- HRC prices drop w-o-w

- Rebar market under pressure

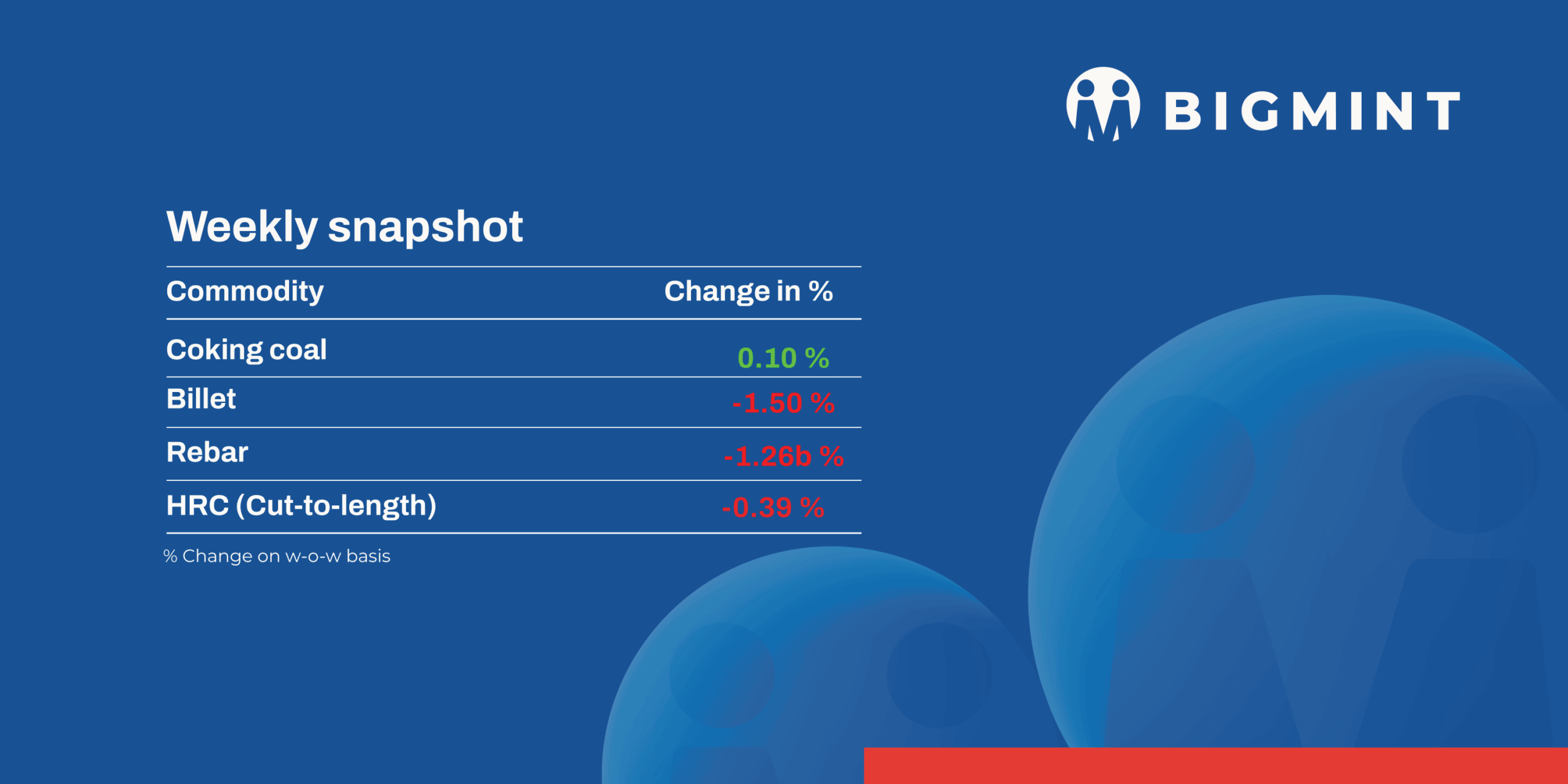

The domestic steel market witnessed a downtrend during week 40 (29 September-3 October 2025), with semi-finished steel prices registering a decline in the range of INR 100–900/tonne (t) across major trading regions. The market is expected to recover following the festive season.

Iron ore, pellet

BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $2.5/t w-o-w to $66/t FOB east coast on 1 October. With Chinese buyers remaining absent due to the week-long holiday (1-8 October), trading activity in the seaborne market slowed significantly, leaving exporters with limited avenues to conclude fresh deals.

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index (FOB east coast) dropped by $3.5/t w-o-w to $102.5/t on 1 October. There were no export deals concluded in the sea market this week. A few suppliers offered higher-grade cargo, but these remained unsold.

KSMCL conducted an auction for 199,996 t of iron ore from its mines in Bellary, Karnataka, on 30 September. Out of the offered quantity, 56,000 t was booked consisting of 28,000-t lumps (10-40 mm, Fe 62.27-63.03%) at INR 5,151-5,212/t and 28,000 t fines (Fe 61.51-62.54%) at INR 4,560-4,636/t (base prices). Prices are exclusive of royalty, DMF, and NMEDT.

Coal

Domestic coal offers moved higher this week, with 5,000 GCV assessed at INR 6,250/t ex-Bilaspur and 4,500 GCV at INR 5,300/t, up by INR 400-500 w-o-w. The hike followed strong premiums fetched in SECL’s recent auction, where sponge grade coal attracted robust bids. The upward revision was further reinforced by SECL’s new mandate requiring financial coverage for coal quality upgradation under the e-auction system, prompting sellers to lift offers. However, no major deals have been finalised yet, as buyers await clarity on the impact of these reforms.

South African portside coal offers in India stayed stable this week, with RB2 at INR 8,200/t and RB3 at INR 7,100/t across Vizag and Gangavaram. Market activity remained muted due to the festive season, though participants expect trade flow to revive from next week as activity gradually resumes.

India’s met coke market held steady during the week ending 1 Oct’25. BF-grade (25–90 mm) was assessed at INR 29,500/t ex-Jajpur, while prices in western India stayed at INR 30,000/t ex-works Gandhidham. Foundry-grade material stood at INR 35,600/t ex-Rajkot. Market activity was muted amid holidays, though Australian PHCC inched up $3/t to $190/t FOB. In China, mills raised coke by RMB 50–75/t ($7–10.5/t), while India’s pig iron market stayed cautious, limiting near-term met coke demand.

Ferrous scrap

India’s imported scrap market remained largely muted throughout the week, with price offers holding steady across origins. Shredded scrap was quoted around $360/t CFR, HMS 80:20 near $330-335/t, busheling at $370-375/t, and PNS at $360–370/t, though workable bids were consistently below these levels.

Market sentiment was weighed down by sluggish finished steel demand, cheaper domestic scrap (about INR 1,500-1,800/t lower than imports), and seasonal disruptions from monsoon rains. The Dussehra holidays further slowed trading activity, with most mills staying on the sidelines and preferring to delay fresh bookings.

Sponge iron trials by mills, coupled with limited liquidity and cautious procurement strategies, added to the subdued tone. Sellers held offers firm, but weak buying interest and festival-related slowdowns kept trading volumes thin, leaving the Indian import scrap market quiet for yet another week.

Ferro alloys

- Silico Manganese:Indian silico manganese prices (60-14) rose by INR 450/t ($5/t) w-o-w to INR 69,800-70,300/t ($786-792/t) in the key regions of Durgapur, Raipur, and Vizag. Heavy rains disrupted transport and tightened supply, while steady demand pushed prices higher across key production regions.

- Additionally, State-owned MOIL has raised prices of all ferro grades by 6.4% and SMGR grades (Mn30%, Mn25%) by 5.2% m-o-m, effective 01 October, 2025.

- Ferro Manganese:Indian ferro manganese (HC 70%) prices stayed mostly steady, with slight decline by INR 200/t ($2/t) w-o-w to INR 70,400/t ($793/t) exw in Durgapur. While, prices, exw-Raipur, stayed flat at INR 70,300/t ($792/t) w-o-w. Stable demand, balanced supply, and limited spot trades kept ferro manganese prices mostly steady this week.

- Ferro silicon:Indian ferro silicon prices stayed unchanged w-o-w and stood at INR 88,300/t ($995/t) exw-Guwahati. Meanwhile, Bhutanese remained unaltered at INR 88,000 ($991/t). The market remained largely subdued as participants awaited this month’s price announcement.

- Ferro chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices remained unchanged w-o-w at INR 118,700/t ($1,337/t) exw-Jajpur. Prices held firm, with sellers maintaining firm offers while buyers remained cautious.

Semi-finished

- Indian semi-finished steel prices showed a declining trend, as per BigMint’s assessment. Domestic billet prices across key locations fell by INR 100–900/t ($1–10) amid weak finished steel demand, compelling sellers to lower offers to stimulate buying. Sponge iron prices also declined by INR 100–600/t ($1–7) across regions, as limited buyer inquiries and cautious market sentiment continued to weigh on prices. The ongoing weakness reflected subdued confidence among both buyers and sellers, keeping overall trade activity muted.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 5,000 t of steel-grade pig iron on 29 September, with the entire quantity booked at an average price of INR 31,350/t (by road). However, management approval is still pending. Bids fell by INR 300/t from the previous auction on 18 Sep for 10,000 t, in which the entire quantity was booked at an average of INR 31,650/t (by road).

- Indian DRI (Direct Reduced Iron) export offers increased by $6 stood at CPT Raxaul, at $335/t while, CPT Benapole offers seen increased by $9/t and stands at $346/t.

Finished long steel

- IF-rebar: The induction furnace route steel rebar market remained sluggish as festivals and heavy rainfall slowed down trading, causing inventories to build up of over 12 days. However, with the monsoon season ending and construction activities expected to restart, industry participants believe that prices will improve in the near term.

- On a weekly basis, rebar prices declined in the range of INR 200-1,100/t across regions. The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 39,000-39,400/t exw Raipur, INR 42,800-43,400/t exw Jalna.

- Trade reference prices of heavy structural steel for base size 150mm channel stands at INR 41,200-41,600/t exw Raipur.

- Trade reference prices of wire rod are hovering at INR 39,400-40,000/t ex Raipur.

- BF-rebar: India’s trade-level blast furnace (BF) rebar prices rose w-o-w across major markets. Prices witnessed an uptick amid market optimism and expectations of price hike by the major primary mills for October sales.

- Trade-level BF rebar prices rose by INR 400/t ($5/t) w-o-w to INR 47,200/t ($532/t) exy-Mumbai on 3 October. Prices are exclusive of GST at 18%. In the projects segment, prices hovered between INR 45,500-46,500/t ($512-524/t) FOR Mumbai.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India fell w-o-w to INR 47,400-50,000/t ($534-563/t). Additionally, cold-rolled coil (CRC) prices showed a slight downtrend w-o-w, with prices ranging between INR 54,000-58,300/t ($608-656/t).

- The Indian HRC market continued to face sluggish conditions, with buying limited to immediate requirements and restocking activity remaining scarce. Distributors, on the other hand, prioritised steady sales flow, choosing to close deals quickly to avoid losing customers. Additionally, festive holidays such as Durga Puja weighed on trade activity.

- India’s bulk imports of HRCs touched 434,637 t as of 27 September, based on vessel line-up data. Around 208,371 t of additional cargoes are expected by mid-October.

- India’s bulk exports of HRCs touched 140,901 t as of 27 September, and around 63,820 t of additional cargo are in transit.

- BigMint’s India hot-rolled coil (HRC, SAE 1006) export index for the Middle East and Vietnam fell by $10/t w-o-w to $490/t as of $500/t last week. A deal was heard concluded for October sales to the Middle East, indicating improved demand in the region from the infrastructure sector. While some sectors may be experiencing a slowdown, significant government-backed construction initiatives are still driving demand for steel products in key areas of the region.

- India’s HRC (S275) export index for Europe held steady w-o-w at $545/t FOB main port amid sluggish domestic demand, with the market quiet due to weak end-user demand and regulatory uncertainty.

Leave a Reply