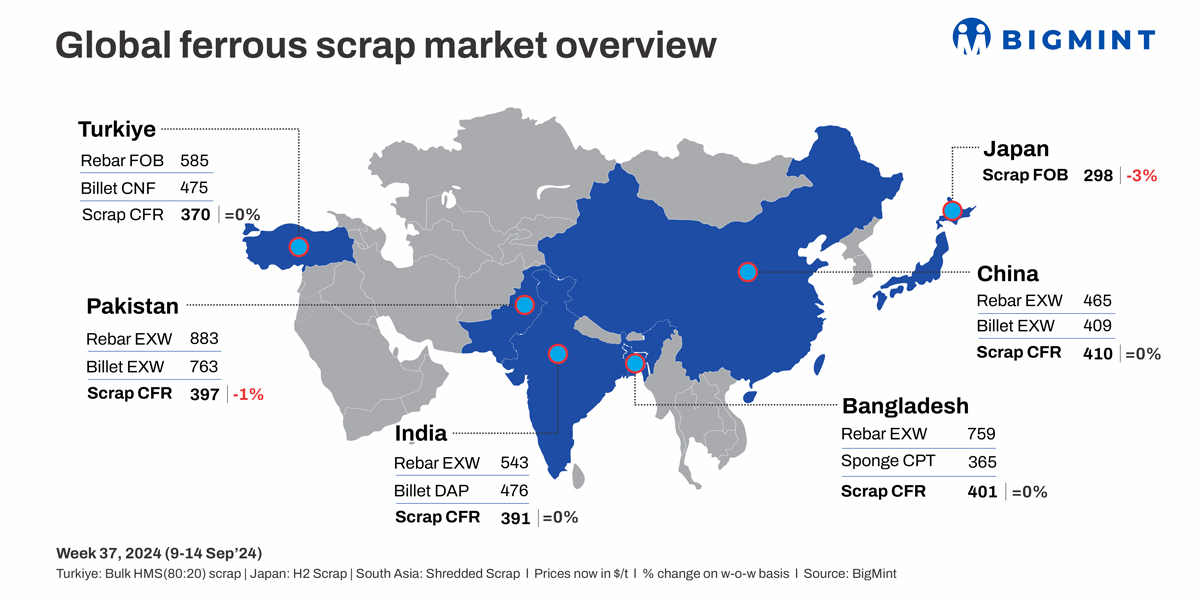

This week, the global ferrous scrap market experienced notable shifts, with Turkiye witnessing stability in import prices against the backdrop of falling billet prices and cautious buyer sentiment.

In the South Asian markets such as India, Pakistan, and Bangladesh, activity was subdued due to weak demand and financial challenges. Indian buyers preferred cheaper domestic alternatives, while Pakistan’s market was hampered by sluggish steel sales and monsoon-related disruptions. Bangladesh faced delays in banking processes and reduced construction activity.

Meanwhile, Japanese H2 scrap prices plummeted to their lowest in nearly two years, driven by weak demand from traditional markets and ongoing price cuts by domestic suppliers.

Turkiye: The Turkish imported ferrous scrap market exhibited stability, driven by consistent demand and stable long steel prices, despite caution due to falling billet prices. This situation created a balancing act between sellers aiming to maintain margins and buyers seeking better deals.

Turkish mills are currently facing scrap shortages but have secured bulk cargoes from US suppliers at stable prices $370/t CFR for HMS (80:20) and $390/t for shredded scrap. Although sellers remain firm and buyers have been retreating, and there is slight downward pressure on prices due to lower European domestic scrap prices.

The scrap-to-rebar spread stood at $215/t, allowing mills to focus on scrap while maintaining favorable margins.

The market is in a holding pattern with no significant price shifts expected in the short term.

India: The imported scrap market in India had been subdued, with buyers showing little interest due to the availability of cheaper domestic alternatives. Imported shredded scrap had been priced between $385-390/t CFR Nhava Sheva, while HMS (80:20) ranged from $365-370/t CFR.

Weak steel demand and falling prices had led mills to delay purchases and priorities local scrap. Traders faced narrow margins, often selling at a loss. Many mills were also burdened with high inventories and sluggish sales of finished steel, further dampening market activity. As a result, Indian buyers continued to prefer domestic scrap due to its cost advantage and the uncertain outlook for imports.

During the week, around 2,500 t of scrap were booked, including 2,000 t of shredded scrap from the UK at $398/t CFR and around 500 t of HMS (80:20) scraps from West Africa at $360-365/t CFR.

Pakistan: Pakistan’s demand for imported scrap has remained moderate this week, due to sluggish domestic steel sales, worsened by the off-season monsoon rains and squeezed profit margins. Offers for shredded scrap from the UK and Europe have held steady at $395-$405/t CFR Qasim.

The market has been slow due to reduced government projects leading to weak steel demand and lower scrap consumption. Steel mills are dealing with excess rebar inventory resulting in production cuts and lower scrap purchases.

Traders are encountering challenges with limited buyer activity and profitability concerns. As domestic conditions subdued, mills are focusing on clearing their existing inventory before resuming scrap purchases.

In the domestic market, local scrap prices stood at PKR 145,000-150,000 /t, while rebars were priced at PKR 245,000-250,000 /t, depending on payment terms.

Bangladesh: This week, the imported scrap market in Bangladesh remained subdued due to seasonal factors and ongoing banking challenges. Demand was dampened as buyers struggled with severe financial difficulties, including delays in opening letters of credit (LCs) following recent changes in banking regulations, coupled with a sluggish steel market.

Indicative offers for shredded scrap from the UK/Europe were around $401/t CFR Chattogram, while HMS (80:20) offers were approximately $390/t CFR.

The imported ferrous scrap index declined w-o-w, influenced by weak bulk scrap interest and falling prices. Limited construction activity and financing issues, particularly among smaller mills, have further reduced scrap consumption. Major steel mills are postponing new scrap purchases due to adequate inventory while smaller mills continue to face difficulties with LCs.

Market activity is expected to improve by mid-October as the impacts of the monsoon disappear and hamper projects potentially resume.

Vietnam: Demand for Japanese scrap in Vietnam has softened due to weak market conditions and in anticipation of further reductions in domestic scrap prices in Japan. H2 scrap offers to Vietnam have dropped to $347-350/t CFR, but buyers are bidding lower, around $330-335/t. This bid-offer gap indicates limited buying interest from Vietnamese mills, who are hesitant to accept higher-priced offers amid sluggish demand and competition from cheaper alternatives such as US-origin containerised scrap.

Japan: Japanese H2 scrap export offers plummeted to their lowest in nearly two years, dropping from JPY 52,100/t ($371/t) FOB Tokyo Bay in mid-July to JPY 42,000/t ($299/t) FOB. This decline, marked by nine consecutive weeks of falling prices, reflects weak demand from traditional markets and ongoing price cuts by Tokyo Steel, which has also reduced domestic scrap procurement prices by JPY 4,000-5,000/t ($28-36/t) in September. The appreciation of the Japanese yen against the US dollar has further pressured export prices.

South Korea: In South Korea, demand for Japanese scrap is weak. South Korean mills have shown little interest in Japanese scrap due to a slow construction market and high inventory levels. Offers for H2 scrap from Japan are not attracting bids, as mills are avoiding high-priced spot market bids and focusing on cheaper alternatives, such as Russian scrap, for which deals were recently heard at $335/t CFR.

This week, the combined ferrous scrap inventory of eight major South Korean steel mills touched 690,000 tonnes (t), marking a fall of 2.4% from 707,000 t seen a week back. Notably, domestic steelmakers’ scrap inventory has declined for the first time in three weeks, primarily due to the upcoming Chuseok holiday shutdown.

Leave a Reply