- South African coal demand stays selective despite stronger market cues

- Domestic auctions see slower lifting due to falling bid prices

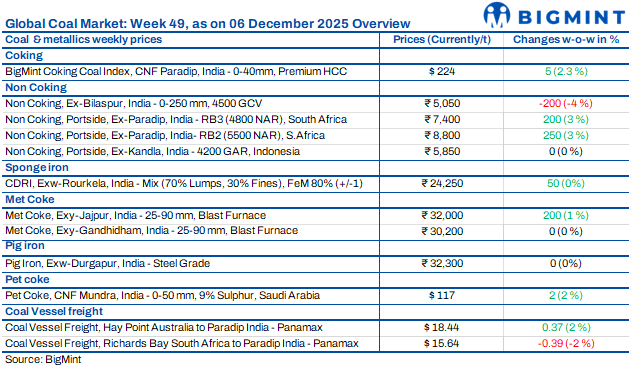

India’s coal market sentiment stayed balanced this week, with import demand remaining selective while domestic buying turned cautious following recent auction price corrections. South African offers stayed firm, but end-users preferred to wait as freight constraints and vessel shortages supported seaborne levels. Domestic mid-CV coal stayed tight, keeping industrial interest steady, though weaker sponge iron activity and cautious procurement limited aggressive restocking across ports.

Indonesian coal prices stable, market expects demand adjustment

Indian portside Indonesian thermal coal prices remained stable w-o-w as of 5 December, supported by firm global benchmarks that prevented deeper discounts. Market sentiment stayed divided: some participants noted that China’s recent slowdown could benefit Indian buyers if demand improved, while others highlighted downside risk for 3400 GAR due to heavy inventories and rising lignite preference ahead of the 10 December auction. Key grades such as 5000 GAR, 4200 GAR and 3400 GAR held steady across Kandla, Vizag and Navlakhi. Indonesian seaborne prices slipped w-o-w as exporters cut offers amid softer buying interest. The near-term outlook pointed to stability for mid-CV coal but a weakening bias for 3400 GAR.

Coal market splits as South African offers rise & buyers step back

India’s thermal coal market showed a clear divergence as South African offers continued to rise while domestic buyers remained highly selective. Imported RB2/RB3 prices moved higher across ports, with RB2 reaching INR 8,800/t at Paradip, INR 8,700/t at Gangavaram and INR 8,650/t at Vizag. RB3 also increased to INR 7,300-7,400/t. Despite these gains, Indian buyers preferred to wait, resisting firm seaborne offers and focusing on domestic coal instead. Sellers held back stock in anticipation of further hikes, supported by strong indices, higher freight and vessel shortages for Jan-Mar deliveries. Deals included 5,000 t at INR 8,700/t ex-Mangalore and another 5,000 t RB2 at INR 8,400/t. Export offers strengthened as RB2 rose to $76/t and RB3 to $60.5/t w-o-w.

Domestic coal prices soften on lower auction bids

Domestic coal prices eased w-o-w, with 5,000 GCV declining to INR 6,150/t and 4,500 GCV slipping to INR 5,050/t ex-Bilaspur. Buyers avoided lifting coal purchased in earlier SECL auctions after noticing significantly lower bid levels in recent events, which left many holders at risk of losses on higher-priced stock. This bid correction kept overall sentiment cautious. SECL’s upcoming 9 December auction is set to offer 1,096,000 t.

India coking coal index edges up

India’s PHCC index inched up to $224/t CNF Paradip on 6 Dec’25, rising $5 w-o-w amid firmer global cues. However, the domestic steel sector showed weak sentiment, and wide bid-offer gaps persisted as buyers resisted Australian offers above $220/t CFR. Prices were supported by recent Chinese deals that lifted global offers. Met coke prices had firmed in the east while staying stable in the west, even as China’s coke market softened further due to weak steel demand and rising inventories. Indian BF rebar prices showed mixed signals for early December after selective hikes by primary mills.

Met coke prices edge up in eastern India

India’s met coke market showed a mixed trend in early December. Prices in east India firmed, with BF-grade material rising to INR 32,000/t ex-Jajpur as tighter supply and a 27,500 t deal supported sentiment. Western prices stayed unchanged at INR 30,200/t ex-Gandhidham, while foundry-grade coke in Rajkot held steady at INR 36,000/t amid selective demand. Higher seaborne coking coal costs and a weaker rupee added upward pressure, as Australian PHCC moved up to $202/t FOB. In China, coke sentiment stayed weak due to cautious buying, higher inventories and reduced steel output. Overall, Indian met coke prices remained firm but upside stayed limited by soft regional fundamentals.

Imported pet coke offers rise w-o-w

Imported pet coke offers edged up this week, with US-origin assessed at $118-120/t and Saudi-origin at $117-119/t across both coasts, up $2/t w-o-w as per BigMint’s assessment. Despite the increase, buying stayed subdued as most end-users remained well stocked from earlier low-priced purchases. The presence of cheaper domestic coal also reduced the urgency to procure imported pet coke, keeping overall trading momentum muted.

Nayara Energy raised its pet coke price to INR 14,880/t from 1 December, up INR 60/t from INR 14,820/t in the previous month. The small increase followed November’s INR 50/t reduction and came amid continued tight domestic supply. With RIL consuming all pet coke internally since Apr’25 and Nayara’s output down 25-30% due to crude constraints, market availability remained limited.

Coal freight rates rebound in Pacific, Atlantic market softens

Coal freight rates to India showed mixed movement this week. Pacific routes firmed up w-o-w as tighter prompt tonnage from Australia and Indonesia pushed rates higher, despite fewer fixtures and limited Indian chartering activity. Conversely, Atlantic rates softened due to muted enquiry and a growing list of open vessels. Rising bunker costs also added upward pressure to overall freight sentiment. Australia-India Panamax rates rose to $18.44/dmt, while South Africa-India eased to $15.64/dmt. Supramax rates from Indonesia to India increased slightly to $14.70/dmt. Overall, the market remained stable, with Pacific strength offsetting weaker Atlantic momentum.

Leave a Reply