- Higher input costs push steel prices upward

- Geopolitical tensions, cautious buying limit trade activity

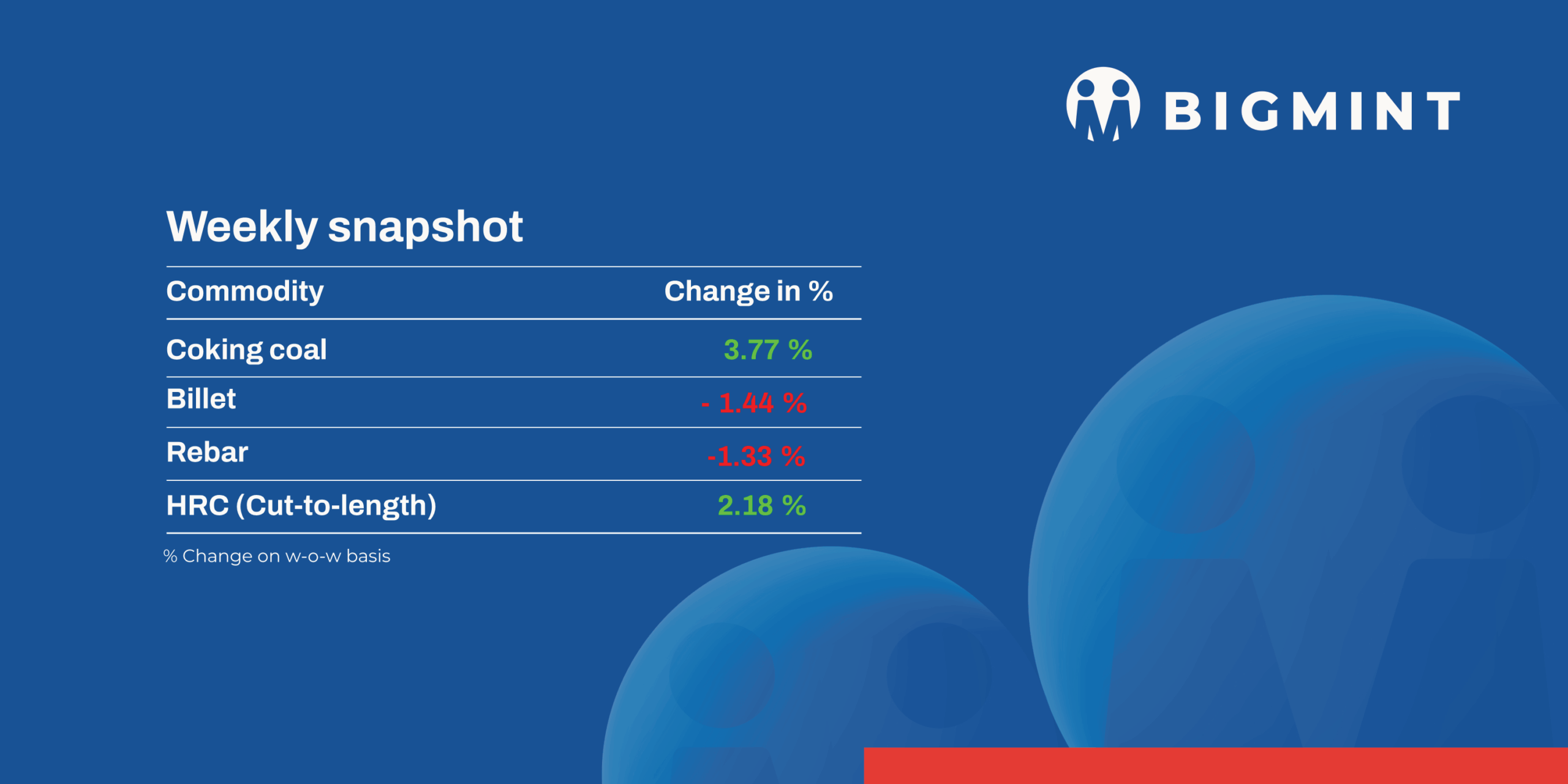

Rising input costs gave a boost steel prices this week but weak demand, geopolitical disruptions, and cautious buying weighed on overall market sentiment.

Iron ore and pellet

- On 25 March 2026, NMDC’s Chhattisgarh operations received bids for approximately 77,400 tonnes of iron ore. At the Kirandul mines, 34,400 tonnes of ROM (10–150 mm, Fe 65.5%) and an equal quantity of fines (Fe 64%) were successfully booked at base prices of INR 4,790/t and INR 4,090/t, respectively. Meanwhile, at the Bacheli mines, 8,600 tonnes of ROM (10-150 mm, Fe 65.5%) were sold at INR 4,790/t, whereas a significantly larger volume of 114,000 t of fines (Fe 60%) failed to attract buyers and remained unsold.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index rose by $1.5/t week-on-week to $63.5/t FOB east coast on 26 March 2026, supported by improved trading activity and a narrowing of discounts. Following a relatively subdued phase over the past two to three weeks largely due to ongoing geopolitical uncertainties the market has begun to regain momentum, with a noticeable pickup in spot transactions.

- SAIL auctioned a total of 40,350 t of iron ore from its Odisha mines, with the entire quantity booked by 25 March 2026. At Bolani, 20,000 t of dump fines (Fe 60.70%) were sold at INR 4,950/t, while at Taldih, 20,350 t of dump fines (Fe 53.01-54.34%) were booked at INR 2,000-2,150/t. Additionally, SAIL conducted an auction for 39,970 t of iron ore tailings (Fe 58.84–62.22%) from its Barsua mines on 23-24 March 2026, with the full volume reportedly sold at INR 4,550-5,400/t. All prices were on an ex-mines basis and inclusive of royalty, DMF, NMET, and extra premiums.

Ferrous Scrap

- India’s imported scrap market witnessed a w-o-w increase in prices, driven by sharp rupee depreciation (near INR 94/$), elevated freight costs, and ongoing supply disruptions. UK/EU-origin HMS 80:20 moved up to $370-372/t CFR, while shredded scrap rose to $390-396/t CFR, as suppliers maintained firm offers despite limited buying interest.

- Market sentiment remained subdued, with mills cautious amid high costs and weak demand. Middle East tensions tightened container supply, raised freight rates, and disrupted 20–22% of imports, pushing mills to rely more on domestic scrap.

- Around 2,000 t of imported scrap was booked during the week, including Singapore-origin HMS (bundles) at $360/t CFR Chennai and New Zealand-origin HMS (machine loaded) at $365/t CFR Chennai, reflecting selective buying amid challenging market conditions.

- Ferro alloys

- Silico Manganese: Indian silico manganese (60-14) prices went up by INR 975/t ($10/t) w-o-w to INR 74,500 -75,500/t ($786-797/t ) across Durgapur, Raipur, Vizag, and Raigarh, driven by a sharp surge in imported manganese ore prices and persistent supply tightness in the global market. Meanwhile, HC 65-16 silico manganese prices rose by $9/t to $931/t FOB Vizag/Haldia.

- Ferro Manganese: Indian ferro manganese (70%) prices rose w-o-w by INR 2,200/t ($23/t) to INR 76,700/t ($809/t) in Raipur while, went up by INR 1,500/t ($16/t) to INR 76,000/t ($802/t) in Durgapur. Prices increased as sellers were unwilling to offer material at lower rates amid rising production costs. Meanwhile, export prices for 75 grade saw a sharp increase by $22/t w-o-w to $940/t FOB Vizag/Haldia.

- Ferro Silicon: Indian ferro silicon (Si 70%) prices rose slightly by INR 3,000/t ($32/t) w-o-w to INR 103,000/t ($1,087/t) exw Guwahati, while Bhutan prices also edged up by INR 3,400/t ($36/t) at INR 103,400/t ($1,091/t). Prices were stable due to limited transactions last week, as the majority of sellers were sold out or supplying to previously booked orders.

- Ferro Chrome: Indian high-carbon ferro chrome (HC 60%, Si 4%) prices dipped slightly by INR 900/t ($10/t) to INR 117,800/t ($1,243/t) exw Jajpur. Prices fell as the majority of key buyers were absent from the market which prompted sellers to lower their offers.

Semi Finished

- India’s semi-finished steel market witnessed a mixed trend this week. Domestic billet prices declined by INR 100-600/t ($1-6/t) w-o-w across key producing regions. However, prices rose in western and southern India, supported by raw material tightness and region-specific demand variations. Overall buying interest remained subdued, as weak demand in the finished steel segment and ongoing year-end liability closures restricted market activity.

- The sponge iron market reflected mixed sentiments across the country. Pan-India prices declined by INR 250-600/t ($2-6/t) w-o-w across most regions, pressured by weak demand. However, south India witnessed relative firmness in offers due to higher raw material costs and limited material availability, which prevented sharp corrections.

- On the export front, DRI offers dropped sharply this week amid limited enquiries and weak overseas demand. Export offers to Nepal fell by $13/t w-o-w to $332/t CPT Raxaul, while offers to Bangladesh declined by $16/t to $339/t CPT Benapole. The decline was led by limited domestic sponge iron demand coupled with multiple global factors, which collectively dampened export buying interest.

Finished long steel

- IF-rebar: The IF-route rebar market exhibited a mixed trend w-o-w across major Indian markets, indicating cautious sentiment. Trading activity remained moderate, with buyers largely purchasing material at lower price levels while showing resistance to higher offers. Demand continued to be predominantly need-based, limiting aggressive bookings. Meanwhile, manufacturers maintained relatively higher offer levels, supported by prevailing cost pressures, although selective discounts were extended to facilitate transactions. Overall, despite the mixed movement, the market remained range-bound with cautious optimism.

- On a week-on-week basis, rebar prices showed mixed trends week-on-week across key regions, with movements in the range of INR 100–800/t.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 45,400-45,800/t exw Raipur, INR 51,300-52,000/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 46,500-47,000/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 44,800-45,400/t ex-Raipur.

BF-rebar: Indian primary steelmakers increased rebar prices further by up to INR 1,000/t ($11/t). Post-revision, list prices stood at INR 59,500-61,000/t ($628-644/t) on landed basis. The price hike could be attributed to rising raw material prices and input costs and falling inventories. - Trade-level BF-rebar prices (distributor to dealer) remained stable w-o-w at INR 60,000/t ($633/t) exy-Mumbai, as per BigMint’s assessment on 27 March. Enquiries were subdued in recent days due to cautious buying by end-users at higher prices and market uncertainty.

- In the projects segment, prices hovered at around INR 60,000-61,000 /t ($633-644/t) FOR basis. Mills reported healthy order bookings and continued to focus on fulfilling pending project-linked orders.

Flat steel

-

- Indian steelmakers increased list prices of hot-rolled coils (HRCs) by INR 750-1,500/t ($8-16/t) for late April sales. List prices of HRCs (2.5-8 mm, IS2062, Gr E250 Br) were reported in the range of INR 54,750-58,500/t ($583-623/t) ex-Mumbai.

- BigMint’s benchmark assessment (bi-weekly) for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) prices increased by INR 1,000/t ($11/t) w-o-w to INR 57,500/t ($612/t) on 24 March against INR 56,500/t ($601/t) on 17 March.

CRC (IS513, Gr O, 0.9 mm/CTL) prices increased to INR 65,000/t ($692/t) as assessed on 24 March 2026, up by INR 2,200/t ($23/t) w-o-w against INR 62,800/t ($668/t) on 17 March. - Indian trade-level sentiment for both HRC and CRC strengthened, with prices increasing. However, demand continues to be largely need-based, while some level of panic buying persists in the market amid supply concerns. Overall, trading activity remains limited, with a stable-to-moderate demand outlook.

- India’s bulk imports of HRCs touched 103,000 t. Around 51,213 t of additional cargoes are expected.

Bulk exports of HRCs touched 127,394 t. Around 135,600 t of additional cargoes are expected. - Indian hot-rolled coil (HRC) export activity remained largely at a standstill across key overseas markets during the week, as escalating geopolitical tensions continued to disrupt critical shipping corridors. Heightened security risks along routes such as the Red Sea-Suez Canal and the Strait of Hormuz have led to widespread vessel diversions, extended transit times, and a sharp rise in freight and war-risk insurance costs.

Leave a Reply