iron ore port inventories have remained above 130 million tonnes (mnt) for nearly three years. Over the same period, benchmark seaborne iron ore prices have retreated markedly, with highs sliding from around $143/dmt in early 2024 to roughly $100/ dmt at present, indicating a clear downward shift in the average price level.

The persistent buildup in inventories largely reflects the structural oversupply of seaborne iron ore following new mine capacity coming onstream, combined with gradually weakening domestic crude steel demand in China.

However, Mysteel’s tracking of market developments in recent years suggests that the relationship between port stock accumulation and iron ore price movements is not consistently negative. Several factors help explain this divergence.

Short-term supply disruptions

The first quarter is typically a period of frequent weather-related disruptions for global iron ore supply, including cyclones in Australia and the rainy season in Brazil. Such events can temporarily curb shipments from major miners and quickly translate into tighter spot supply in the seaborne market.

These supply losses are reflected in price movements almost immediately, while their impact on Chinese iron ore port inventories tends to appear with a lag. As a result, iron ore prices may rise in response to supply shocks even as port inventories continue to build.

Circulating supply, inventory structure matter more than absolute volumes

Although China’s total port inventories have remained elevated in recent years, the volume of readily tradable cargoes has often been limited, and temporary tightness in certain ore grades has constrained the downside in prices.

Relatively low port storage costs have encouraged iron ore traders to hold higher-cost cargoes rather than sell at depressed prices, which has reduced the amount of iron ore actively circulating in the market.

At the same time, negotiations between Chinese buyers and BHP in 2025 reportedly faced difficulties, restricting the circulation of Jimblebar Fines and leaving part of port stocks effectively stranded as “dead inventory”.

Structural imbalances in grade availability have also influenced price movements. In the second half of 2025, inventories of mid-grade ores — represented by PB fines — tightened significantly, while the availability of Jimblebar fines remained constrained.

As a result, stocks of mid-grade ore materials fell to extremely low levels during the year, leading to pronounced grade differentiation in the iron ore market and driving a noticeable price rally, even though total port inventories remained historically high.

Steel mills’ low-inventory strategy triggers periodic restocking

In recent years, most Chinese steelmakers have adopted a low raw-material inventory strategy, purchasing iron ore largely on a just-in-time basis to control costs and reduce balance-sheet pressure.

However, ahead of extended holidays — such as China’s National Day in October and the Chinese New Year in January/February — mills often conduct short bursts of concentrated restocking to ensure sufficient feedstock during production schedules. This periodic surge in procurement demand tends to provide short-term support to iron ore prices, regardless of the prevailing inventory levels at ports.

Narrowing futures-spot basis

Iron ore derivatives also play a role in shaping price movements. Iron ore futures listed on the Dalian Commodity Exchange typically have delivery months in April, August, and December.

Given the prevailing market expectation of ample supply and relatively weak demand for iron ore, this commodity’s futures prices often trade at a discount to spot prices for much of the year. As the delivery month approaches, futures prices tend to converge with the spot market.

Historical data suggest that when spot prices of iron ore remain relatively stable, futures prices are more likely to rise to narrow the discount, rather than spot prices falling to meet futures levels. This process of basis correction can drive futures-led price increases that do not closely follow changes in port inventories.

Iron ore market outlook for 2026

Overall, the global iron ore market continues to face structural oversupply, and China’s port inventories are likely to remain elevated as a new normal. This backdrop has contributed to the downward shift in iron ore price averages in recent years.

Nevertheless, the correlation between inventory levels and price movements is not linear. Supply disruptions, temporary tightening in inventory structure, and futures-spot basis adjustments can all trigger price increases even during periods of stock accumulation.

Looking ahead to 2026, China’s imported iron ore prices are expected to fluctuate within a relatively low range. Market participants will closely monitor negotiations between Chinese buyers and major iron ore miners, as well as the potential impact of further supply growth on price dynamics.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply