- Portside South African offers rise, but Indian buying muted

- SECL’s auction bids improve as traders face low inventories

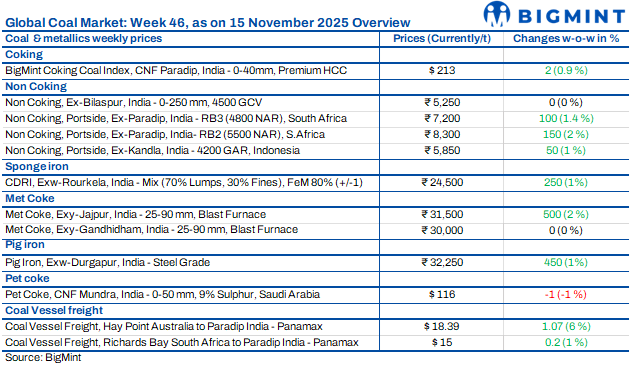

The coal market this week reflected steady sentiment as buyers remained cautious and restocking stayed selective across major ports. Imported coal offers held firm due to stronger global cues, but domestic buying interest was still restrained as sponge iron and industrial demand showed uneven recovery. Auctions saw active participation, yet overall procurement remained measured, keeping trade momentum moderate despite improving signals in a few regions.

Indonesian coal prices gained as Chinese demand strengthened

Indian portside prices for Indonesian coal moved higher w-o-w, supported by firmer global benchmarks and renewed Chinese buying. 5000 GAR rose to INR 7,200/t at Kandla and INR 7,100/t at Vizag, while 4200 GAR reached INR 5,850/t and INR 5,750/t. The 3400 GAR grade climbed to INR 4,550/t at Navlakhi. Chinese procurement strengthened, as import controls eased, and domestic output fell, lifting regional sentiment. Indian power plant stocks increased to 51.56 mnt, providing 17 days of cover, even though 15 plants remained under critical levels. Seaborne prices edged higher, with 5800 GAR at $80.45/t, 4200 GAR at $48.40/t, and 3400 GAR at $32.63/t.

South African coal prices rise, but buying remains sluggish

South African thermal coal prices firmed w-o-w at Indian ports, with RB2 rising to INR 8,300/t at Paradip, INR 8,350/t at Vizag and INR 8,400/t at Gangavaram, while RB3 moved to around INR 7,200/t. The increase followed stronger FOB values — RB2 at $75-76/t and RB3 at $60-61/t — supported by vessel shortages, higher February-March forward freights and steady Chinese buying. Portside stocks eased to 12.57 mnt, yet local demand remained weak, as buyers resisted higher levels. BigMint’s C-DRI index increased to INR 24,500/t, reflecting firmer steel sentiment. Prices will likely remain supported, though meaningful buying might not return until the bid-offer gap narrows.

SECL’s auction bids improves as traders face low inventories

Domestic coal prices held steady w-o-w, with 5,000 GCV at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. The recent SECL auction saw stronger bidding despite limited volumes, as traders held low stocks and competed more aggressively. SECL also withdrew the grade guidelines issued in October. The upcoming SECL auction on 20 Nov’25 is set to offer 784,000 t of non-coking coal across G3-G9 and G11 and is expected to draw firm participation amid tight spot availability.

India’s PHCC index edges up as trades close

BigMint’s PHCC index moved up by $2/t w-o-w to $213/t CNF Paradip, supported by two Australian cargo deals for 30,000 t each — one at 98.5% index and one on a 50:50 index-fixed price basis. Price indications hovered at around $213-215/t as mills noted a gradual correction. For index computation, trades received a 50% weight and selected offers/bids received 50%. Firmer met coke prices in eastern India and China’s tight coke supply provided cost support, while mixed steel demand — with BF-rebar prices at INR 47,300/t and HRCs at INR 46,500-48,300/t — kept sentiment steady but cautious.

Met coke prices firm in the east, while west holds steady

Met coke prices showed a mixed pattern, with the east recording modest gains and the west remaining stable. BF-grade met coke reached INR 31,500/t ex-Jajpur, rising INR 500/t w-o-w, supported by firmer demand and higher coking coal costs. Gandhidham remained unchanged at INR 30,000/t, while foundry-grade met coke at Rajkot moved to INR 35,700/t, up INR 200/t. A bulk trade of 25,000 t at INR 32,000/t ex-Jajpur boosted sentiment. Pig iron touched INR 32,000/t ex-Durgapur, with recent auctions closing at INR 30,850-31,450/t, drawing healthy interest.

China’s aggressive buying keeps Indian pet coke market in limbo

China’s sudden buying surge reshaped global pet coke sentiment, while India remained stuck in a bid-offer stand-off. Chinese buyers secured US- and Mexico-origin cargoes at $125-132/t CFR, expecting tariff easing. This pushed freight to multi-month highs and tightened vessel availability for November-December loadings. In India, offers held at $116-119/t CFR, but cement buyers remained firm at lower bids due to high freight and cheaper coal alternatives. Domestic sentiment remained weak as buyers preferred cautious procurement.

Refineries trim pet coke prices in Nov’25 after long rally

Indian refiners reduced pet coke prices for Nov’25 after four straight months of hikes. IOCL cut rates uniformly by INR 200/t across Koyali, Panipat, Paradip and Haldia. BPCL raised Bina to INR 15,046/t, while Kochi eased slightly to INR 12,536/t. MRPL implemented the deepest reduction of INR 400/t, taking rake supplies to INR 11,370/t. Nayara trimmed its tag by INR 50/t to INR 14,820/t, while CPCL lowered prices by INR 30/t to INR 14,530/t. These adjustments signalled easing demand and improved refinery availability.

Dry bulk coal freights strengthen on tighter vessels, firm Pacific cues

Dry bulk coal freights to India moved higher as the Pacific market turned firm, vessel supply tightened, and bunker prices rose. Panamax rates on the Australia-India route increased w-o-w to $18.39/dmt, while the South Africa-India route edged up to $15/dmt. Supramax freights from Indonesia rose to $14.72/dmt amid improved fixture activity. Higher bunker costs added upward pressure, keeping owner sentiment firm, although gains remained moderate as Indian inquiries stayed selective.

Leave a Reply