- Pellet exports, scrap imports, and semi-finished markets remained subdued.

- Alloy prices diverged while long steel demand stayed cautious nationwide.

Iron ore and pellet

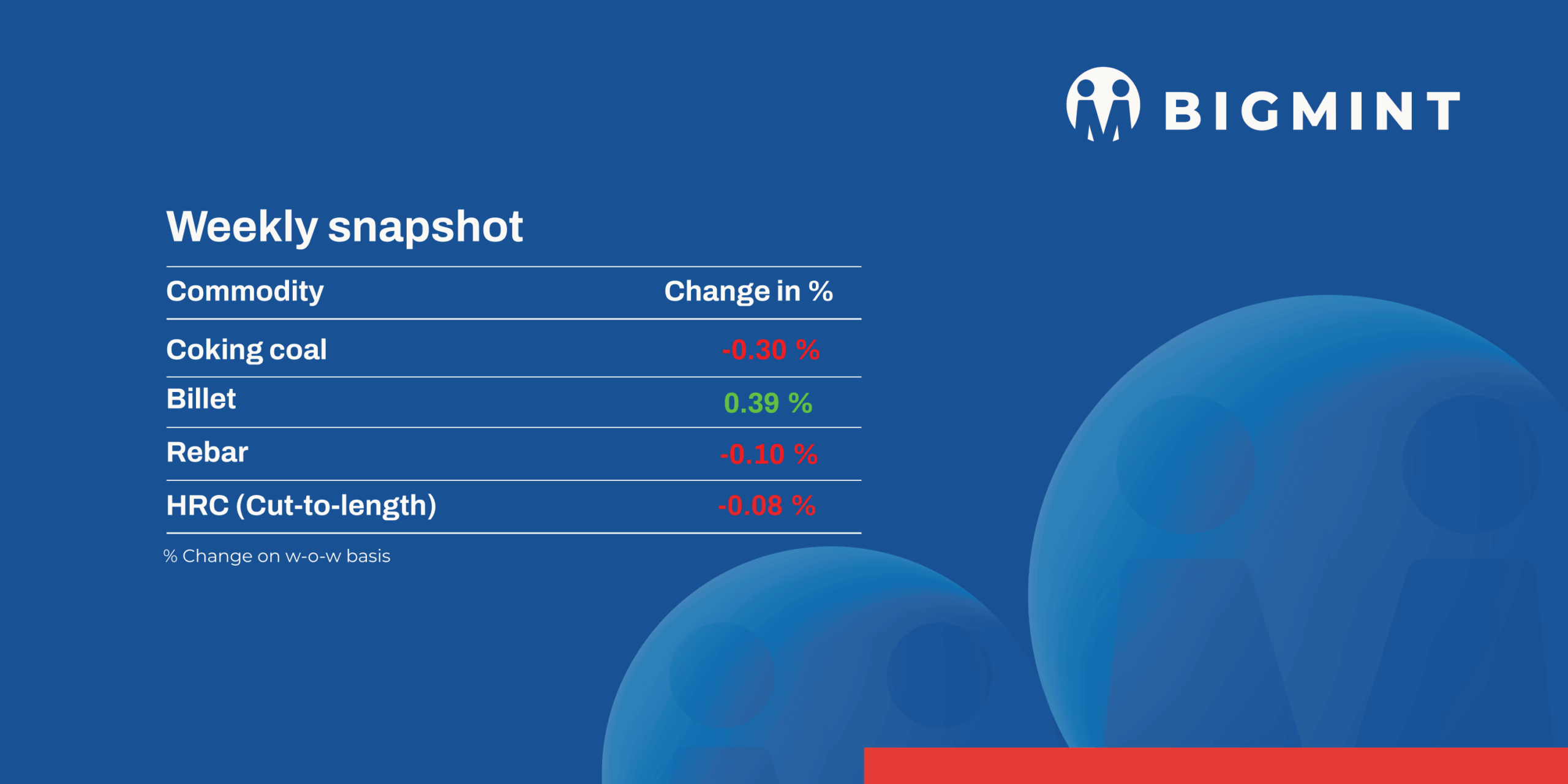

- BigMint’s India pellet export index (Fe 63%, 3-3.5% Al) declined by $4/t w-o-w to $98/t FOB east coast on 10 June 2026. Export market activity remained subdued as falling global prices, cautious buyer sentiment, and uncertainty over iron ore prices and Chinese raw material inventories weighed on trade. Indian exporters largely refrained from offering material due to the widening gap between buyer bids and seller expectations.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, increased by INR 200/t ($2/t) w-o-w to INR 9,600/t ($101/t) DAP, as pellet manufacturers in Raipur raised offers for Fe 62.5/63% (+/-0.5%) grade pellets by INR 200/t ($2/t) to INR 9,400-9,500/t ($98-99/t) exw after NMDC increased prices of iron ore fines and lumps by INR 150-200/t last week.

- During SAIL auctions held in this week, around 56,000 t of iron ore (Fe 59.5-62%) was booked at prices ranging between INR 3,850-6,275/t. The prices were on an ex-mines/FOR loaded into rake basis, inclusive of royalty, DMF, NMET, and additional premium charges.

In KSMCL’s auction from Karnataka on 9 Jun, 120,000 t lumps (10-40 mm, Fe 61.32-62.66%) got booked at INR 5,076-5,538/t and 118,000 t fines (Fe 62.12-62.41%) got booked at INR 4,263-4,294/t ex-mines, exclusive of royalty, DMF and NMET.

Ferrous Scrap

- Imported ferrous scrap market remained subdued during the week, with weak steel demand and poor mill margins continuing to restrict buying activity. Buyers largely stayed on the sidelines, targeting HMS 80:20 around $340-345/t CFR, while workable levels for UK-origin HMS were heard closer to $3350-355/t CFR. A few spot deals were reported, including Brazil-origin HMS 80:20 (2% impurities) at $325/t CFR Mundra, UK-origin shredded scrap at $405/t CFR Mundra, and Malaysia-origin turnings at $340/t CFR Chennai.

- The persistent gap between buyer bids and supplier offers continued to limit fresh bookings. Offer indications for UK-origin HMS 80:20 (3% impurities) were heard around $360/t CFR India, while Philippines-origin GI bundles were offered at $345-347/t CFR. Market participants noted that suppliers increasingly preferred selling to Southeast Asian and Bangladeshi buyers, where prices were typically $15-20/t higher than those achievable in India.

- In the last seven days, India imported a total of 3,500-4,000 t of ferrous scrap, comprising 1,500 t of HMS, 2,000 t of shredded scrap followed by turning scrap.

Ferro alloys

- Silico Manganese:Indian silico manganese (60-14) prices increased by INR 750/t ($8/t) w-o-w to INR 75,200-76,000/t ($785-793/t) across key markets on limited offers. Prices rose on stronger buying interest from traders and steel mills, while bulk deals concluded at higher levels improved market sentiment and supported upward price movement. Meanwhile, HC 65-16 silico manganese export prices rose by $12/t to $918/t FOB Vizag/Haldia.

- Ferro Manganese:Indian ferro manganese (70%) prices rose w-o-w by INR 600/t ($6/t) to INR 79,000/t ($825/t) in Raipur and by INR 700/t ($7/t) to INR 79,000/t ($825/t) in Durgapur. Prices increased as sellers resisted lower bids amid limited spot availability and firm production costs, prompting buyers to accept slightly higher transaction levels. Meanwhile, export prices for the 75% grade also went up by $10/t w-o-w to $922/t FOB Vizag/Haldia.

- Ferro Silicon:India ferro silicon (Si 70%) prices fell by INR 3,400/t ($36/t) w-o-w to INR 95,100/t ($993/t) ex-works Guwahati, while Bhutan prices also went down by INR 2,900/t ($30/t) to INR 95,700/t ($999/t). Prices fell as inquiries remained slow, and buyers delayed purchases, expecting further price drops. Material availability was also heard to be sufficient, with more inflows from Bhutan.

- Ferro Chrome:India high-carbon ferro chrome (HC 60%, Si 4%) prices remained staedy with slight rise by INR 300/t ($3/t) w-o-w to INR 122,500/t ($1,279/t) ex-works Jajpur. Prices remained stable as steady export demand and balanced domestic buying were offset by firm seller offers, keeping prices range-bound.

Semi finished

- India’s semi-finished steel market displayed a mixed trend this week, as per BigMint’s assessment. Domestic billet prices across key regions declined by INR 50-450/t ($0.5-5.7/t) w-o-w, while southern markets remained stable to marginal gains this week. Market participants highlighted the trend due to rising operational cost and freight costs, which encouraged sellers in several regions to maintain offer levels despite weak demand from end users. Buyers, however, continued to seek lower-priced procurement opportunities, influenced by competitive pricing in neighbouring markets, which impacted recent purchasing patterns.

- The sponge iron market also witnessed mixed price movement during the week. Pan-India sponge iron prices declined by INR 100-400/t ($1-4/t) w-o-w due to limited buying activity. A wide bid-offer gap between buyers and sellers restricted trade volumes, as buyers pushed for lower bids amid unsupportive finished steel demand conditions.

- On the export front, Indian DRI offers weakens further this week amid limited bookings from neighbouring countries, mostly concluded at lower price levels. Export offers to Nepal declined by $4/t w-o-w to $306/t CPT Raxaul, while offers to Bangladesh fell by $5/t to $311/t CPT Benapole.

- SAIL-RSP auctioned 5,000 t of steel-grade pig iron on 10 Jun’26, with only 1,100 t of the offered quantity booked at an average price of INR 37,100/t exw. Bids declined marginally by INR 50/t from the previous auction held on 2 Jun’26. In the earlier auction, the entire 3,400 t offered quantity was booked at INR 37,150/t exw. The sharp decline in booking volumes despite largely stable prices indicates cautious procurement activity and persistent pressure on pig iron demand.

- NMDC’s Nagarnar Steel Plant auctioned 12,000 t of steel-grade pig iron on 10 Jun’26, with only 3,100 t booked at the base price of INR 36,000/t ex-works. Prices remained unchanged from the previous auction held on 2 Jun’26, when the entire 12,000 t offered quantity were sold. The sharp decline in offtake suggests subdued buying interest, amid weak downstream demand and uncertain market conditions.

Finished long steel

- IF-rebar: IF-route rebar trade prices weakened across major markets this week amid subdued trading activity and weak buying interest. Buyers continued to procure material on a need-based basis, resulting in slow bookings in both finished and semi-finished steel segments and keeping sentiment cautious. Although sellers attempted to hold prices, sluggish demand and limited acceptance at higher offers forced them to lower prices and offer discounts to maintain sales momentum. Mills reported sales at around 50-70% of production, while inventories across most regions stood at 10-15 days. Dispatches of previously sold material remained smooth despite the weak market conditions. Going forward, prices are expected to remain under pressure amid subdued demand, cautious procurement, and the onset of the monsoon season.

- On a week-on-week basis, rebar prices declined by INR 50–1,000/t across key regions, with the sharpest decline of INR 1000/t observed in the Rourkela region, according to BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10–25 mm size) were assessed at INR 41,300–41,700/t exw Raipur and INR 45,000–45,600/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 43,600–44,000/t exw Raipur.

- Trade reference prices of wire rod stood at INR 42,600–43,100/t exw Raipur.

- BF-rebar:BF-route rebar sentiment remained bearish as trade-level prices declined to INR 52,900/t exy-Mumbai, while project deals were heard at INR 51,000-52,000/t landed. Distributor inventories rose to 25-30 days, intensifying selling pressure and keeping procurement strictly need-based.

Flat steel

- BigMint’s bi-weekly benchmark assessments for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) remained stable w-o-w at INR 58,300/t ($612/t) as of 12 June against previous week. Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) remained stable w-o-w at INR 65,200/t as of 12 June.

- India’s trade-level HRC prices remained stable w-o-w amid weak demand and cautious buying. Approaching monsoons and muted market sentiment kept procurement restrained despite quantity discounts from steel majors.

- India’s bulk imports of HRCs touched 41,308 t as on 5 June. Around 121,692 t of additional cargoes are expected by early-July.

- India’s bulk exports of HRCs touched 59,956 t as on 5 June.

- Indian HRC export activity remained subdued, with weak demand from Europe amid safeguard quota uncertainty and muted buying from the Middle East due to geopolitical tensions, high freight costs, and shipping disruptions.

Leave a Reply