- India may add ~1.5 mnt refining capacity by FY’30

- Copper demand projected to reach ~10 mnt by 2047

As India charts its path toward becoming a developed nation by the centenary of its independence, Viksit Bharat 2047 lays out a bold vision of a $35 trillion economy with a per capita income of $20,000-$21,000. At the heart of this transformation is a focus on innovation, sustainability, and industrial leadership. Copper, as a critical enabler across sectors like transportation, telecommunications, renewable energy, and healthcare, will play a pivotal role in realising this vision and supporting India’s emergence as a global leader in technology and infrastructure.

Mining and beneficiation

India’s only copper miner, Hindustan Copper Ltd (HCL), has maintained a stagnant output of ~4 mnt/year in recent years due to issues like mining lease delays, water shortages in Rajasthan, and the shift to underground mining at Malanjkhand. However, HCL plans to triple ore production to 9.6 mnt in the short term, with a long-term goal of 12.2 mnt, led by the Malanjkhand expansion from 2.5 to 5 mnt.

Copper concentrate imports

In CY’23, India imported around 1 mnt of copper concentrate, with 75% sourced from just four countries—Indonesia (27%), Chile (25%), Peru (14%), and Panama (9%). With ~90% of India’s copper concentrate needs met via imports in FY’24—projected to rise to 95% by FY’30—this overdependence poses supply risks. To reduce vulnerability, India must ramp up domestic mining, invest in overseas assets, diversify supply chains, and boost recycling to build long-term resilience.

Expansion plans of major copper producers

India’s leading copper producers are stepping up capacity expansions and establishing new facilities to ensure a reliable supply of refined copper. This move is aimed at narrowing the supply-demand gap and supporting the country’s industrial and technological growth. India currently has 1.285 mnt (MT) of smelting and refining capacity, which is projected to reach 1.785 mnt by 2029 with the full commissioning of Kutch Copper Ltd (Adani Group).

Driven by the growing need for copper in sectors like infrastructure, EVs, and renewable energy, companies like HCL, Hindalco, Vedanta, and Adani are actively boosting domestic output and exploring global opportunities. These initiatives—across both primary and secondary production routes—are essential for strengthening India’s copper supply chain, reducing import dependence, and enhancing global competitiveness.

In FY24, India imported 0.31 mnt of copper scrap, growing at a 10% CAGR since FY18, aided by the import duty cut from 5% to 2.5% in 2021–22. Policies like the Vehicle Scrappage Policy, EPR, and RCM are expected to boost recycling. However, India’s current secondary production relies mainly on direct melting. With QCO implementation, secondary refining is likely to expand in the coming years.

Copper prices ranged between $8,500-10,500/t in 2024, with future prices expected to rise amid mine depletion and falling ore grades. Global demand may reach 36.6 mnt by 2035, but supply could lag at 30.1 mnt, leading to a 6.5 mnt deficit.

Expected growth of copper sector

India’s domestic copper demand is expected to grow significantly, reaching 8.8–9.8 mnt by FY47, up from current levels, as infrastructure, EVs, and renewable energy drive consumption. Per capita copper use is set to rise from ~1.2 kg in FY24 to 5.4–6 kg by FY47, marking a 4.5–5-fold increase. Historical data from China (7x growth in 17 years) and the U.S. suggest India’s copper demand will likely continue rising even beyond 2047 as industrialisation and electrification accelerate.

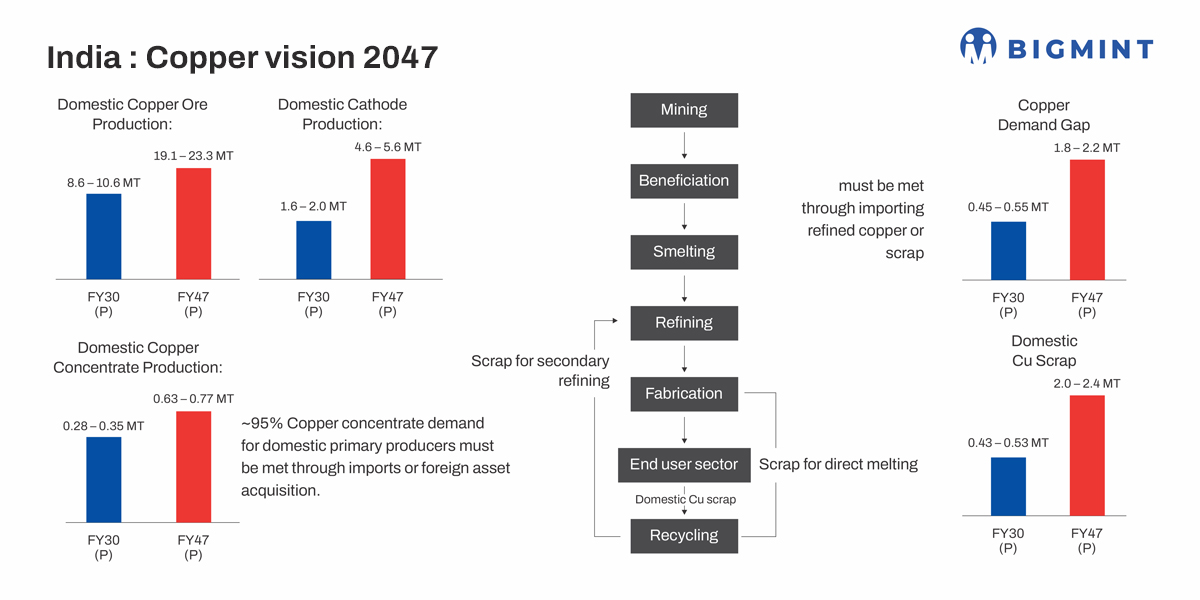

India’s Copper supply outlook: 2030 and Amrit Kaal

India needs to add ~1 mnt of refining capacity every five years to meet the projected 10 mnt copper demand by 2047. With 95% of copper concentrate needs expected to be met via imports by 2030, expanding domestic mining through reopened or auctioned blocks and forging long-term offtake deals with copper-rich countries like Chile, Peru, and Australia is critical.

By FY30, India is expected to add ~1.5 mnt refining capacity-led by Adani’s Mundra project-taking the country’s refined copper output to 1.6–2.0 mnt. Despite growing scrap availability (projected at 430,000–530,000 t), about 95% is still expected to be directly melted, with minimal secondary refining. The country will remain import dependent for 0.45–0.55 mnt of copper through cathode or scrap.

By 2047, India’s copper ore production is projected at 20.2 mnt—mainly from HCL and auctioned mines—but import dependency for concentrate may still exceed 95%.

To meet the projected demand of copper cathodes India needs to add approximately 1 mnt of smelting and refining capacity every five years to meet the projected copper demand. Copper cathode supply is expected to reach 4.6 -5.6 mnt.

India is expected to generate 2–2.4 mnt of domestic copper scrap by FY47, with around 80% directly melted into semis and finished goods. The anticipated copper demand gap of 1.8–2.2 mnt will likely be met through refined copper and scrap imports. Future scrap and copper sources may include the UAE, Saudi Arabia, Africa, and Latin America, as developed countries reduce exports to retain scrap for domestic use. Strategic offtake deals with invested firms can also help bridge the gap.

Leave a Reply