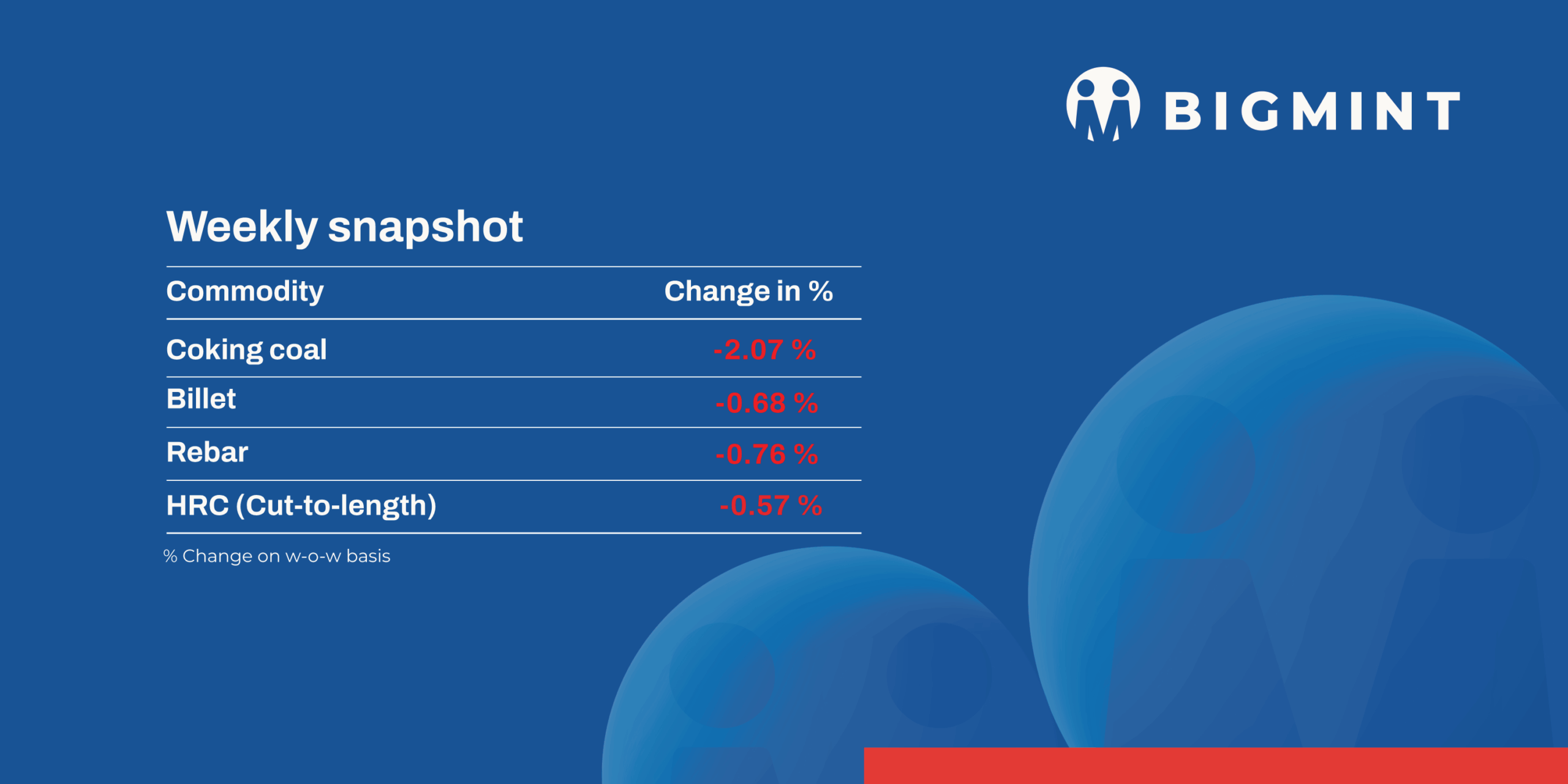

Semi-finished steel prices saw movements of INR 100-500/t during 14-19 July, with traders and buyers closely watching today’s OMC iron ore auction for potential market direction and price stability.

Iron ore and pellet

- OMC has scheduled an auction for 2.249 mnt of iron ore (0.901 mnt of lumps and 1.348 mnt of fines) on 19 July 2025. The miner has increased base prices by INR 150/t m-o-m for the few of fines and lumps lots. Heavy rainfall has curbed iron ore availability, restricting production and dispatch, which led to an increase in base prices.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, rose by INR 400/t ($4.5/t) w-o-w to INR 9,700/t ($108/t) DAP Raipur on 18 July. Raipur-based pellet producers raised their offers for 63% (+/-0.5%) material by INR 200/t ($2.5/t) to INR 9,500-9,700/t ($110-112/t) exw.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched up by $1.5/t w-o-w to $64.5/t FOB east coast on 17 July. Indian export prices have reached their highest level in four-and-a-half months, with the last similar price level observed at the end of February 2025. Around 225,000 t Fe57% fines were sold at $75-76/t CFR China this week in the uptick prices in the sea market.

Coal

- Portside prices for South African coal inched up amid disruptions in rail movement and RBCT maintenance, with RB2 at INR 7,650/t and RB3 at INR 6,650/t exw-Gangavaram. Offers stayed volatile, but weak buying interest capped gains. Portside stocks held steady at 15.84 mnt as arrivals matched offtake. Going ahead, South African supply tightness may lend some support, but high domestic availability and muted industrial demand may limit any sharp rise. Traders remain cautious, waiting for firmer cues from end-user sectors.

- Domestic coal prices stayed flat this week, with 5000 GCV and 4500 GCV assessed at INR 4,700/t and INR 4,250/t exw-Bilaspur. Market activity remained slow as buyers refrained from new bookings. However, in SECL’s latest auction, a few high-grade lots received decent bids, while most grades hovered near notified prices. Supply stayed steady, and end-user demand remained subdued.

- BigMint’s premium hard coking coal (PHCC) index dropped to $186/t CNF Paradip on 18 Jul’25, down by $8/t w-o-w. Indian steelmakers have mostly secured cargoes for Aug loadings, with fewer spot trades seen. A few Australian-origin deals were concluded at $183–188/t CFR. Canadian offers stood at $175–180/t, but no trades were heard.

- Met coke prices in India picked up slightly this week due to stable steel demand and tight global supply. As of 16 July, BF-grade met coke was assessed at INR 29,000/t ex-Jajpur, up by INR 500/t. Prices in Gandhidham rose modestly to INR 29,100/t. India’s met coke imports dropped 9% y-o-y to 2 mnt in H1CY’25, owing to government QRs and good domestic supply. Meanwhile, China may raise coke prices amid supply cuts, even as Australian PHCC dropped $5/t w-o-w to $173/t FOB.

Ferrous Scrap

- India’s imported scrap market stayed weak this week amid poor steel demand, monsoon disruptions, and buyer caution. HMS 80:20 offers hovered at $325-330/t CFR, Market activity was muted as mills avoided new bookings, citing poor finished steel demand and unclear tradable levels.

- Mills shifted to sponge iron which saw 50-60% higher intake and domestic scrap due to cost advantages, reducing reliance on imports. Sellers held shredded offers near $365-370/t CFR, but buyers stayed firm at lower levels. Only limited deals were heard, with UK/Europe shredded assessed at $360/t CFR Nhava Sheva, down 1% w-o-w.

- Around 5,000-6,000 t of imported scrap was booked into India this week, mostly HMS 80:20 at $330-345/t CFR. The rest included MS Turning, HMS-LMS bundle mix, and HMS 1.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) edged down by INR 350/t ($4/t) w-o-w to INR 72,400-73,000/t ($840-847/t) in the key regions of Durgapur, Raipur, and Vizag. The price decline was mainly driven by weakening demand and a drop in steel prices, both of which have significantly influenced the overall pricing dynamics.

- Ferro manganese: Indian ferro manganese (HC 70%) prices went down w-o-w by INR 750/t ($9/t) at INR 71,150/t ($826/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also dropped by INR 1,100/t ($13/t) at INR 71,100/t ($825/t). Need-based purchasing and subdued demand continued to weigh down Indian ferro manganese prices.

- Ferro silicon: Indian ferro silicon prices declined by INR 1,100/t ($13/t) w-o-w to INR 85,700/t ($994/t) exw-Guwahati. Meanwhile, Bhutanese prices decreased by INR 700/t ($8/t) to INR 86,300/t ($1,001/t) exw. The market remained sluggish, with limited activity as sellers reduced their offers and buyers showed resistance toward higher prices.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices were stable w-o-w at INR 99,600/t ($1,156/t) exw-Jajpur. Prices remained stable amid a quiet market, with attention focused on today’s OMC chrome auction.

- Odisha Mining Corporation (OMC) has scheduled an auction for 73,100 t of chrome ore today, with the offered quantity reduced by 2,900 t m-o-m. Meanwhile, base prices of all grades were reduced marginally by 1% (INR 10-297/t).

Semi-finished steel

- Indian semi-finished steel prices showed an increasing trend, as per BigMint’s assessment. Domestic billet prices in all key locations went down by INR 250-500/t. Meanwhile, other regions showed a slight increase of up to INR 100-300/t. Sponge iron prices showed mixed trends.

- Indian DRI (Direct Reduced Iron) export offers increased by $5 stood at CPT Raxaul, at $325/t while, CPT Benapole offers seen decreased by INR 3/t and stands at $332/t.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 10,000 t of steel-grade pig iron on 17 July, with the entire quantity getting booked at an average price of INR 31,450/t (by road). However, management approval is still pending. Bids increased by INR 350/t from the previous auction on 1 Jul’25 for 10,000 t where the entire quantity were booked at an average of INR 31,100/t (by road).

Finished long Steel

- IF-rebar: India’s induction furnace rebar prices remained under pressure this week, despite a slight pickup in trading activity. Buyers still booked moderate quantities anticipating that prices may decline further . However, manufacturers further reduced prices to encourage sales. Currently, inventory levels are reported at around 12-15 days. Market participants expect the market to remain subdued in the near term, primarily due to weak project demand and sluggish construction activity amid the ongoing monsoon season.

- On a weekly basis, in rebar steel prices witnessed mixed response in the range of INR 100-500/t across the regions as except in Patna market where prices hiked by INR 500/t as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 38,800-39,200/t exw Raipur, INR 42,700-43,300/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 41,500-42,000/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 40,600-41,000/t ex Raipur.

- BF-rebar: India’s trade-level blast furnace (BF) rebar prices declined w-o-w, driven by weak demand, cautious market sentiment, and a monsoon-led slowdown in trade momentum. Buyers adopted a wait-and-watch approach due to the prevailing disparity between bids and offers, while distributors aimed to offload previously procured high-cost inventories.

- Trade-level BF rebar prices declined by INR 800/tonne (t) ($9/t) w-o-w to INR 48,400/t ($562/t) exy-Mumbai, as per BigMint’s assessment on 18 July 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices declined further to INR 46,000-47,000/t ($534-546/t) FOR Mumbai. Limited orders were placed amid expectations of further price corrections. Mills continued to face challenges in securing bookings due to stiff market competition.

Flat steel

- Trade-level prices of hot-rolled coils (HRCs) in India declined by up to INR 500/tonne (t) w-o-w to INR 49,200-51,400/t ($574-599/t) across markets. Moreover, cold-rolled coil (CRC) prices dropped by INR 800/t w-o-w to INR 55,000-59,500/t ($641-694/t).

- BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 700/t ($8/t) w-o-w to INR 49,200/t ($574/t) on 15 July 2025 against INR 49,900/t ($582/t) a week ago. Additionally, CRC (IS513, Gr O, 0.9 mm/CTL) prices declined by INR 500/t ($6/t) w-o-w to INR 56,000/t ($653/t) on Tuesday against INR 56,500/t ($659/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

- Market sentiment remains subdued as demand continues to be lacklustre, with no visible signs of recovery. Inventory levels at the distributor end also remain elevated, reflecting slow offtake. In response, buyers are largely adopting a “wait and watch” stance, anticipating a potential further correction in prices before making fresh purchases.

- India’s bulk imports of HRCs touched 201,211 t as of 12 July, based on vessel line-up data. Around 282,745 t of additional cargo are expected by the month-end.

- India’s bulk exports of HRCs touched 43,357 t as of 12 July, based on vessel line-up data from BigMint. Indian HRC export offers to the EU fell amid subdued European demand and concerns around CBAM costs. Moreover, Indian mills held back offers due to strong domestic demand and overseas competition

Leave a Reply