- Asian exporters benefit from healthy demand, stronger Chinese offers

- Kardemir opens fresh sales at reduced prices, sells around 100,000 t

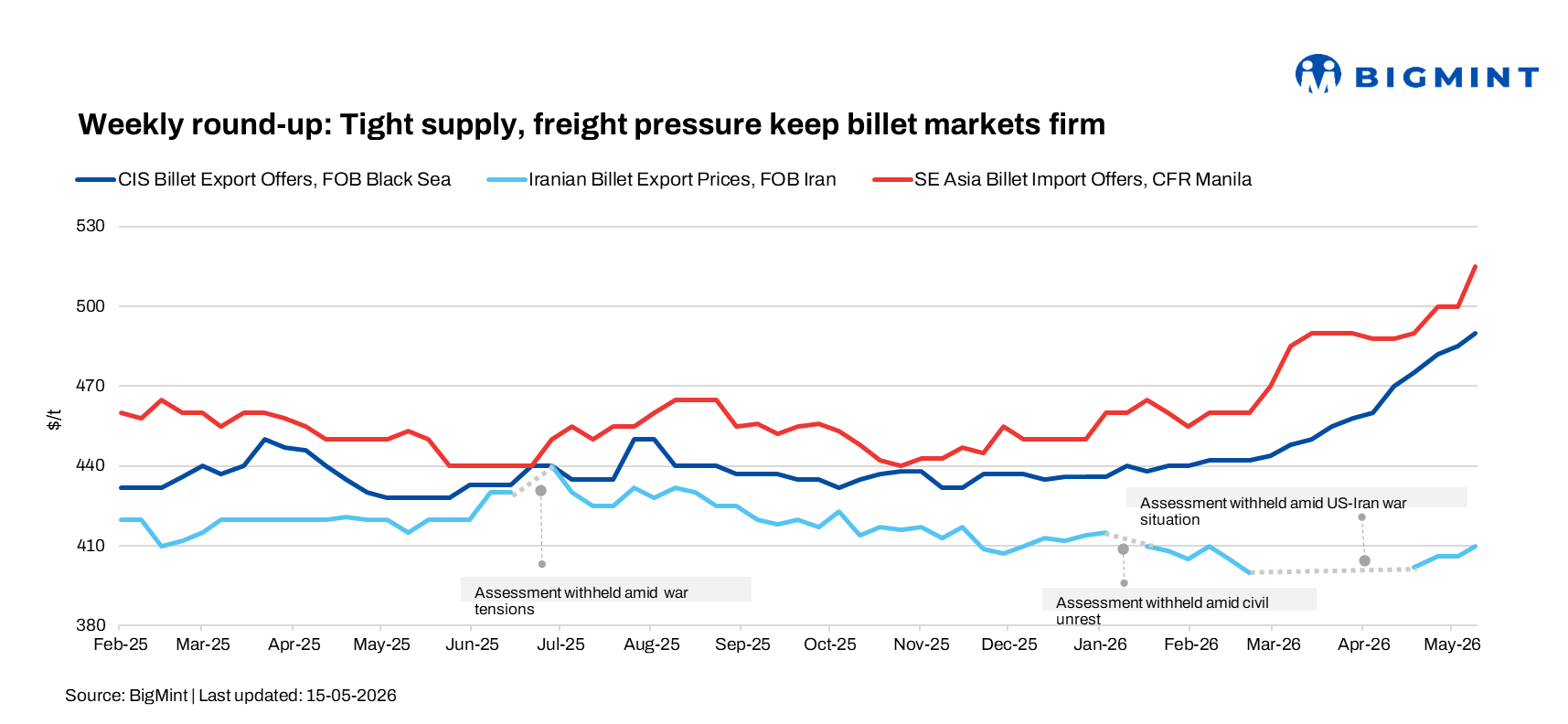

Global billet markets remained cautiously firm during the week ended 16 May 2026, supported by tight semis availability, firm scrap prices, and elevated freight costs across key export regions. CIS suppliers maintained firm offers amid limited availability, while Asian exporters benefited from healthy order books and stronger Chinese billet offers.

Meanwhile, ongoing logistics disruptions around the Strait of Hormuz continued pressuring GCC steel trade and regional shipment flows. However, weak downstream steel demand and cautious buying sentiment across major importing markets limited fresh bookings and sharper price increases.

Turkiye’s deep-sea imported scrap market remained cautiously firm during the week, supported by limited cargo availability, elevated freight costs, and firm exporter sentiment. However, Turkish mills resisted higher scrap prices as the scrap-to-rebar spread narrowed to around $177-178/t.

Turkish rebar export prices were largely heard at $590-592/t FOB, while weak finished steel demand and squeezed margins limited aggressive scrap bookings. Meanwhile, domestic billet sentiment improved after Kardemir resumed billet sales at competitive levels, although overall steel trading activity remained subdued.

CIS billet market

The CIS billet market remained firm during the week, supported by limited supplier availability, firm scrap prices, and steady exporter confidence. Russian square billet offers were heard at $490/t FOB Black Sea for late June-early July shipment.

Turkiye remained the key export destination, with CIS billet offers heard at $510-515/t CFR Turkiye, rising by $5/t w-o-w. Market participants noted that $505-508/t CFR remained the latest workable deal level, although fresh transactions stayed limited amid weak downstream rebar demand and squeezed mill margins.

Turkish domestic billet sentiment improved after Kardemir opened fresh billet sales at reduced prices and sold nearly 100,000 t within hours. Kardemir offered different billet grades at $530/t exw and $540/t exw, making domestic material more competitive compared to imported CIS billet at $510-515/t CFR and Chinese offers around $535/t CFR.

Other Turkish mills were heard offering billets at $545-550/t exw, while Iskenderun-region producers targeted around $560-565/t exw. However, overall trading activity in the semi-finished steel segment remained subdued due to weak finished steel demand.

Asian billet market

Asian billet export prices strengthened during the week, supported by firm mill order books and improved buying activity early in the week, although trading momentum slowed later amid weaker futures sentiment and cautious buyer response.

Chinese base grade billet deals were concluded at $485-490/t FOB, up by around $5/t w-o-w, while new 3sp billet offers for July-August shipment were heard at $490-495/t FOB. Market participants noted that Chinese mills maintained firm offers due to sufficient forward orders despite slower negotiations later in the week.

Indonesian steel major reportedly sold around 50,000 t of billet at $490-495/t FOB for August shipment, around $5/t higher than late-April deals. Later in the week, the producer slightly reduced September-shipment offers to $485-490/t FOB to attract fresh buying interest.

In Southeast Asia, 5sp billet offers were heard around $515/t CFR, while bids remained near $505/t CFR. Taiwanese buyers received Chinese 3sp billet offers at $505-510/t CFR, broadly stable w-o-w, although trading activity remained limited.

Philippines billet demand stayed weak amid slow construction activity and economic uncertainty, with China-origin 5sp billet offers heard at $510-515/t CFR Manila. Meanwhile, Chinese billet offers to Saudi Arabia were heard at $540-550/t CFR, although no major buying interest was reported.

GCC market

The GCC steel market remained under pressure during the week amid ongoing uncertainty around the Strait of Hormuz, which continued disrupting regional logistics, freight availability, and shipment planning. Despite renewed diplomatic discussions between Iran and the US, market participants remained cautious due to unstable maritime conditions and elevated shipping risks.

Iranian steel exporters continued offering billet cargoes, although trading activity remained inconsistent due to high freight costs, insurance restrictions, and vessel availability concerns. Gulf shipping routes continued to be treated as high-risk corridors, keeping logistics conditions volatile.

Iran also increased reliance on overland logistics, with railway cargo traffic between China and Iran rising significantly through Kazakhstan and Turkmenistan. However, rail transportation remained unable to fully replace maritime trade volumes due to limited carrying capacity and elevated logistics costs, with container freight rates reportedly reaching around $7,000/container.

In the UAE, the long steel market continued facing constrained billet availability and irregular cargo arrivals. Oman’s Salalah Steel Industries and Algeria’s Algerian Qatari Steel (AQS) recently received Emirates Conformity Assessment Scheme (ECAS) certification, expanding the list of approved billet and rebar suppliers for the UAE market amid ongoing regional supply disruptions.

Outlook

Global billet markets are expected to remain cautiously firm in the coming weeks, supported by tight semis availability, elevated freight costs, and ongoing logistics uncertainty across the Middle East and Black Sea regions. CIS and Asian suppliers are likely to maintain firm offer levels amid healthy order positions and limited supply.

Leave a Reply