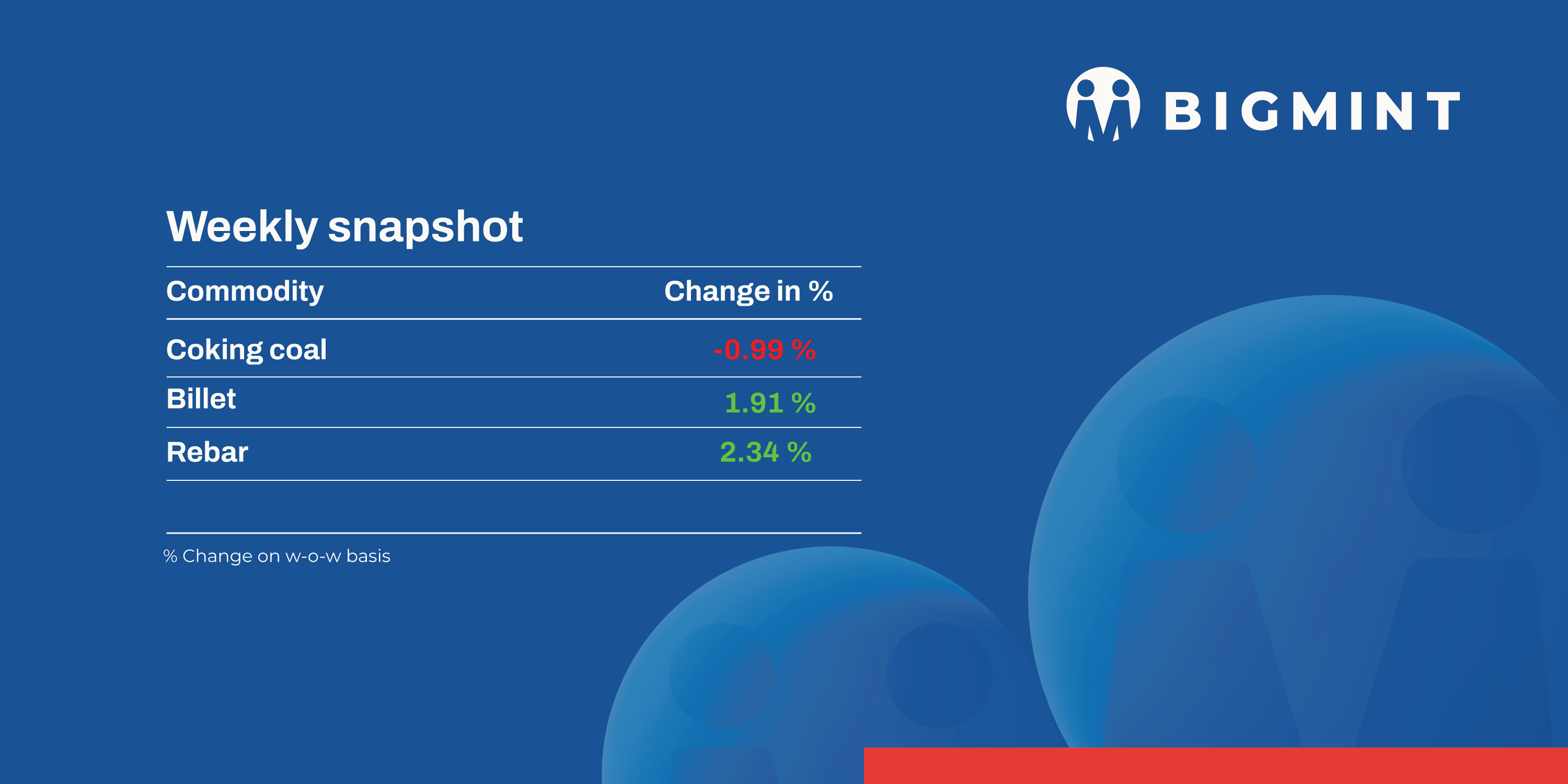

India’s semi-finished steel prices showed an uptrend w-o-w, with billet and sponge iron tags moving up across most locations. Additionally, domestic induction furnace (IF) finished long steel offers increased by INR 200-800/tonne (t) this week.

Trade reference prices for hot rolled coils (HRCs) and cold rolled coils (CRCs) increased in most regions, with a maximum rise of INR 800/t seen in the market.

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe63%) index inched up by INR 50/t ($0.5/t) w-o-w to INR 9,850/t ($113/t) DAP Raipur on 28 February. Around 36,500 t of were recorded by BigMint at INR 9,650-10,050/t ($110-115/t) DAP Raipur. However, overall buying interest remained sluggish as buyers restricted their bookings to need-based procurement, showing no urgency to stock up inventory.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) decreased by $4.5/t w-o-w to $100/tonne (t) on 28 February. A few eastern India-based exporters sold 115,000 t (Fe63%) at $114-115/t CFR China in the middle of last week, while trades remained muted this week amid lower prices. An Indian pellet-maker concluded an export deal for around 50,000 t (Fe 63%, 2% AL2O3) at $106/t FOB India this week.

- NMDC auctioned 358,300-t iron ore from Chhattisgarh on 25 February. From Bacheli mines, entire 34,400-t DRCLO (10-40 mm, Fe 67%) offered was booked at INR 7,130/t (base price and bids were similar to previous auction). The entire 10,000-t of Baila-sized lumps (10-20 mm, Fe65.5%) received 1.7% premium over the base price of INR 6,500/t while 193,500-t fines (Fe 64%) were unsold. Around, 120,400-t ROM (10-150 mm, Fe 65.5%) remained unsold from Kirandul Prices are on FOR, ex-stockpile/mines basis, including royalty.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $2.5/t w-o-w at $66.5/t FOB east coast, India, on 27 February. Odisha-based traders sold around 115,000 t of iron ore fines (Fe 57%) at $78-79/t CFR China last weekend. Market participants remained cautious this week and deals were subdued.

Coal

- Portside South African thermal coal prices in India drop to 1-year low. RB2 (5500 NAR) thermal coal prices at Gangavaram fell to INR 8,500/tonne (t), while RB3 (4800 NAR) dropped to INR 7,100/t, down by INR 50/t. Higher domestic coal availability reduced demand for imported coal, leading to weaker bids. Portside thermal coal stocks rose 3.6% w-o-w to 13.04 mnt.

- Prices of Indonesian non-coking coal at Indian ports have experienced a moderate uptick, largely influenced by global rise in prices amid currency depreciation and higher freight rates. Coal prices at Indian ports have shown mixed trends for the different grades. At Kandla, the price of 5000 GAR coal rose by INR 50/t, reaching INR 7,700/t. Similarly, high-GCV 5000 GAR coal at Vizag also saw a slight increase to INR 7,600/t.

- India’s domestic met coke prices increased, with 25-90 mm BF-grade coke at INR 34,500/tonne (t) exw-Jajpur and INR 32,000/t exw-Gandhidham, both up INR 800/t w-o-w. Limited import bookings and lower port inventories supported higher domestic offers. However, trades at these prices remain slow. Merchant coke plants are hesitant to restart production due to uncertainty over quantitative restrictions beyond June.

Ferrous scrap

- India’s imported scrap market edged up by 1% this week, with UK/Europe-origin shredded prices reaching $375/t CFR Nhava Sheva, up from $373/t the previous week. Despite weak demand, tight liquidity, and a widening bid-offer gap, sellers managed to push prices slightly higher amid rising Turkish scrap prices and improved rebar demand. However, buyers remained hesitant due to sufficient domestic scrap availability and currency depreciation.

- US-origin scrap saw little activity, with no firm offers emerging, Limited interest in 40-ft containers further slowed US trade, while bulk shipments faced delays of 60-70 days, discouraging purchases. Market sentiment remained cautious, as many buyers focused on clearing existing inventories at ports. While hopes for recovery post-March persist, demand uncertainty and global trade shifts, including US tariff changes and Turkish scrap trends, will influence buying decisions in the coming weeks.

- Approximately 11,000-12,000 t of scrap were booked, including 7,000-8,000 t of HMS (80:20) from the UK, Poland, Venezuela, Europe, and Australia at $340-365/t. Additionally, 1,000-1,500 t of shredded scrap from the UK traded at $375/t, while 1,500-2,000 t of PNS scrap from Poland and the EU was secured at $370-375/t. The remaining volumes consisted of turning scrap, busheling, and other scrap types.

Ferro alloys

- Silico manganese: Indian silico manganese prices were slightly down w-o-w by INR 250/t ($3/t) w-o-w to INR 72,500-73,600/t ($829-841/t) in key regions of Durgapur, Raipur and Vizag. The slight correction in prices can be seen because of the resumption in productions and market discounts.

- However, MOIL has raised its manganese ore offers for Mar’25 by 10% for Mn>44% and by 6.5% for Mn<44%.

- Ferro manganese: Indian ferro manganese (HC 70%) prices remained firm w-o-w and stood at INR 76,000/t ($869/t) exw in Durgapur. Meanwhie, prices exw-Raipur also remained unchaged at INR 76,000/t ($869/t). The price stability resulted from consistent market operations and subdued export demand, maintaining balance in the market without significant fluctuations or disruptions.

- Ferro silicon: Indian ferro silicon prices diminished by INR 400/t ($5/t) w-o-w to INR 100,500/t ($1,149/t) exw-Guwahati. Prices also decreased by INR 600/t ($7/t) in Bhutan to INR 100,500/t ($1,149/t) exw. Prices fell, as buyers mostly preferred imported material, whose volumes surged, which led to lower inquiries in the domestic market.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices remained unchanged w-o-w to INR 100,700/t ($1,151/t) exw-Jajpur. Prices remained steady following two key domestic auctions – for chrome ore from the Odisha Mining Corporation (OMC) and ferro chrome from Vedanta-FACOR.

- At OMC’s chrome ore auction on 19 February, 37,100 t were booked out of the 84,500 t offered. Bids went up for some grades by 6-27% (INR 943-5,378/t), while for some, they decreased by 12-18% (INR 2,814-4,890/t) in comparison to the previous month’s auction. Premiums also went up by 5-42% (INR 800-8,900/t) over the base price.

- Vedanta-FACOR’s ferro chrome auction was held on 24 February. The larger lot of 10-150 mm received an H1 price of INR 99,750/t ($1,143/t) exw, up by INR 550/t ($6/t) against the previous auction on 6 January.

Semi-Finished

- Indian semi-finished steel prices showed uptrend as per BigMint’s assessment. Domestic billet prices in almost all key locations increased by INR 200-800/t across regions, with a major increase of INR 800/t seen in the Chennai market. While only, Rourkela and Bhavnagar slipped down by INR 250-400/t ex. However, sponge iron prices also moved up, almost all key locations increased by INR 300-700/t, with a major increase of INR 700/t seen in the Hyderabad market.

- Indian DRI (Direct Reduced Iron) export offers increased by $10 for CPT Raxaul, stood at $350/t while, CPT Benapole offers increased by $3 stood at $345/t.

Finished Long Steel

- IF-rebar:India’s induction furnace route finished long steel prices rose week-on-week, driven by moderate trading activity. Strong buying interest in the early part of the week prompted manufacturers to raise prices slightly. However, demand slowed in the latter half as buyers hesitated to purchase at higher rates, opting to wait for clearer market trends. With steady material movement, mill inventories remain stable at an average of 8-10 days. Market participants expect prices to stay range-bound in the near term.

- On a weekly basis, in rebar steel prices seen surged in the range of INR 300-1,300/t across the regions as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 43,500-43,900/t exw Raipur, INR 47,800-48,400/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 45,000-45,500/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 44,000-44,500/t ex Raipur.

- BF-rebar:Trade-level BF-rebar prices have witnessed rise on weekly basis amid the ongoing material shortages across major Indian markets. Logistics disruptions have led impacted the supplies, as a result this has created shortage of material at distributors channel.

- Current week’s rebar prices (12-32mm) in the trade segment rose w-o-w by INR 600/t to INR 53,200/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the project segment, prices ranged between INR 51,000-52,000/t FOR Mumbai.

Flat Steel

-

- Hot-rolled coil (HRC) prices in India rose by up to INR 800 per tonne week-over-week, reaching INR 48,000-50,000 per tonne. Cold-rolled coil (CRC) prices also increased by up to INR 600 per tonne, now ranging between INR 53,500-56,000 per tonne ($617-671 per tonne) across markets.

- The price increase was driven by supply shortages, even though demand remained limited.

- Imports of bulk HRCs and plates stood at 3,83,294 t till 24 February, as per vessel line-up data maintained with BigMint. It is expected that an additional 38,195 t will be imported by the month-end and 82,349 t in the first week of March.

- The BigMint India HRC (SAE 1006) export index to the Middle East and Vietnam remained stable at $505/t FOB, reflecting reduced trade activity ahead of Ramadan. Despite Vietnam’s anti-dumping duties on Chinese HRCs, and which exclude Indian imports, mills from the latter are not actively exporting to Vietnam. HRC exports to the EU are also limited, pending the outcome of the anti-dumping investigation and new import quota announcements.

Leave a Reply