- Global copper inventories hit record highs despite mine supply disruptions.

- Weak Chinese demand continued driving copper stockpile accumulation globally.

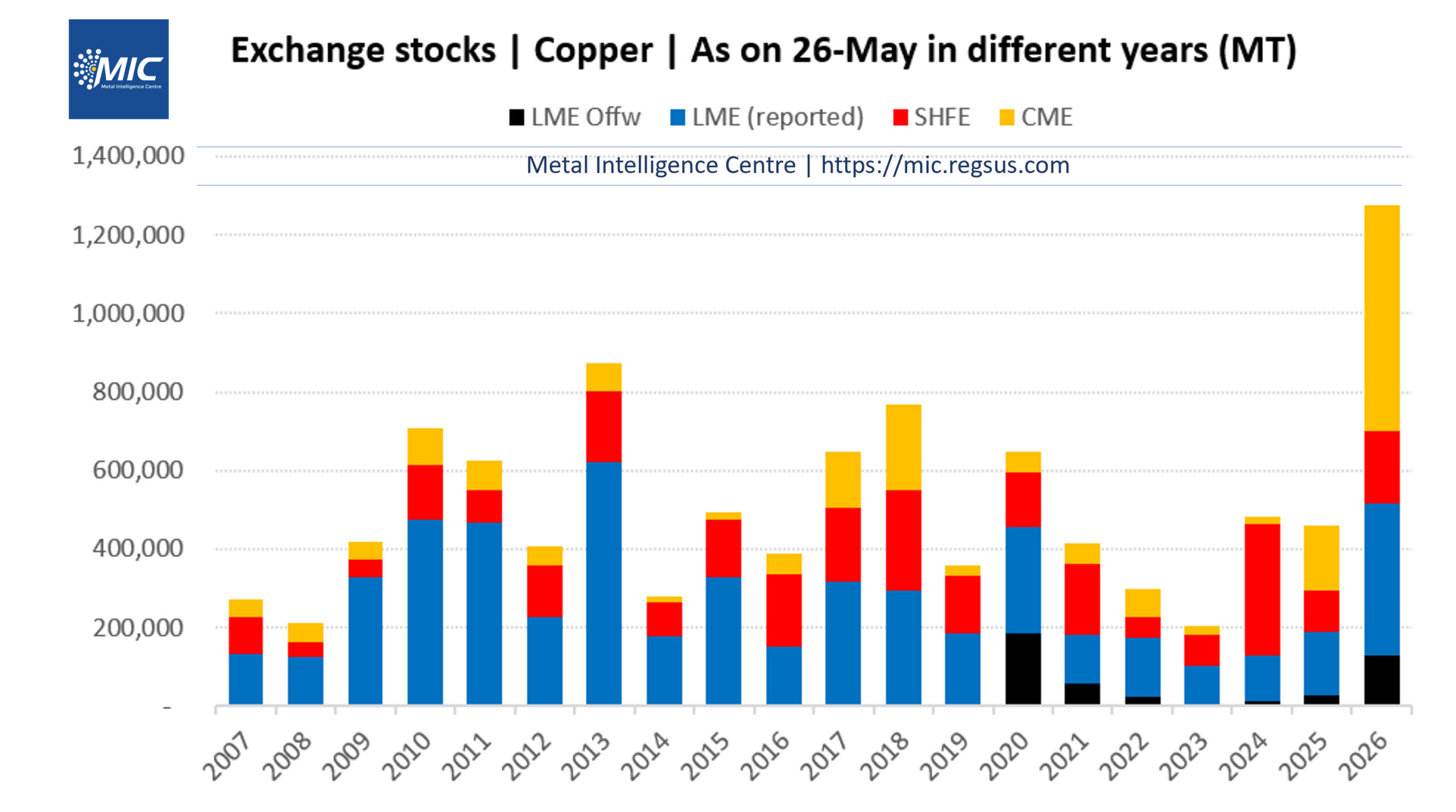

Metal Intelligence Centre: As of 26 May 2026, combined copper inventories across the three major exchanges -the London Metal Exchange (LME), COMEX, and the Shanghai Futures Exchange (SHFE) – reached 12,76,355 mt, marking the highest ever level for this date in the metal’s recorded history.

COMEX accounted for 45% of these inventories. A positive price gap between CME and LME prices attracted a record volume of inventories to the American exchange since last year.

Combined inventories in the LME, both reported and off warrant, accounted for 41% of the total. In the last one year, these stocks increased by 3,29,302 mt to reach the highest level in LME history for this date. Lower Chinese imports this year, which fell by roughly 10% in the first four months of the year, are the principal reason for this accumulation.

Inventories at the Shanghai Futures Exchange (SHFE) accounted for 14% of total global exchange stocks, rising by 76,043 mt from the same date last year. The increase reflects weak domestic demand in China alongside sustained refined copper production.

Surplus grows

The steady build-up in inventories is reflected in ICSG data.

In March 2026, copper supply exceeded demand by 69,000 mt, bringing Q1’s seasonally adjusted balance to a surplus of 247,000 mt – well above the 148,000 mt and 49,000 mt recorded in the same periods of 2024 and 2025.

ICSG reported 3.5% y-o-y growth in refined metal production in Q1 2026, stepping up from 1.9% y/y growth in the same quarter last year.

The National Bureau of Statistics of China reported a 5.62% y-0-y rise in Chinese output of refined metal in January–April 2026.

Supply disruption

Record refined metal production has emerged despite growing supply disruptions.

In September 2025, the Grasberg copper mine, one of the world’s largest copper-gold mining complexes, was hit by a serious underground incident, forcing operator Freeport-McMoRan to halt operations and declare force majeure. This led to growing worry among investors about copper shortages. The Grasberg mine accounts for around 3-4% of global mined copper output.

Also, the Iran war has almost stalled shipments of sulphur from the region, thereby potentially constraining output of SXEW copper from African and South American mines. ICSG’s data showed a 0.4% contraction in mining output in Q1 2026.

Demand slows

The sharp rise in exchange inventories in recent months indicates that end-user demand, especially in China, has been weak.

China’s industrial production rose 4.1% y-o-y in April, missing expectations and slowing sharply from March’s 5.7%, marking the weakest growth in nearly three years and signalling softening demand conditions.

The country’s fixed-asset investment fell 1.6% in Jan-Apr 2026, reversing from a 1.7% rise in Q1 and signalling that policy support has yet to translate into sustained capital formation.

China’s EV sales, which grew by 19% y/y last year, declined 8% y-o-y in Jan-April 2026.

ICSG reported global consumption growth slipping to 1.2% y-0-y in Q1 this year, down from 6.6% y-o-y in the same period in 2025.

Conclusion

Contrary to investors worries about shortages, copper inventories remain plentiful despite supply disruptions. Although an extended Iran war may affect supplies of SXEW copper, its overall impact could be small and may be offset by a demand slowdown, especially in China.

Note: This article has been published as part of a content partnership between MIC and BigMint.

Leave a Reply