- South African coal gained but Indian buying stayed highly selective

- Met coke and coking coal markets remained steady amid weak steel sentiment

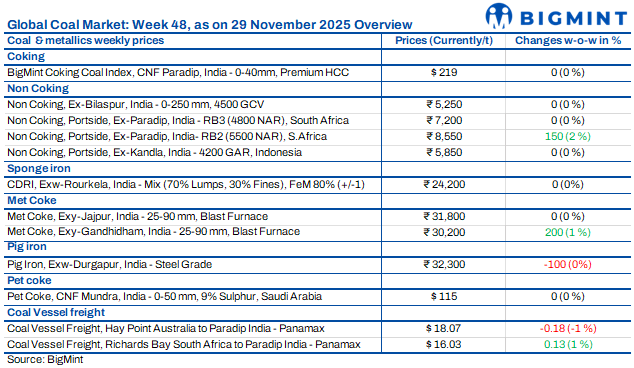

Coal market sentiment remained cautious in the week ended 28 Nov, with firm seaborne offers contrasting against subdued Indian buying. Portside activity stayed selective as industries resisted higher quotes, while domestic coal trading held steady with support from ongoing auctions. Met coke and coking coal markets showed limited movement, reflecting muted steel demand. Overall, sentiment remained balanced but hesitant, with buyers waiting for clearer direction in December.

Indonesian portside coal prices stayed stable amid weak buying interest

India’s portside Indonesian thermal coal market remained steady w-o-w as of 28 November 2025, supported by firm global benchmarks but held back by muted domestic demand. Price movement stayed limited as vessel diversions to China and stable export values prevented any meaningful correction. Traders attempted to raise offers, but weak procurement and ample port stocks kept transaction volumes low. BigMint’s assessments showed 5000 GAR unchanged at INR 7,200/t (Kandla) and INR 7,100/t (Vizag), while 4200 GAR held at INR 5,850/t and INR 5,750/t. The 3400 GAR grade remained stable at INR 4,600/t at Navlakhi, with no aggressive restocking to shift prices. On the seaborne front, Indonesian prices moved mixed: 5800 GAR edged up by $0.30/t, while 4200 GAR and 3400 GAR dipped modestly, reflecting softer demand for low-CV cargoes despite rain-related constraints in Kalimantan.

India stayed cautious as Asian coal prices firmed on tight supply

India’s portside market remained cautious even as South African thermal coal offers rose w-o-w on firm North Asian demand and tighter seaborne supply. RB2 at Paradip moved to INR 8,550/t, while Vizag and Gangavaram saw smaller gains, supported by a 50,000 t deal at INR 8,700/t ex-Paradip. Yet buying stayed selective, with most industries resisting high offers amid mixed inventories and costlier freight. Traders noted that Chinese and Korean demand kept international prices firm, but Indian buyers maintained a wait-and-watch stance, expecting clearer direction after mid-December as stocking decisions approached.

Domestic coal prices stay steady as auction activity intensifies

Domestic coal prices stayed firm w-o-w on 28 Nov, with 5,000 GCV at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. Demand had started to pick up as SECL and ECL lined up frequent auctions ahead of winter needs. Although bidding remained strong in the latest SECL auctions, broader market traction stayed weak, with industrial offtake continuing to lag despite aggressive participation seen in the past two events.

India’s coking coal index stayed steady amid weak buying interest

BigMint’s premium hard coking coal (PHCC) index held stable at $219/t CNF Paradip on 28 November 2025, unchanged from the previous week as bid-offer gaps persisted. Australian offers hovered at $217-220/t CFR India, while bids remained closer to $210/t due to muted steel sentiment. Recent Chinese deals kept global coking coal offers firm. BigMint expanded its PHCC CFR India Index to include normalised material from Australia, Canada, the US, and Mozambique to reflect shifting trade flows. BF-rebar prices in India fell to a 5-year low of INR 46,300/t ex-Mumbai as slow trading and high inventories pushed sellers to offer discounts.

India’s met coke market stayed steady with mild regional variation

India’s met coke market remained broadly steady during the week, with pricing showing a slight regional split. BF-grade met coke stayed unchanged at INR 31,800/t ex-Jajpur, while western prices in Gandhidham inched up to INR 30,200/t, reflecting modest support. Foundry-grade met coke in Rajkot held firm at INR 36,000/t. Market participants adopted a cautious stance as they awaited clarity on anti-dumping duties, while higher feedstock costs added gentle upward pressure. Chinese met coke sentiment stayed soft, with steady spot prices but weak steel margins and rising inventories limiting buying. Domestic pig iron edged down to INR 32,400/t as trade interest eased.

India’s petcoke trade stayed muted as buyers favoured cheaper coal

India’s imported petcoke market faced weak momentum this week as high supplier offers met firm resistance from buyers dealing with soft cement sector demand. Prices slipped w-o-w, with CFR India assessed at $115.50/mt, down $1.50. Cement plants operated at 70-75% capacity, limiting fuel requirements, while the wide $6-9/t bid-offer gap prevented deals. Buyers shifted towards cheaper high-CV thermal coal from South Africa and US NAPP coal. Pet coke offers at $117-121/t found no traction as freight from the US Gulf rose to $47.50/t and China absorbed higher-priced cargoes. Market expectations turned cautious, awaiting clearer construction-season demand.

India: Coal freight market showed clear split as bunker costs increased

India’s coal freight market displayed a clear divide w-o-w, with Pacific basin rates staying soft while the Atlantic basin held firm. The Pacific market weakened due to abundant vessel availability, weak Indian coal demand, and limited fixtures, while the Atlantic benefitted from tighter tonnage and steady export offers. Panamax freight on the Australia-India route fell to $18.07/dmt, whereas the South Africa-India route inched up to $16.03/dmt. Supramax rates from Indonesia rose to $14.50/dmt, though activity stayed muted.

Bunker prices inched higher w-o-w, adding cost pressure on shipowners as Brent crude futures increased. The Baltic Panamax index rose to 1,962, while Supramax edged up to 1,437. Overall sentiment stayed cautious, with India-bound coal freights expected to remain rangebound to soft unless procurement improves or vessel supply tightens.

Leave a Reply