- Buyers wait for post-festival restocking, clearer pricing signals

- Prices range-bound across most grades; domestic coal surges

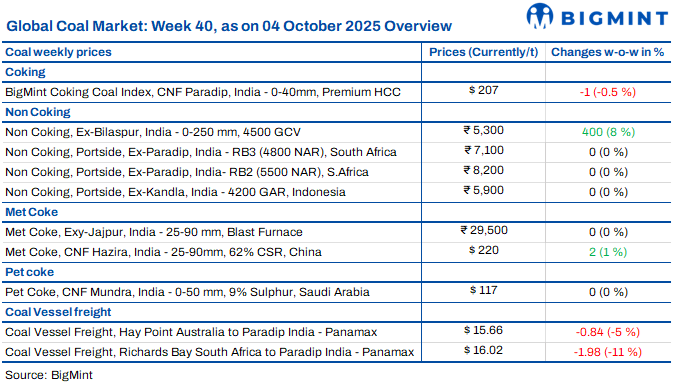

India’s coal market was largely stable this week, with muted buying seen across domestic and imported coal. Festive holidays and subdued industrial activity kept trade volumes low, while inventories remained adequate. Buyers adopted a wait-and-watch stance, waiting for post-festival restocking and clearer signals from auctions and supply trends. Overall sentiment remained cautious, with market participants expecting activity to pick up gradually in the coming weeks.

Indonesian portside coal prices stable amid festive demand lull

Indonesian portside thermal coal prices in India held steady this week as festive holidays and weak industrial activity slowed demand. BigMint assessed 5000 GAR at INR 7,100/t at Kandla and INR 7,050/t at Vizag, while 4200 GAR stayed at INR 5,900/t and INR 5,800/t, respectively. Power plant stocks fell to 45.84 million tonnes (mnt), enough for just 15 days of use, raising supply concerns. Seaborne prices softened slightly, with 5800 GAR at $76.10/t and 4200 GAR at $43.32/t. Market participants expect prices to remain range-bound until post-festival restocking improves sentiment.

South African portside coal offers remain stable amid festive slowdown

South African portside coal prices in India stayed stable this week, with RB2 at INR 8,200/t and RB3 at INR 7,100/t across Vizag and Gangavaram. Market activity remained muted due to the Dussehra holidays, with limited trade seen at INR 8,300/t ex-Vizag and Krishnapatnam. Freights from South Africa to India eased to $16.02/t, reflecting lower chartering activity. Portside inventories dipped slightly to 11.86 mnt, as traders adopted a wait-and-watch approach following GST reforms. Prices are likely to remain steady until post-festive restocking begins.

Domestic coal prices rise on strong SECL auction premiums

Domestic coal offers increased by INR 400-500/t w-o-w this week, with 5,000 GCV assessed at INR 6,250/t ex-Bilaspur and 4,500 GCV at INR 5,300/t. The hike followed SECL’s recent auction, where sponge-grade coal fetched strong premiums. Further support came from SECL’s new rule mandating financial coverage for coal quality upgradation under the e-auction system, prompting sellers to lift offers. However, no major deals were concluded, as buyers waited for clarity on these changes. Market sentiment remained cautious, but traders expect clearer direction once deliveries and payments under the revised system begin.

Met coke trade steady amid festive lull, China hikes

India’s met coke market held steady during the week ending 1 October 2025. BF-grade (25-90 mm) was assessed at INR 29,500/t ex-Jajpur, while prices in western India stayed at INR 30,000/t ex-works Gandhidham. Foundry-grade material stood at INR 35,600/t ex-Rajkot. Market activity was muted amid holidays, though Australian PHCC inched up by $3/t w-o-w to $190/t FOB. In China, mills raised coke by RMB 50-75/t ($7-10.5/t), while India’s pig iron market stayed cautious, limiting near-term met coke demand.

Imported pet coke offers steady in India as trading pauses for holidays

Imported pet coke prices in India were unchanged this week, with US-origin assessed at $118-120/t CFR and Saudi-origin at $117-119/t CFR. Sellers remained firm on offers despite limited spot activity, as festive holidays slowed industrial participation and delayed fresh bookings. Market participants expect clearer direction and renewed buying interest once post-festival operations restart, though overall sentiment remains cautious in the near term.

Nayara, BPCL hike pet coke prices amid tighter availability

Nayara Energy increased its pet coke price by INR 580/t to INR 14,870/t, w.e.f. 1 October, from INR 14,290/t last month. The hike extends pet coke’s upward trend, reflecting tight supply, as RIL remains absent from the market since April. BPCL also raised prices, with Bina refinery at INR 14,749/t (rail) and Kochi at INR 12,547/t. Reduced availability and higher refinery costs continued to support domestic pet coke prices, keeping the overall market firm into October.

Dry bulk coal freights show mixed movements

Dry bulk coal freight rates showed a mixed trend this week. Indonesia-India Supramax freights rose to $16.47/dmt, supported by tighter vessel supply and firm owner sentiment, while South Africa-India Panamax rates dropped to $16.02/dmt, and Australia-India eased to $15.66/dmt amid thin activity. No new fixtures were heard, reflecting a quiet market during the holidays. India’s portside coal inventories fell slightly to 11.86 mnt as traders stayed cautious following GST reforms and volatile ocean freight conditions, keeping overall sentiment steady but watchful.

Leave a Reply