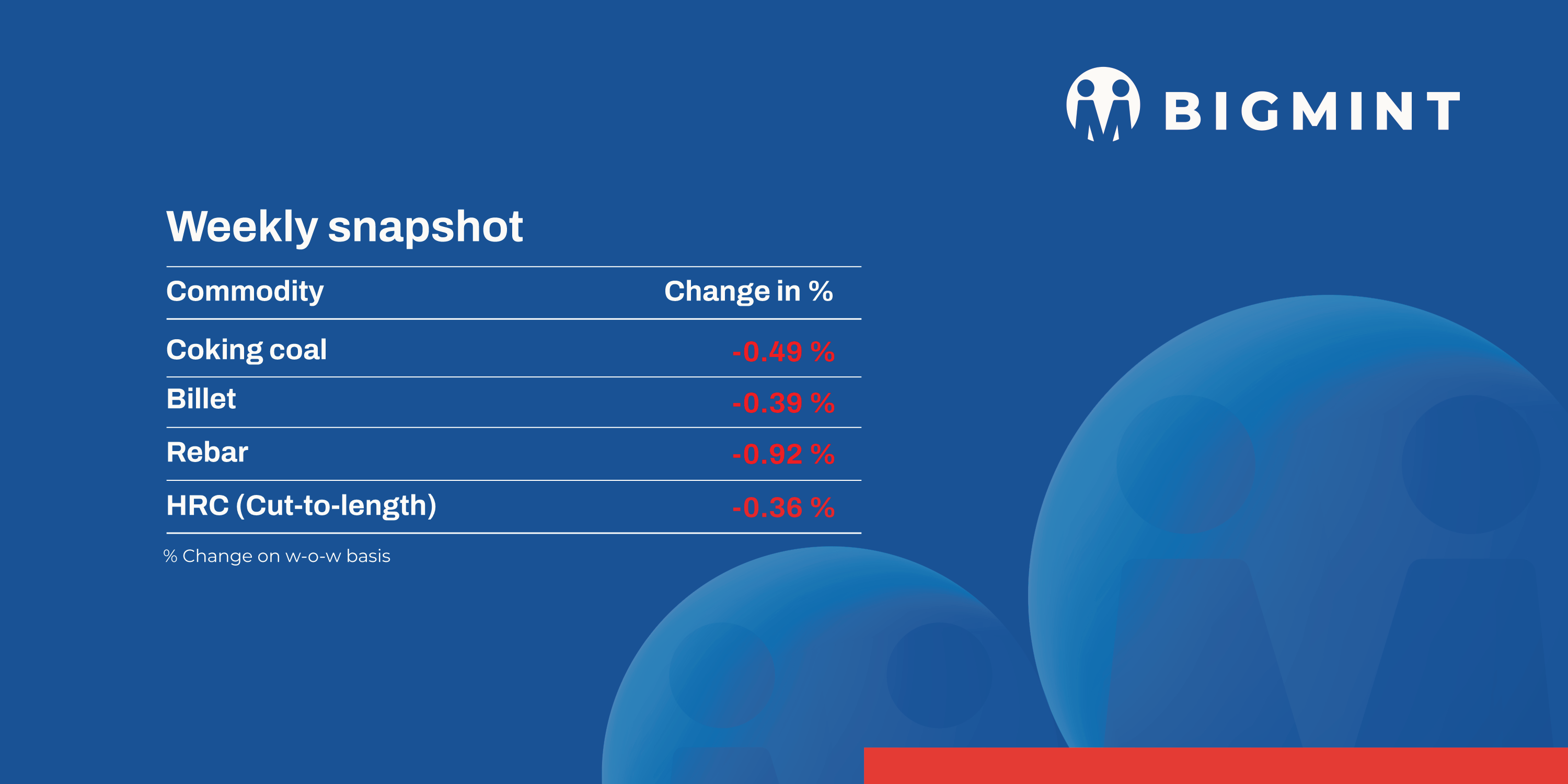

Prices of semi-finished and finished long steel produced via induction furnaces dropped by INR 100-1,600/t w-o-w, while ferro alloys showed an uptrend, rising up to INR 1,100/t.

Iron ore and pellet

- OMC conducted an auction for 2.353 mnt of iron ore (1.025 mnt of lumps and 1.328 mnt of fines) on 19 May. Around 0.508 mnt (38%) fines (Fe 55-65%) from different lots were booked at the base prices within the range INR 4,100-5,500/t ex-mines while 1.017 mnt (99%) were booked at INR 5,500-8,150/t, with premiums of 2-17% over the base prices. Bids (weighted average) dropped INR 100/t m-o-m, but lumps bids remained stable m-o-m. The miner reduced base prices by INR 50-100/t ($0.5-1/t) and INR 450/t ($5/t) m-o-m for fines and lumps, respectively.

- BigMint’s bi-weekly domestic pellet (Fe63%) index fell by INR 300/t ($4/t) w-o-w to INR 9,400/tonne (t) ($110/t) DAP Raipur on 23 May. Raipur-based pellet producers reduced offers for Fe 62/63% (+/- 0.5%) INR 9,100-9,300/t ($107-109/t) exw. Around 80,000 t trade took place this week in the Raipur region.

- NMDC auctioned 163,400 t of iron ore from its Bacheli mines on 22 May. Around 21,500 t of DR CLO (10-40 mm, Fe 67%) were booked at INR 7,480/t, i.e., 2.9% premium against a base price of INR 7,270/t. While 141,900 t of fines (-10 mm, Fe 64%) were left unsold. Prices include royalty, DMF, and NMET.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index remained stable w-o-w at $62/t FOB east coast, India, on 22 May. Exporters dealing in Fe 57% fines reportedly offered discounts of 20-21% compared to the global index, which is largely similar to last week. They were pointed to an overall positive trend, with deals for nearly 430,000 t concluded during the recent price rally. However, few deals are yet to be confirmed from the selling parties.

Coal

- Portside RB2 (5500 NAR) fell by INR 350/t to INR 7,900/t at Gangavaram, while RB3 dropped INR 250/t to INR 6,900/t. Prices hovered at four-year lows amid weak buying interest and surplus availability. Export offers also declined by $1/t as demand across markets remained subdued.

- Portside Indonesian coal prices declined w-o-w on low demand and monsoon disruptions. At Kandla, 5000 GAR dropped by INR 50/t to INR 7,750/t; 4200 GAR fell by INR 100/t to INR 6,100/t. Global 4200 GAR slipped by $1.18/t to $47.46/t. Market sentiment remained bearish amid limited procurement.

- Domestic coal prices held steady, with 4500 GCV at INR 4,350/t and 5000 GCV at INR 4,800/t exw-Bilaspur. Weak spot market activity continued as buyers preferred auction-linked or direct power plant supplies. SECL’s latest auction saw muted response with just 0.19 mnt coal booked, reflecting demand pressure.

- Met coke prices held steady this week across key regions, with BF-grade (25–90 mm) assessed at INR 32,300/t ex-Jajpur and INR 31,000/t exw-Gandhidham. Despite a $9/t rise in Australian coking coal since mid-April, coke prices in the domestic (India) market remained under pressure due to weak steel demand. China’s coke prices dropped amid surplus supply.

Ferrous scrap

- India’s imported scrap market remained largely subdued throughout the week, as buyers resisted higher offers due to weak finished steel demand and sufficient availability of lower-cost alternatives like sponge iron and pellets. UK/Europe-origin shredded scrap prices stood at $367/t CFR Nhava Sheva, reflecting a marginal 1% drop from last week’s $369/t, with bids mostly at $360-365/t and limited concluded trades.

- Pakistan-bound scrap cargoes were diverted to India due to emergency shipping surcharges, adding short-term supply pressure. However, Indian mills stayed cautious, focusing on inventory control and weak steel margins. HMS 80:20 offers held at $345-355/t CFR, but mills were only interested at lower bid levels.

- Approximately 44,000 t of imported scrap were booked in India this week, including a 31,000 t US bulk cargo at Kandla with shredded, HMS 80:20, and bonus. Container deals covered HMS 80:20, shredded, and mixed grades like PNS, busheling, and bundles

Ferro alloys

- Silico manganese: Indian silico manganese prices jumped by INR 1,100/t ($13/t) w-o-w to INR 71,100-72,200/t ($832-845/t) in the key regions of Durgapur, Raipur and Vizag. The price rise was fuelled by constrained supply, leading buyers to secure material quickly, often agreeing to pay higher rates to ensure timely procurement

- Ferro manganese: Indian ferro manganese (HC 70%) prices rose by INR 400/t ($5/t) w-o-w to INR 72,300/t ($846/t) exw in Durgapur. Meanwhile, prices, exw-Raipur inched up by INR 50/t ($1/t) to INR 72,300/t ($846/t). Prices had trended upward due to supply shortages and production cuts affecting overall market availability and stability.

- Ferro silicon: Indian ferro silicon prices declined by INR 600/t ($7/t) w-o-w settling at INR 94,100/t ($1,101/t) exw-Guwahati. Meanwhile, prices in Bhutan stood at INR 95,000/t ($1,112/t) exw, down by INR 300/t ($4/t) . Prices may remain steady short-term, but a minor correction remains a possible market movement ahead.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices saw a slight decline of INR 100/t ($1/t) w-o-w to INR 100,300/t ($1,174/t) exw-Jajpur. Prices held steady w-o-w as market participants paused activity following the recent conclusion of OMCs’ chrome ore auction.

- Additionally, At Vedanta-FACORs ferro chrome auction yesterday, the bigger lot of 10-150 mm achieved an H1 tag of INR 100,300/t exw, above the base price of INR 99,500/t. Compared to the previous 28 Apr25 auction, prices saw a slight uptick of INR 800/t m-o-m.

Semi-finished

- Indian semi-finished steel prices showed a mixed trend as per BigMint’s assessment. Domestic billet prices in all key locations decreased by INR 50-600/t across regions Except Ahmedabad region showed up by INR 500/t. Similarly, sponge iron prices also showed downward trend, almost all key locations moved down by INR 50-600/t, with a major decrease of INR 600/t seen in the Durgapur region.

- Indian DRI (Direct Reduced Iron) export offers decreased by $4 for CPT Raxaul to $335/t while, CPT Benapole offers decreased by $5 to $340/t.

- SAILs Rourkela Steel Plant (RSP) conducted an auction for 8,000 t of steel-grade pig iron on 19 May in which 1,900 t was booked at a base price of INR 32,000/t exw. This shows a decline of INR 800/t compared to the previous auction on 13 May in which 1,500 t was sold at INR 32,800/t exw.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for 2,000 t on 22 May. The entire quantity received bids at an average of INR 32,600/t against a base price of INR 32,000/t. However, management approval is still pending. In the previous approved auction, held on 14 May, out of 10,000 t, 4,500 t were booked (by road) at an average price of INR 32,500/t.

Finished longs

- IF-rebar: India’s induction furnace route rebar remained under pressure this week, with prices declining. Overall, trading activities remained subdued w-o-w across regions. The onset of heavy rainfall in the key regions of western and southern India further impacted market movement, prompting increased caution among participants. Buyers largely restricted purchases to immediate needs and avoided bulk bookings. Meanwhile, sellers were burdened with slightly elevated inventories of around 10–12 days due to sluggish sales, compelling them to reduce prices further. Given the current market conditions, prices are likely to remain range-bound in the near term.

- On a weekly basis, in rebar steel prices witnessed declined in the range of INR 100-1,500/t across the regions, as per BigMint assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 43,000-43,400/t exw Raipur, INR 46,900-47,500/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 44,800-45,300/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 43,300-43,800/t ex Raipur.

- BF-rebar: Trade-level blast furnace (BF) rebar prices witnessed downtrend w-o-w across key Indian markets owing to dull domestic demand and weak sentiment. The prevailing uncertainty led market participants to adopt a cautious approach and stay on the sidelines.

Trade-level BF rebar prices dropped by INR 400/t w-o-w to INR 56,000/t exy-Mumbai, as per BigMint’s assessment on 23 May 2025. Prices are exclusive of GST at 18%.

In the projects segment, prices continued to fall w-o-w to around INR 54,000-55,000/t FOR Mumbai amid need-based trade activities. Buyers were cautious regarding the procurement of material amid market uncertainty and weak sentiment.

Flats

-

- Trade-level prices of hot-rolled coils (HRCs) fell up to INR 200/t ($2/t) w-o-w, to INR 51,100-53,000/t ($600-622/t) across markets. Cold-rolled coil (CRC) prices showed mixed trend w-o-w, to INR 56,600-61,500/t ($664-722/t).

- Market demand has started to decline with the onset of the monsoon season, as several regions have already begun experiencing rainfall.

- India’s bulk imports of HRCs and plates touched 1,71,834 t as of 19 May, based on vessel line-up data from BigMint. Also its expected that 24,238 t is expected by months end.

- Export offers for Indian Hot Rolled Coil (HRC) grade S275 to the European Union (EU) declined by $10/t week-on-week, now quoted at $630–635/t CFR Antwerp ($580–585/t FOB eastern Indian port), compared to last week’s $640–645/t CFR. Despite the price correction, trading activity in the region remained limited.

- Meanwhile, Chinese HRC offers to the Middle East (ME) remained within a narrow range due to the seasonal summer slowdown in demand. Japan, however, secured bookings for HRC shipments to the region scheduled for late July. Indian mills have refrained from actively offering to the ME market, citing stiff competition from Chinese suppliers and more attractive domestic realisations.

Leave a Reply