The domestic steel market experienced a seesaw trend in prices during week 36 (2-7 September, 2024). Semi-finished steel prices fluctuated within a range of INR 50-400/tonne (t).

Iron ore, pellet

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, fell by INR 150/t w-o-w to INR 8,650/t DAP Raipur on 30 August. Around 59,000 t of pellet (Fe62.5-63%) deals were recorded in the Raipur region this week. Raipur-based pellet makers have reduced their offers for Fe 63%(+/_0.5%) by INR 300/t ($2.5/t) to INR 8,600/t ($102/t) exw-Raipur.

- BigMint’s weekly Indian low-grade iron ore fines (Fe 57%) export index decreased by $7.5/t w-o-w to $51/t FOB East Coast on 5 September. Iron ore prices fell sharply in the overseas market this week following the continuous drop in the global fines spot and futures prices. BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB East Coast) significantly decreased by $11.5/t w-o-w to $83.5/t on 6 September and no pellet export deal was recorded in the last one week amid the downtrending market sentiments.

- NMDC held an auction for 320,000 t of iron ore on 31 August, 2024 from its Kumaraswamy mines. Around 96,000 t of lumps (10-40 mm, Fe 64.74-65.04%) were booked at INR 5,844-5,964/t against base price of INR 4,744-4,804/t while 216,000 t of fines (Fe 59.95-65.94%) were booked at INR 3,212-5,384/t against base price of INR 3,202-4,234/t. Prices were on ex-mines basis.

- Asia-Pacific Supramax dry bulk (50,000-55,000 t) freight rates for iron ore vessels from the East Coast of India to China inched down by $0.14/t w-o-w, reaching $12.8/t as of 5 September

Coal

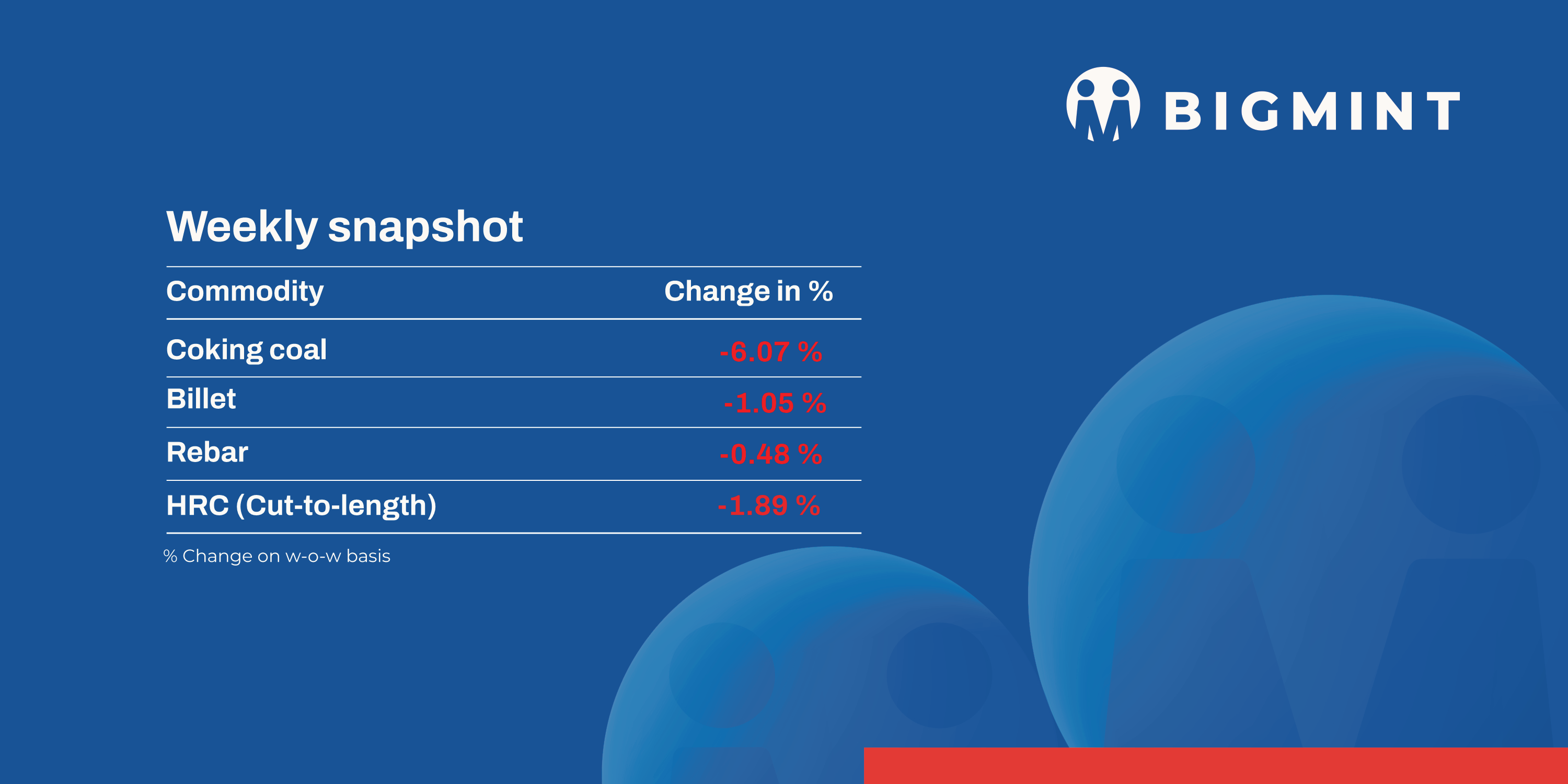

- Australian coking coal prices were corrected downwards by $13 w-o-w to $185, FoB Australia. Fall in futures along with demand concerns in China weighed on offers.

- Domestic met coke prices in India declined this week due to low demand and global market cues. Prices dropped by INR 100/t to INR 34,100/t ex-works Jajpur, while western India saw a decline of INR 500/t to INR 30,800/t ex-works Gandhidham.

- BigMint’s assessment indicated that portside prices of South African thermal coal have fallen by INR 100-300/t w-o-w. RB2 (5500 GAR) and RB3 (4800 GAR) coal prices were assessed at INR 9,450/t and INR 7,600/t ex-Gangavaram, respectively. Trades remained subdued due to bid-offer disparities and weak steel demand.

Ferro scrap

- The imported scrap market in India continued to face sluggish demand during the week, driven by a significant gap between bids and offers, along with the seasonal slowdown in the domestic steel market during the monsoon season. Shredded scrap offers were quoted between $385-395/t CFR Nhava Sheva while HMS (80:20) were at $364/t, but buyers remained largely inactive, pushing for lower prices amid weak finished steel demand and high inventory levels.

- Despite these challenges, suppliers and traders are cautiously optimistic, suggesting that prices may have nearly bottomed out, with hopes for a potential demand boost after mid-September as weather conditions improve and winter approaches.

- Additionally, market sentiment has been influenced by the possibility of future regulations requiring automakers to recycle steel from older vehicles. Starting financial year 2026 (FY’26), India could mandate that 8% of steel from vehicles sold since 2005 be recycled, which may significantly impact long-term scrap market dynamics.

Ferro alloys

- Silico manganese: Silico manganese prices remained under pressure with decline of around INR 900/t ($11/t) w-o-w to INR 66,700-67,100/t ($794-799/t) exw in Raipur, Durgapur and Vishakhapatnam. Domestic silico manganese prices in India edged down w-o-w amid falling raw material prices and limited demand in domestic steel mills.

- Ferro manganese: India’s ferro manganese (HC70%) prices inched down by around INR 600/t ($7/t) in Raipur to INR 73,000/t ($869/t) exw w-o-w. Meanwhile, in Durgapur, prices inched down by around INR 400/t ($5/t) w-o-w to INR 73,000/t ($869/t). Prices were largely stable as the market did not witness any significant change and remained cautious with the purchases.

Ferro silicon: Indian ferro silicon (FeSi:70%) prices remained largely stable with a slight fluctuation, up by around INR 2,000/t ($24/t) w-o-w to settle at INR 87,900/t ($1,047/t) ex-works Guwahati on 6 September. However, prices in Bhutan inched down slightly by INR 800/t($10/t) w-o-w, reaching INR 88,000/t ($1,048/t) ex-works. Bhutan’s offer for this month was announced at INR 88,000/t ($1,048/t) exw, so prices stayed at those levels.

Ferro chrome: Prices of Indian high-carbon ferro chrome (HC60%, Si:4%) inched down by INR 400/t ($5/t) w-o-w on 6 September, reaching INR 106,600/t ($1,269/t) ex-works Jajpur. The price consistency was driven by the market’s continued acceptance towards offers and the execution of routine trades.

Semi-finished

- Indian semi-finished steel prices showed downtrend as per BigMint’s assessment. Domestic billet prices in almost all key locations decreased by INR 50-400/t across regions, with a major decrease of INR 400/t seen in the Raipur and Ahmedabad markets. Similarly, sponge iron prices also decreased in almost all key locations by INR 50-500/t, with a major decrease of INR 500/t seen in the Bellary market.

- SAIL-Durgapur Steel Plant (DSP) held an auction for 2,500 t of steel-grade pig iron on 6 September. The entire quantity received bids at an average price of INR 35,150/t ex-works. In the previous auction, held on 23 August, the entire quantity of 2,500 t of steel-grade pig iron was booked at an average price of INR 35,500/t ex-works.

- Indian Direct Reduced Iron (DRI) export offers decreased by $1 for CPT Raxaul, reaching $345/t while, CPT Benapole offers decreased by $4 to $361/t.

Finished long steel

- IF-rebar: India’s induction furnace (IF) route finished long steel witnessed minor fluctuation in prices w-o-w. Average trades were observed this week as buyers procured need-based material for restocking material. However, they steered clear of bulk bookings until further clarity on the market direction owing to constant variation in offers and volatility at the moment. A similar trend in steel billets further led to the current scenario. As per the participants, sellers might try to raise offers post-hike in prices announced by primary mills, however, market is likely to remain range-bound in the near-term owing to limited buying interest at higher offers at the moment.

- On a weekly basis, in rebar steel prices saw a mixed response by up to INR 500/t across the regions except few markets were stable as per BigMint’s assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 41,100-41,500/t exw Raipur and INR 44,400-45,000/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 43,400-43,900/t exw Raipur.

- Trade reference prices of wire rod were hovering at INR 41,400-41,900/t ex Raipur.

- BF-rebar: Indian tier-1 mills have increased list prices of rebars by up to INR 1,000/t for early-September 2024 deliveries. Post-revision, list prices are hovering in the range of INR 50,500-51,500/t on a landed basis. Following this, trade-level BF-rebar prices witnessed increase across major markets. Despite of price hike, demand in traders’ market remained dull. Current week’s rebar prices (12-32mm) in the trade segment rose by INR 300/t w-o-w to INR 50,600/t exy-Mumbai, excluding 18% GST.

- In the projects segment, prices are hovering in the range of INR 49,000-50,000/t landed Mumbai basis. Buyers have been postponing their purchases and procuring on a need-only basis.

Finished flat steel

- Major public sector units (PSUs) have announced a reduction in the list prices for hot rolled coils (HRCs) and cold rolled coils (CRCs) by approximately INR 1,000-2,000/t ($12-24/t), effective 1 September.

- Reports indicated that some leading private mills may also lower their prices by INR 1,000-1,500/t or maintain current levels, though confirmation from these mills is still awaited.

- BigMint’s bi-weekly benchmark assessment shows a decrease in HRC (IS2062, Gr E250, 2.5-8mm) prices by INR 1,000/t ($12/t), to INR 49,000/t ($584/t) as of September 3. CRC (IS513, Gr O, 0.9mm) prices also fell by INR 900/t ($11/t), to INR 56,400/t ($672/t) for the same period. The quoted prices are ex-Mumbai, excluding 18% GST, for cut-to-length (CTL) deliveries (INR 1 = USD 0.0119116; USD 1 = INR 83.952).

- According to BigMint’s vessel line-up data, the cumulative import volume for August 2024 reached 627,426 t, compared to 636,651 t in July. An additional 331,092 t are projected to arrive in the first half of September.

- Domestic supply of HRCs remains robust due to a growing preference for cost-effective import alternatives and procurement based on specific needs. The market is currently well-stocked with both domestically produced and imported HRCs.

- India’s export volumes have experienced a decline, attributed to competitive pricing from other exporting countries such as China, Vietnam, Japan, and South Korea. Exports to Southeast Asia (SEA), the Middle East (ME), and the European Union (EU) have diminished due to subdued demand.

Leave a Reply