- IF rebar prices decline as buyers wait for price corrections

- Bids decline at OMC’s iron ore auctions after base price cut

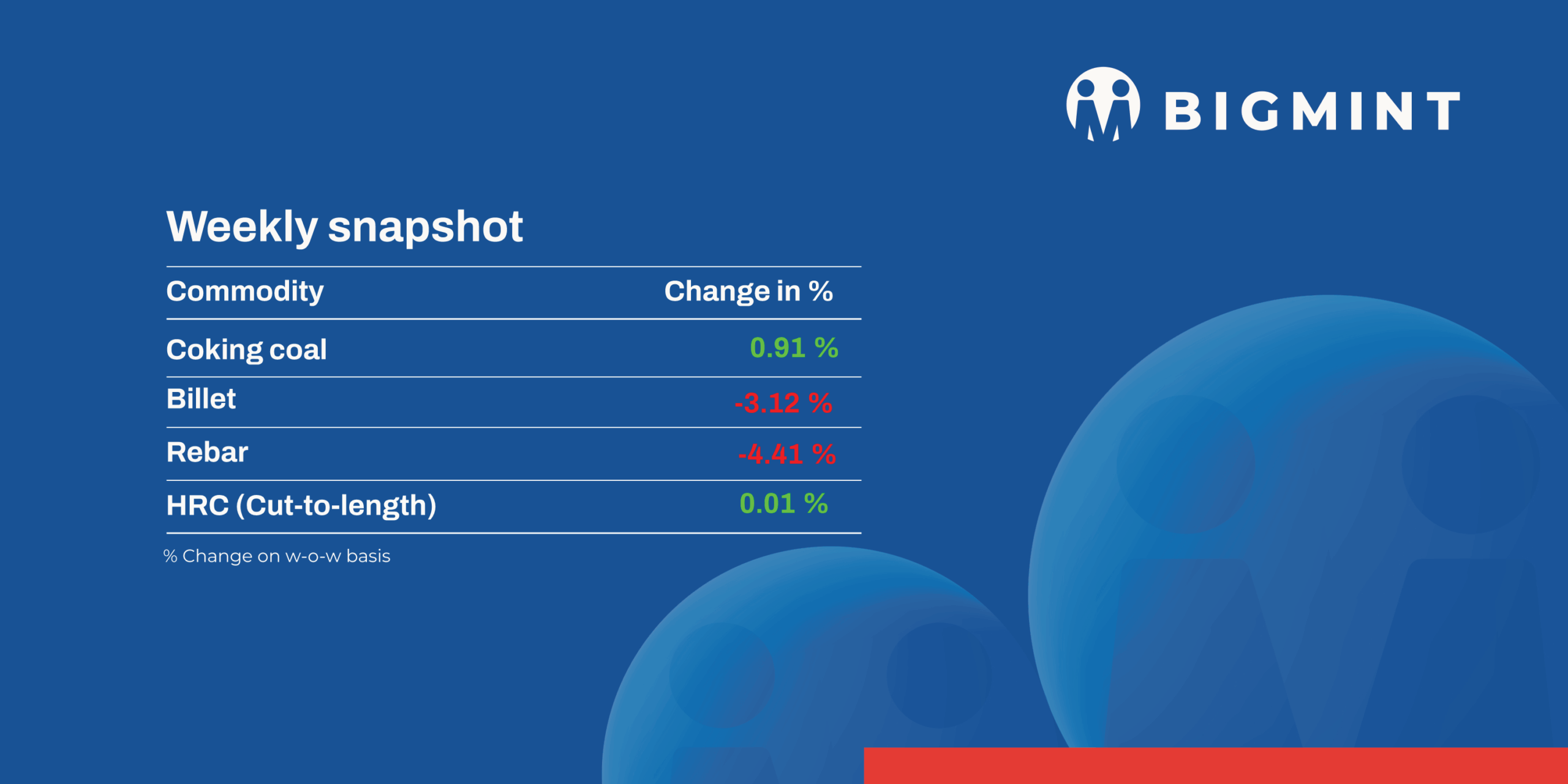

Weak steel demand and falling finished steel prices deepened pressure across India’s steel and raw materials market in the week ended 23 May 2026, dragging down prices of iron ore, scrap and metallics, ferro alloys, and long steel products as buyers limited purchases to immediate requirements.

Iron ore, pellet

- The Odisha Mining Corporation (OMC) witnessed subdued bidding sentiment in its 20 May iron ore auctions due to weak sponge iron and semi-finished steel market conditions. In the lumps auction, 1.24 mnt (95%) of the offered quantity were booked, while weighted average bids dropped by INR 900/t m-o-m amid a reduction of INR 150-1,100/t in base prices. Similarly, in the fines auction, 1.374 mnt (70%) material was booked, with weighted average bids declining by INR 700/t m-o-m after OMC lowered base prices by INR 200-900/t.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, fell by INR 300/t ($3/t) to INR 9,600/t ($100/t) DAP on Friday as compared to last week. Raipur-based pellet producers reduced their offers in response to weak demand and falling raw material prices. However, despite the correction in offers, market inquiries remained limited, and no aggressive trades were heard in the market. Traders and suppliers noted that buyers are largely adopting a wait-and-watch approach amid expectations of further corrections in pellet prices.

- NMDC Chhattisgarh’s auction on 21 May witnessed bookings for 81,400 t of iron ore. At Bacheli, 25,800 t of DR CLO (10-40 mm, Fe 67%) received a premium of INR 800/t over the base price of INR 6,200/t, while 4,000 t of lumps (10-20 mm, Fe 65.5%) were booked at a premium of INR 1,100/t above the base price of INR 5,650/t. Meanwhile, at Kirandul, 51,600 t of fines (Fe 64%, FOR basis) were sold at INR 4,740/t, whereas 68,000 t of fines remained unsold.

- Lloyds Metals and Energy Limited has reduced its offers for iron ore fines and pellets in Chandrapur, Maharashtra, in response to weak domestic market sentiment and sustained pressure across the steel value chain. Offers for Fe 63% iron ore fines were reduced by INR 300/t ($3/t) compared to the previous revision in April, taking the current level to INR 6,350/t ($66/t) FOR Balharshah as of 22 May. Pellet offers were at INR 10,000/t ($105/t) exw. Notably, the company had increased its offers in the last revision announced on 6 April 2026.

Coal

- South African thermal coal sentiment remained subdued in the week ending 22 May 2026 amid weak sponge iron demand, comfortable domestic coal availability, and cautious industrial procurement. Buyers largely avoided aggressive imported coal bookings despite firm global coal indices and higher freight costs. Ex-Paradip RB2 (5,500 NAR) prices increased INR 100/t w-o-w to INR 11,450/t, while RB3 (4,800 NAR) remained stable near INR 9,800/t. FOB offers for 5,500 NAR coal were heard around $96-97/t, while freights from Richards Bay Coal Terminal (RBCT) to Vizag stayed near $23/t. Port inventories declined 4.5% w-o-w to 15.16 mnt, although overall stock levels remained comfortable.

- Domestic coal prices remained under pressure amid weak sponge iron and steel demand, along with comfortable coal availability through frequent CIL auctions. BigMint assessed 5,000 GCV coal prices lower by around INR 500/t w-o-w, while 4,500 GCV material declined around INR 200/t to nearly INR 4,100/t as on 22 May 2026. Market participants stated that buying activity largely remained requirement-based, while lower auction premiums and stable domestic supply continued reducing urgency for imported coal procurement across key industrial regions.

- India’s BF-grade metallurgical coke prices remained largely stable amid balanced supply-demand dynamics and firm import parity. Ex-Jajpur BF-grade coke prices increased marginally by INR 300/t w-o-w to INR 36,700/t, while ex-Gandhidham prices remained stable at INR 33,500/t. Indonesian-origin BF-grade coke was assessed stable around $302/t CFR India following improved sentiment after DGTR’s proposal to reduce anti-dumping duty. Meanwhile, Australian PHCC prices increased $8/t w-o-w to $241/t FOB Australia, continuing to support global coke costs. Pig iron prices increased marginally, although downstream buying sentiment remained cautious amid fluctuating steel demand.

- India’s Ministry of Steel urged the Ministry of Finance to reconsider and withdraw anti-dumping duty on imported metallurgical coke amid concerns over limited domestic availability and rising steelmaking costs. The ministry stated that RINL faced difficulty procuring met coke at competitive prices, resulting in nearly 20% higher input costs and affecting operational viability. Smaller steelmakers also remain impacted due to dependence on merchant suppliers.

- US-origin NAPP thermal coal continued strengthening its position in India’s cement fuel mix amid better delivered-cost economics compared with imported petcoke. US 6,900 NAR coal was heard around low-to-mid $130s/t CFR west coast India, while imported petcoke remained higher near $147-152/t CFR. Portside US 6,900 NAR coal at Kandla increased INR 100/t w-o-w to INR 13,500/t. Cement producers increasingly focused on fuel flexibility and cost optimisation, while buying activity remained selective ahead of the monsoon season. Retail lifting declined during the week, reflecting cautious procurement sentiment across the cement sector.

- Market sentiment in the Indonesian coal segment also remained influenced by Indonesia’s proposed export policy reforms aimed at gradually shifting coal exports under State-Owned Enterprises (BUMN). Although implementation is now expected from 2027, Indian importers remained watchful regarding possible changes in export procedures, pricing flexibility, and spot cargo availability. However, participants largely expect major supply disruptions to remain unlikely due to India’s strong dependence on Indonesian coal imports.

Ferrous scrap

- The imported scrap market remained weak throughout the week amid sluggish steel demand, a weak rupee, and poor import viability, with buyers largely resisting higher offers. Market participants noted that imported scrap trade parity remained near INR 95-96 against the US dollar, further pressuring buying sentiment and limiting fresh bookings.

- Malaysia-origin HMS 80:20 deals were heard around $350/t CFR Chennai, while Malaysia-origin turnings were sold near $340/t CFR. South America-origin LMS bundles were heard at around $335/t CAD, while West Africa-origin HMS 80:20 offers stood at $350-365/t CFR and Australia-origin HMS 80:20 near $365/t CFR Chennai.

- Higher-grade imported scrap offers continued facing resistance, with UK-origin shredded scrap heard at $390-415/t CFR, HMS at $360-375/t CFR, and busheling near $425-430/t CFR, while buyers stayed cautious, expecting further downside.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices continued to fall by INR 1,050/t ($11/t) w-o-w to INR 73,800-74,600/t ($771-780/t) across key markets. The market stayed subdued during the week as weaker steel prices and constrained liquidity reduced buying interest, prompting buyers to avoid large-volume deals. Meanwhile, smelters kept offers mostly stable within a limited range despite continued weak sentiment.

- Meanwhile, HC 65-16 silico manganese export prices were down by $29/t to $883/t FOB Vizag/Haldia.

- Ferro manganese: Indian ferro manganese (70%) prices dipped w-o-w by INR 1,100/t ($11/t) to INR 76,800/t ($803/t) in Raipur and decreased by INR 900/t ($9/t) to INR 77,000/t ($805/t) in Durgapur. Ferro manganese prices declined due to limited bulk enquiries, slow market activity, and suppliers lowering offers to encourage transactions.

- Meanwhile, export prices for the 75% grade declined by $26/t w-o-w to $874/t FOB Vizag/Haldia.

- Ferro silicon: India ferro silicon (Si 70%) prices fell by INR 1,700/t ($18/t) w-o-w to INR 103,800/t ($1,085/t) ex-works Guwahati, while Bhutan prices also went down by INR 1,600/t ($17/t) to INR 103,000/t ($1,076/t). Indian ferro silicon market sentiment weakened as suppliers offered bulk discounts, while limited buyer interest and sellers’ focus on fulfillment of bookings kept trading activity subdued.

- Ferro chrome: India high-carbon ferro chrome (HC 60%, Si 4%) prices inched up by INR 1,000/t ($10/t) w-o-w to INR 120,000/t ($1,247/t) ex-works Jajpur. Sentiment remained cautious as market participants awaited the outcome of major domestic auctions for clearer price direction.

- At the Odisha Mining Corporation (OMC) chrome ore auction on 20 May, around 96,400 t were booked against 131,800 t offered. Bids and premiums across grades increased by up to 6%, supported by restocking ahead of the monsoon season, when chrome ore supply typically tightens.

Semi-finished

- India’s semi-finished steel market remained under pressure this week, with spot prices witnessing a sharp correction across the regions amid subdued buying interest and weak downstream demand. As per BigMint’s assessment, billet prices declined by INR 400-1,700/t w-o-w, with the sharpest fall recorded in the western region’s Jalna market, where prices dropped by INR 1,700/t. Market participants largely restricted procurement to immediate requirements, while overall trading activity remained weak due to lower finished steel demand across domestic markets.

- Meanwhile, sponge iron prices also continued their downward trajectory, falling by INR 400-1,200/t ($1-10/t) across all major regions during the week. The steepest correction was observed in the Durgapur market amid limited enquiries and muted trade activity. Although manufacturers initially attempted to maintain price stability, persistent weakness in finished steel demand and poor buyer participation continued to exert pressure on the market. Procurement activity remained largely need-based, while traders continued to offer material at lower prices in line with prevailing bearish market sentiment.

- On the export front, Indian DRI offers remained firm with minor fluctuations this week. Export offers to Nepal edged lower by $1/t to $320/t CPT Raxaul, while offers to Bangladesh remained steady at $328/t CPT Benapole. Buying activity from Nepal stayed limited, whereas enquiries from Bangladesh remained subdued ahead of the upcoming Eid festival.

Finished long steel

- IF-rebar: IF rebar trade prices declined across major markets this week amid subdued trading activity and weak market sentiment. Demand remained sluggish, with buyers restricting purchases to immediate requirements due to cautious sentiment and expectations of further price corrections.

- To support sales and improve material movement, producers reduced offers and provided additional discounts, while mill inventories were at around 12-15 days. In the near term, market participants expect price volatility to persist amid weak bookings and continued pressure in the finished steel segment.

- On a w-o-w basis, rebar prices declined by INR 400-1,800/t across key regions, with the sharpest drop observed in the Raipur market, according to BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 41,500-41,900/t exw Raipur and INR 45,700-46,300/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 44,400-44,800/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 42,500-43,000/t ex-Raipur.

- BF-rebar: Trade-level BF rebar prices (distributor-to-dealer) fell by INR 700/t ($7/t) w-o-w to INR 56,800/t ($487/t) exy-Mumbai, according to BigMint’s assessment on 22 May 2026. Buying activity remained moderate across key regions, while demand in southern markets continued to stay relatively weak, as per market sources. Stable raw material prices provided cost support to BF-route steel producers despite weak market demand.

Flat steel

- BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.58 mm/CTL) was stable w-o-w at INR 58,700/t ($612/t) as of 22 May against the previous week.

- However, CRC (IS513, Gr O, 0.9 mm/CTL) prices decreased by INR 500/t ($5/t) to INR 65,000/t ($678/t) on 22 May from INR 65,500/t ($683/t) on 15 May.

- India’s bulk imports of HRCs touched 169,172 t on 15 May. Around 138,586 t of additional cargoes are expected by early-June.

- India’s bulk exports of HRCs touched 69,541 t on 15 May. Around 53,356 t of additional cargoes are expected to be shipped.

- Indian HRC export markets showed a mixed regional trend in the week ended 20 May, with offers to the EU remaining absent amid continued regulatory uncertainty and tighter safeguard expectations.

- Indian HRC export offers to the Middle East resumed this week after months of limited market activity, with offers heard at around $550-560/t FOB.

Leave a Reply