- Imported coal firm, but high offers restrict buying interest

- Weak steel demand weighs on coal market activity

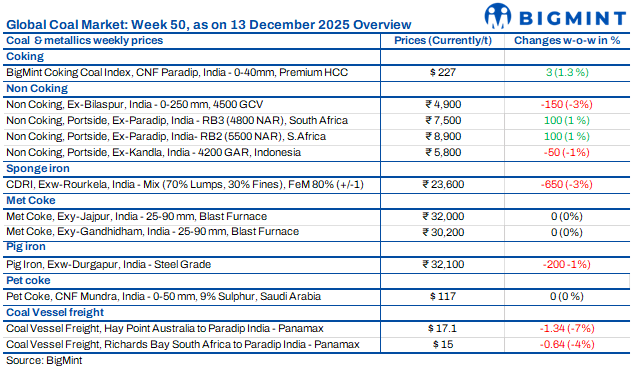

Coal markets showed divergent trends this week, with imported coal remaining firm amid supply disruptions and logistical constraints, while domestic prices softened due to heavy auction volumes and lower bids. Buyers largely stayed cautious, focusing on immediate needs rather than fresh stocking. Weak downstream demand from sponge iron and steel sectors limited buying appetite, even as quality coal continued to attract interest. Overall sentiment remained watchful, with participants expecting further adjustments before confidence improved.

Indonesian thermal coal prices weaken

Indonesian thermal coal prices softened further in the Indian market during the week ended 12 December 2025, weighed down by rising portside inventories and weak buying interest. The 4,200 GAR grade at Kandla slipped to around INR 5,800/t from INR 5,850/t earlier, while 3,400 GAR at Navlakhi corrected sharply to INR 4,400-4,650/t, with most trades discussed near INR 4,500-4,550/t, down from INR 4,600-4,650/t in late November. Heavy congestion at Navlakhi, with stocks estimated near 1 mnt, forced pressure selling. Softer Chinese demand, easing freight of $11-12/t, and fuel switching toward lignite further dampened sentiment, keeping the near-term outlook bearish.

South African thermal coal prices stay firm

South African thermal coal prices in India remained firm in the week ended 12 December 2025, even as spot buying activity stayed muted. RB2 (5,500 NAR) prices strengthened to INR 8,900-9,000/t ex-Paradip from INR 8,400-8,800/t, while RB3 (4,800 NAR) rose to INR 7,450-7,600/t from INR 7,200-7,350/t. The firmness was supported by global supply disruptions and demand from other destinations along with further currency depreciation for landed material, therefore RB2 offers reported as high as $93-94/t CFR India. However, Indian buyers largely stayed on the sidelines, citing high landed costs and better domestic alternatives, resulting in firm prices but thin trading volumes.

Domestic coal prices ease after SECL auction

Domestic coal prices declined INR 150-250/t w-o-w, with 5,000 GCV falling to INR 5,800/t and 4,500 GCV to INR 4,900/t Exw-Bilaspur. The market remained under pressure following SECL’s 12 December auction, which offered 3.2 mnt of non-coking coal and saw full clearance. However, final bid prices were lower than previous levels, reinforcing bearish sentiment. Market participants expected further near-term softening as the impact of higher auction volumes continued to weigh on prices.

US thermal coal portside prices rise

US-origin thermal coal prices at Indian ports increased by INR 250/t w-o-w to INR 10,200/t. The uptick was driven by tight domestic pet coke availability, which continued to constrain cement sector procurement. As pet coke supplies remained limited, traders and end-users increasingly turned to US thermal coal as a substitute fuel, lifting demand and supporting higher portside prices.

Coking coal index firms up on global cues

BigMint’s premium hard coking coal (PHCC) index edged up on 12 December, reflecting firmer global cues, though bid-offer gaps persisted. The index was assessed at $227/t CNF Paradip, up $3/t from 6 December. Indian mills showed limited interest for Jan’26 cargoes, with only a few enquiries reported. Australian prime cargoes were quoted higher at $230-235/t CFR India, supported by weather-related disruptions and firmer China-linked trades. However, most Indian buyers stayed cautious, placing bids $5-10/t below offers, near $220-225/t CFR. Meanwhile, China’s second coke price cut of RMB 50-55/t weighed on sentiment, limiting upside despite higher coal costs.

Met coke prices stable, sentiment cautious

India’s metallurgical coke market remained stable across regions during the week ended 10 December, as balanced supply met gradual demand. In eastern India, BF-grade (25-90 mm) met coke was assessed at INR 32,000/t ex-Jajpur, unchanged w-o-w, while western prices held at INR 30,200/t ex-Gandhidham. Foundry-grade material stayed firm at INR 36,000/t ex-Rajkot.

Market sentiment remained cautiously firm following earlier gains. Australian premium hard coking coal prices rose $4/t w-o-w to $206/t FOB, adding mild cost pressure, though domestic demand stayed neutral. In China, coke prices weakened further amid conservative buying, rising inventories, and lower blast furnace utilisation. Overall, steady Indian demand and soft Chinese trends kept prices range-bound.

Pet coke prices diverge, IOCL effects sharp cut

Indian pet coke pricing moved in different directions in December 2025 as refiners reacted to uneven supply conditions. IOCL reduced prices aggressively by INR 480-900/t across refineries, with Koyali cut to INR 12,380/t (road) and INR 12,180/t (rake), Panipat to INR 13,660/t, Paradip to INR 11,510/t, and Haldia to INR 11,680/t. In contrast, Nayara raised prices marginally to INR 14,880/t (+INR 60/t), CPCL increased to INR 14,610/t (+INR 80/t), MRPL lifted prices by INR 300/t to INR 11,740/t (rake), and BPCL raised prices by INR 27-73/t. The divergence reflected softer demand, refinery-specific availability, and RIL’s continued absence from merchant sales.

Coal freight rates decline w-o-w

Coal freight rates to India fell across key routes in the week ended 12 December, reflecting subdued cargo demand and ample vessel availability despite temporary supply disruptions. Panamax freight on the Australia-India route dropped by $1.34/dmt w-o-w to $17.10/dmt, while Richards Bay-India rates declined by $0.64/dmt to $15/dmt. Indonesia-India Supramax rates eased by $0.70/dmt to $14/dmt. The RBCT force majeure limited South African loadings but failed to lift rates due to weak buying interest. Lower bunker prices and rising open tonnage kept overall freight sentiment under pressure.

Leave a Reply