- BF-grade rebar falls w-o-w amid slow demand

- Trade-level HRC prices rise by INR 1,200/t w-o-w

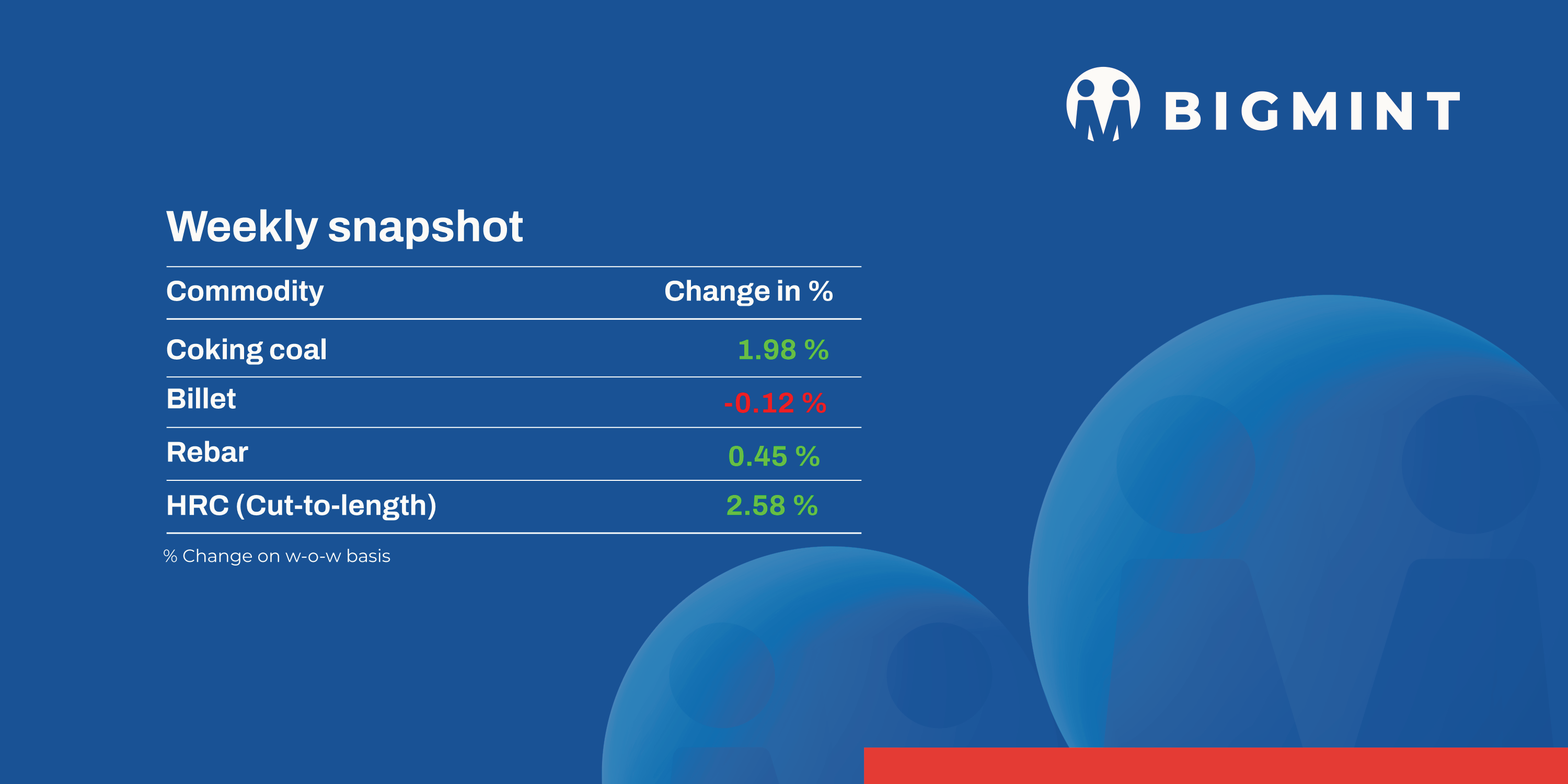

The domestic steel market witnessed a mix trend in prices during week 17 ( 21-26 April, 2025). Semi-finished steel prices rose in the range of INR 100-500/tonne (t).

Iron ore and pellets

- BigMint’s bi-weekly domestic pellet (Fe63%) index dropped by INR 200/tonne ($2/t) w-o-w to INR 9,950/t ($116/t) DAP Raipur on 25 April. Deals of around 51,500 t of pellets (Fe62.5/63%) were concluded in Raipur by local and Odisha-based suppliers. Raipur sellers dropped pellet offers by INR 200/t ($2/t) mid-week.

- NMDC Donimalai sold 8,000 t of lumps (10-40 mm, Fe 58%) and 16,000 t of fines (Fe 58%) were booked at base prices of INR 4,224/t and INR 3,537/t respectively. From NMDC Kumaraswamy, the entire 144,000 t of lumps and fines were sold, with the lots receiving an average premium of 17%.

- NMDC auctioned 108,600 t of iron ore from its Bacheli mines on 22 April. The entire 25,800 t of DRCLO (10-40 mm, Fe 67%) and 14,000 t of lumps (10-20 mm, Fe 65.5%) were sold at 13% and 7% premiums, respectively, while 68,800 t of fines (Fe 64%) received no bids. Prices were on FOR, ex-stockpile/mines basis, including royalty, DMF, and NMET.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched up by $0.5/t w-o-w to $60.5/t FOB east coast, India, on 24 April. Trade activity in the Indian Ocean remained thin, but a few exporters received inquiries. Export deals for around 175,000 t were recorded in this publishing window. Another 120,000 t of fines export deals were heard but are yet to be confirmed by the parties concerned.

Coal

- RB2 (5500 NAR) was assessed at INR 8,450/t at Gangavaram and Paradip, while RB3 (4800 NAR) remained stable at INR 7,200/t. Vizag saw RB2 trades at INR 8,150/t and RB3 at INR 7,250/t in Dhamra. Weak sponge iron demand and falling prices (down INR 450/t w-o-w) limited portside activity. No signs of pre-monsoon stocking was observed.

- Met coke prices remained largely flat w-o-w. Jajpur recorded a minor dip of INR 100/t to INR 34,100/t, while Gandhidham held steady at INR 32,200/t. A 7,500-tonne deal was reported at INR 34,000-34,500/t. Despite a $4/t uptick in Australian coking coal, domestic demand stayed muted due to a INR 600/t drop in pig iron prices.

- Imported US pet coke prices declined by $4/t, now at $106-108/t CFR for May-June deliveries. Saudi-origin pet coke was quoted at $114-120/t CFR, easing by $1/t, but faced weak buying interest. Despite Chinese demand offering some support, Indian buyers showed limited appetite due to higher costs, keeping market sentiment cautious for both origins.

Ferrous scrap

- India’s imported ferrous scrap market stayed subdued this week as prices averaged $371/t CFR, down 2% from last week’s $380/t. Weak global cues, a sharp drop in domestic steel prices, and slowing demand from Turkiye weighed on sentiment. Confusion over the new 12% safeguard duty added to the caution, though domestic steel prices briefly firmed mid-week. Buyers preferred local alternatives like sponge iron amid liquidity issues and high port inventories.

- Shredded scrap offers from the UK/Europe hovered at $370-375/t CFR Nhava Sheva, but bids lagged at $365-370/t. Most buyers stayed sidelined, avoiding high-priced cargoes. Falling Turkish scrap prices, rising freight costs, and full inventories at ports like Kandla limited fresh deals, with preference for ready or short-haul shipments.

- Around 18,000-19,000 t of imported scrap arrived in India, comprising 14,000-15,000 t of HMS 80:20 booked at $350-375/t, 1,000-1,500 t of shredded scrap priced between $370-380/t, and the remaining volume consisting of HMS 1, LMS bundles, and turning scrap.

Ferro alloys

- Silico manganese: Indian silico manganese prices decreased w-o-w by INR 700/t ($8/t) to INR 70,500-70,900/t ($826-831/t) in the key regions of Durgapur, Raipur and Vizag. The decline in domestic steel prices has significantly impacted the silico manganese market w-o-w.

- Ferro manganese: Indian ferro manganese (HC 70%) prices fell significantly by INR 1,050/t ($12/t) w-o-w to INR 73,700/t ($863/t) exw in Durgapur. Meanwhile, prices exw-Raipur, decreased by INR 800/t ($9/t) to INR 74,000/t ($867/t). Prices fell on persistent decline in inquiries and cautious market moves.

- Ferro silicon: Indian ferro silicon prices remained unchanged w-o-w at INR 95,000/t ($1,113/t) exw-Guwahati. Meanwhile, prices in Bhutan dipped by INR 200/t ($2/t) to INR 95,800/t ($1,122/t) exw. Prices dropped slightly, as sellers received limited inquiries and deals were closed at lower values.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices held steady with a slight decline of INR 100/t ($1/t) w-o-w to INR 100,500/t ($1,177/t) exw-Jajpur. The majority of market participants were in a wait-and-watch mode which acted as a buffer against price fluctuations.

- Additionally, 30,900 t of material were sold at OMC’s chrome ore auction out of the 104,600 t offered. Bids edged up by 2-5% (INR 189-900/t) against the previous auction.

Semi-finished

- Indian semi-finished steel prices showed a mixed trend as per BigMint’s assessment. Domestic billet prices in almost all key locations rose by INR 100-500/t with the major increase of INR 500/t seen in Ramgarh while other regions witnessed a decline of INR 50-500/t. However, sponge iron prices showed a downtrend in almost all key locations by INR 100-500/t, with a major decrease of INR 500/t seen in the Ramgarh market. However, the southern region’s sponge market showed an increase of INR 100-400/t.

- Indian DRI export offers increased by $1/t for CPT Raxaul, to $355/t while, CPT Benapole offers stood unchanged at $360/t.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted an auction for 12,000 t of steel-grade pig iron (for rake transport) on 22 April. Of the total offered quantity, around 4,000 t were booked at the base price of INR 33,700/t. At the previous auction, out of 10,000 t on offer, 1,000 t (for road transport) was booked at the base price of INR 34,500/t.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted an auction for 15,000 t of steel-grade pig iron (for road transport) on 23 April. Of the total offered quantity, 2,500 t were booked at the base price of INR 34,200/t. At the previous auction, out of 12,000 t on offer, 4,000 t were booked at the base price of INR 33,700/t (for rake transport).

Finished longs

- IF rebar: India’s induction furnace-route finished long steel prices displayed a mixed trend w-o-w. Early in the week, moderate trading activity was observed as manufacturers raised prices following the imposition of a 12% provisional safeguard duty on certain steel imports. However, buyer resistance to higher prices led to subdued procurement. In response, manufacturers adjusted their offers in the latter half of the week, offering attractive discounts to stimulate sales. Market participants anticipate continued volatility in the near term as well.

- On a weekly basis, rebar steel prices showed a mixed trend in the range of INR 100-600/t across regions, as per BigMint’s assessment.

- The trade reference price of Fe500 grade, 10-25 mm, rebar manufactured via the IF route was assessed at INR 44,800-45,300/t exw Raipur, and at INR 49,200-49,700/t exw Jalna.

- Trade reference price of heavy structural steel of base size 150mm stood at INR 45,900-46,200/t exw Raipur.

- Trade reference prices of wire rods hovered at INR 45,000-45,500/t ex Raipur.

- BF-rebar: Trade-level blast furnace (BF) rebar prices dropped on a weekly basis amid slow domestic demand across key Indian markets. Buyers preferred to wait and watch, anticipating further fall in prices in the near term. In addition, limited availability of material in the market is still prevailing across some regions.

- Trade-level BF rebar prices edged down by INR 200/t w-o-w to INR 56,900/t exy-Mumbai, as per BigMint’s assessment on 25 April 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered at around INR 55,500-56,500/t FOR Mumbai.

Flats

- Trade-level prices of hot-rolled coils (HRC) rose by up to INR 1,200/t w-o-w to INR 52,500-53,500/t across major markets. Cold-rolled coil (CRC) prices also increased by up to INR 1,000/t w-o-w to INR 57,000-60,2000/t.

Market sentiment remained cautious due to sluggish demand and buyer resistance to higher prices. - BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) increased by up to INR 300/t w-o-w to INR 51,600/t ($601/t) on 22 April 2025. However, CRC (IS513, Gr O, 0.9 mm/CTL) prices remained stable w-o-w at INR 58,500/t ($685t). These prices are quoted ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

India’s bulk imports of HRCs and plates touched 2,10,591 t as of 21 April, based on vessel line-up data from BigMint. Another 65,488 t are expected by the end of the month. - Indian mills have increased their HRC (S275) FOB offers to Europe. However, trade activity in the region is currently slow due to the just-concluded Easter holiday period. Indian HRC export offers to the EU have increased by $10-15/t w-o-w, reaching $645-650/t CFR Antwerp, compared to $630-635/t CFR in the previous week. Indian mills are not actively offering to the Middle East due to price competition from Chinese suppliers and more favourable domestic prices.

Leave a Reply