The domestic steel market saw fluctuating trend in prices during week 23 ( 3-8 June, 2024). Semi-finished steel prices fluctuated wildly in the range of INR 50-500/tonne (t).

Iron ore and pellets

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, decreased by INR 400/t w-o-w to INR 10,600/t DAP Raipur on 7 June. Around 27,000 t of deals in pellets (Fe63-66%) were recorded in the Raipur region in the last one week. Pellet-buying interest in Raipur remained muted post-parliamentary election results. Buyers remained cautious about purchasing as they had already stocked up enough for the next few weeks.

- BigMint’s weekly Indian low-grade iron ore fines (Fe 57%) export index fell sharply by $9.5/t w-o-w to $57/t FOB east coast on 6 June 2024. No active deals were witnessed this week as exporters remained sidelined in a declining market. Prices have fallen significantly, with an exporter from Odisha selling 55,000 t of Fe57% iron ore fines at $80/t CFR China towards the end of last week. Fe 54% fines export price indications were at around $59-60/t CFR China.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) declined by $13/t w-o-w to $96/t on 5 June 2024. No deal was recorded from the east coast in this publishing window, as per data maintained with BigMint. The exporters received only a few bids in the downtrend market at lower prices.

- Asia-Pacific Supramax dry bulk (50,000-55,000 t) freight rates for an iron ore vessel from the east coast of India to China fell by $0.4/t this week to $13.9/t on 5 June, as per BigMint’s assessment. Dry bulk iron ore freight rates experienced a slight decrease this week on major routes, as demand remained low and trade activities are limited in global markets. Furthermore, buyers have secured vessels at reduced rates for shipments in June.

Coal

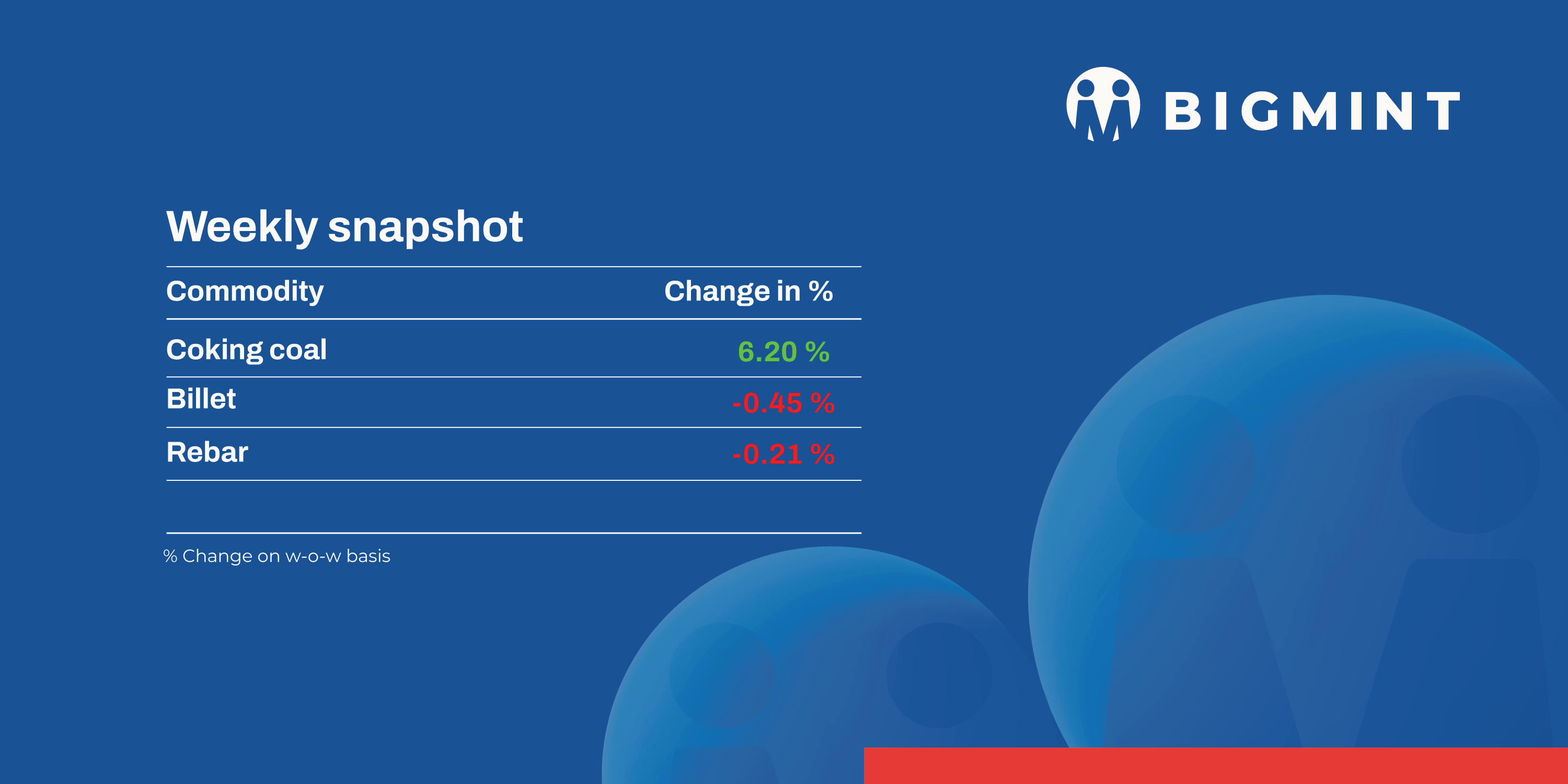

- Australian premium hard coking coal prices picked up by 6% w-o-w to $256.25/t FOB and $274.05/ t CNF on 7 June. The prices picked up on rising demand, coupled with limited availability of cargoes for July loading.

- RB1 (6000 NAR) grade prices edged up w-o-w to $110/t FOB. However, RB3 stood stable w-o-w at $79/t FOB Richards Bay, South Africa.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port were recorded at INR 8,350/t, majorly stable w-o-w.

Ferro scrap

- Indian buyers showed resistance to making firm commitments amidst rising freight costs, which were further exacerbated by container shortages, resulting in market uncertainty.

Throughout the week, the Indian imported ferrous market experienced sluggish activity as buyers adopted a wait-and-see approach due to the uncertain parliamentary election results. This cautious stance resulted in minimal trading and a noticeable bid-offer disparity. Shredded scrap offers from the US and the UK/Europe were consistently assessed at $415-420/t CFR Nhava Sheva, occasionally reaching $428-430/t CFR, while buyers aimed for lower prices of $410-415/t CFR. - HMS (80:20) offers from the UK/Europe, and West Africa ranged from $395-400/t CFR, with buyer bids slightly lower at $390-395/t.

- In the domestic scrap market, despite high production levels of 90-95% at steel mills, new bookings for imported materials were scarce. Traders feel market sentiments will stabilize in the coming days, and that there will be a short-term impact of the election results.

- As per market insiders, regional government changes in states like Odisha, Andhra Pradesh, and Uttar Pradesh could have localized effects, but overall, the market was expected to recover. An upward trend in imported scrap prices was also predicted due to increasing freight rates.

Ferro alloys

- Silico manganese: Silico manganese prices in India increased w-o-w by INR 4,850/t ($58/t) to INR 90,400-90,900/t ($1,082-1,088/t) exw across markets. The primary driver behind this price surge was the escalated raw material costs

- Ferro manganese: Ferro manganese (HC70%) prices increased w-o-w by INR 1,600/t ($19/t) in Raipur, reaching INR 95,000/t ($1,137/t) exw. Meanwhile, in Durgapur, prices rose by INR 3,000/t ($36/t) to INR 96,000/t ($1,149/t). Prices witnessed an uptick due to the risen manganese ore prices.

- Ferro silicon: Indian ferro silicon (FeSi:70%) prices decreased by INR 650/t ($8/t) settling at INR 98,000/t ($1,173/t) down by INR 1,100/t ($13/t) exw-Guwahati on 7 June. Meanwhile, Bhutan’s prices also inched down by INR 200/t ($2/t), reaching INR 98,000/t ($1,173/t) exw. The market marginally declined post-Bhutan’s offers that stood at INR 98,000/t ($1,173/t).

- Ferro chrome:Prices of Indian high-carbon ferro chrome (HC60%, Si:4%) prices remained unchanged w-o-w on 7 June, settling at INR 105,800/t ($1,267/t) exw-Jajpur. Prices remained consistent on moderate demand and most market players awaited the outcome of FACOR’s auction last week.

Semi-finished

- Indian semi-finished steel prices decreased as per BigMint’s assessment. Domestic billet prices in almost all key locations decreased by INR 50-500/t across regions, with a major decrease of INR 500/t seen in the Hyderabad market. However, billet prices only in Mandi Gobindgarh rose slightly by INR 200/t. Similarly, sponge iron prices also decreased in key locations by INR 50-700/t, with a major decrease of INR 700/t seen in the Rourkela and Raigarh markets.

- SAIL-Durgapur Steel Plant (DSP) held an auction for 2,500 t of steel-grade pig iron on 4 June. The total quantity was booked at an average price of INR 39,800/t exw.

- Tata Metaliks has decreased pig iron prices for both basic and foundry grades by INR 1,500/t ($18/t) due to the lack of demand at existing prices. Post-revision, prices of foundry-grade pig iron stand at INR 45,000/t ($541/t), while basic grade (Si 1.0-1.5%) prices are at INR 42,500/t ($511/t).

- Indian DRI export offers decreased by approximately $3/t, reaching $403/t on CPT Raxaul, and $405/t on CPT Benapole.

Finished long steel

- IF-rebar: India’s induction furnace-route finished long steel followed a mixed price trend w-o-w. Subdued buying interest prevailed since the last few weeks as minimal movement was observed in the spot market amid bid-offer disparity. This has led to rise in inventory levels at mills across regions as manufacturers have over 10-15 days inventory available now. Suppliers were offering attractive discounts to boost sales, but buyers resorted to need-based material procurement. However, they reported proper lifting of previously booked material. Currently, participants await clarity on the trend as constant fluctuation in prices are being observed at the moment.

- On a weekly basis, rebar steel prices fluctuated by INR 100-700/t across regions, as per BigMint’s assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route, of 10-25 mm size, was assessed at INR 47,800-48,200/t exw Raipur, and at INR 51,900-52,500/t exw-Jalna.

-

Trade reference prices of heavy structural steel for base size 150 mm channel stood at INR 49,700-50,200/t exw Raipur.

-

Trade reference prices of wire rods hovered at INR 47,700-48,200 /t ex Raipur.

- BF-rebar: Indian tier-1 mills have increased rebar list prices by INR 500-1,000/t for early-June 2024 deliveries, sources informed BigMint. Current list prices are hovering at INR 58,500-59,500/t on landed basis. Following this, trade prices witnessed uptick across markets while buying interest continued to remain subdued, weighing on sentiments. On a monthly basis, rebar prices in the trade segment rose by INR 3,700/t to a monthly average of INR 58,300/t exy-Mumbai in May owing to limited supplies from mills due to maintenance shutdowns.

- Current week’s BF-rebar prices (12-32mm) in the trade segment inched up by INR 100/t w-o-w to INR 58,100/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the projects segment, prices were hovering at INR 57,000-58,000/t FOR Mumbai.

Finished flat steel

- Some steel mills have announced price hikes of INR 500-1,100/t ($6-13/t) for June’ compared to May levels, while a PSU steel major and another private mill have rolled over prices.

- Following the announcement, the list prices set by mills for HRCs (2.5-8mm, IS2062 Gr- E250 BR.) and CRCs (0.9mm, IS513 CR 1) for June sales stood at INR 54,200-55,750/t ($650-668/t) and INR 59,800-62,250/t ($717-746/t), respectively, excluding GST at 18%.

- In recent assessments, HRC and CRC prices had remained range-bound prior to the price announcements by the mills amid the declaration of election results. However, HRC prices in Hyderabad rose by INR 1,300/t ($16/t) to INR 53,500-54,500/t ($641-653/t) in reflection of the expected list price hike by mills.

- The traders’ market exhibited persistent sluggishness due to weak demand. Market participants have tried to concurrently increase their offers, citing supply constraints and anticipating a hike in prices by the mills. However, buyers are resisting price hikes, negotiating for lower prices and opting for need-based purchases.

- According to vessel line-up data tracked by BigMint, India’s imports of bulk HRC and plates witnessed a decrease in May 2024 compared to the previous month. Imports reached 357,329t in May, down from 422,132t in April.

- India’s exports of bulk HRC and plates also declined during the same period. Exports stood at 252,673t in May, compared to 365,618t in April.

- Indian steel mill1s have maintained their HRC export offers to South-east Asia, the Middle East this week. However, in a recent development, a few offers of Indian-origin HRCs, CRCs, and hot-dip galvanised iron (HDGI) have been heard in the European Union (EU).