- Pellets, coke, ferro chrome prices rise, scrap imports stay low

- BF-rebar and HRC gain on tight supply, cautious demand prevails

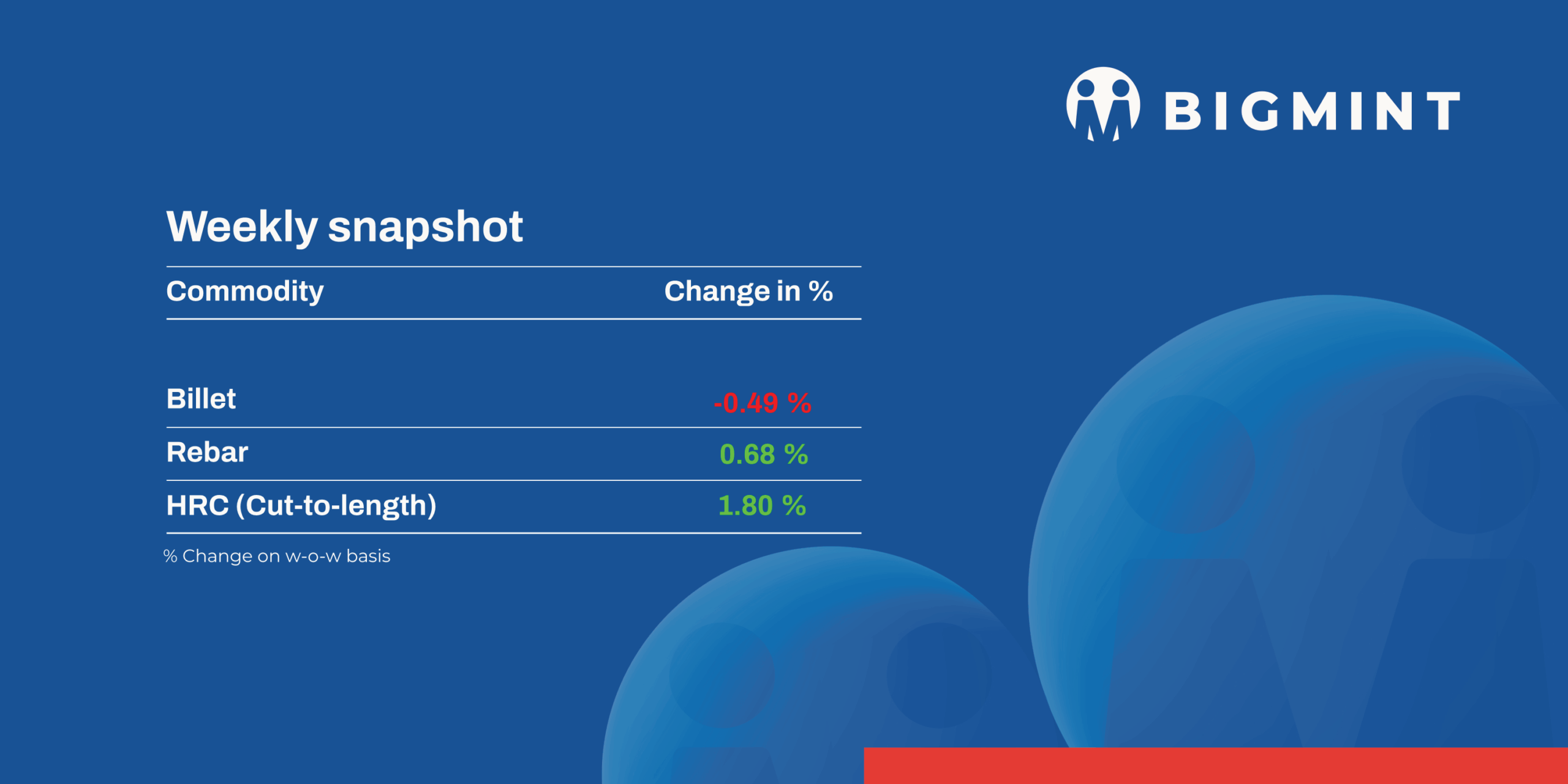

The domestic steel market witnessed mixed price movement during week 5 (26-30 January, 2026). Semi-finished steel prices fluctuated in the range of INR 200-700/tonne (t).

Iron ore and pellet

- BigMint’s bi-weekly assessment showed Indian low-grade iron ore fines (Fe 57%) export prices edging up by $2/t w-o-w to $66/t FOB east coast on Thursday. The index stood at $76/t CFR China, with discount levels against the global Fe 61% benchmark narrowing marginally. Despite a broadly cautious seaborne market sentiment, intermittent buying interest helped lend stability to prices.

- In Raipur, pellet producers increased offers for Fe 62.5–63% (+/-0.5) grade pellets by INR 200/t ($2/t) to INR 9,800–9,900/t ($107–108/t) ex-works on 29 January. The hike was driven by rising iron ore fines prices and recent upward revisions in pellet offers from Odisha. Additionally, sponge iron prices climbed INR 900/t w-o-w, further supporting pellet price momentum.

- Meanwhile, domestic iron ore prices in Karnataka’s Bellary region remained range-bound, with low-grade fines holding steady at INR 2,700/t ($29/t). While recent gains in downstream steel and sponge iron prices provided some support to raw material prices, overall market sentiment remained cautious, with no significant improvement observed so far.

Coal

- Portside South African thermal coal prices had increased in week 5 amid tightening stocks and selective deals. As per BigMint assessment, exw-Paradip 5,500 NAR rose by INR 100/t w-o-w to INR 9,500/t, while 4,800 NAR remained at INR 8,100/t. At Vizag, 5,500 NAR gained INR 150/t to INR 9,400/t and 4,800 NAR increased INR 50/t to INR 8,000/t.

- Domestic non-coking coal prices had remained unchanged w-o-w, with 5,000 GCV assessed at INR 5,750/t and 4,500 GCV at INR 4,800/t. Market sentiment had stayed stable, supported by steady supply through SECL auctions. On 27 January 2026, SECL had offered 1,716,050 t and allocated 915,200 t. Most bulk mid-CV grades had cleared close to floor prices.

- Indian BF and foundry grade metallurgical coke prices had risen sharply w-o-w on 28 January, driven by higher coking coal costs and tight foundry-grade supply. In east India, BF-grade (25–90 mm) increased by INR 500/t to INR 34,000/t ex-Jajpur, while in west India prices rose INR 200/t to INR 30,300/t ex-Gandhidham. Foundry-grade (+90 mm) jumped INR 900/t to INR 36,100/t ex-Rajkot amid limited availability. Australian PHCC climbed $14/t to $251/t FOB due to weather-led supply disruptions, while China remained stable.

Ferrous scrap

- The imported scrap market stayed weak as the rupee depreciated and steel sales remained poor, while the INR-USD conversion touched its highest level, further tightening import affordability. Mundra remained firmer than Chennai, with HMS 80:20 mostly around 350 CFR Mundra versus 330-335 CFR Chennai for UK/EU, keeping mills focused on domestic scrap.

- Shredded and higher grades struggled as buyers resisted firm offers. Canada/US shredded at $366-368 CFR Nhava Sheva and EU HMS 80:20 at $340-345 drew lower bids. Australia-origin offers into Chennai at $330-334 for HMS 80:20 and near $350 for shredded also faced pushback amid a softer southern market.

- In the last seven days, India imported around 3,000-4,000 t of ferrous scrap, of which roughly 1,500-2,000 t was HMS 80:20 priced between 325-353 CFR, while the rest consisted of turning boring, re-rollable scrap, and other mixed machining grades.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices inched up by INR 350/t ($4/t) w-o-w to INR 72,200–73,100/t ($787–797/t) across Durgapur, Raipur, Vizag, and Raigarh, reaching over six-months high. Similar price levels were last seen in July 2025.

Prices strengthened on the back of strong smelter bookings at higher levels, supported by firm spot transactions. Meanwhile, rising raw material costs continued to pressure margins, keeping prices elevated in the domestic market. - Ferro manganese: Indian ferro manganese (70%) prices edged down by INR 200/t ($2/t) to INR 72,300/t ($789/t) in Durgapur, while rising slightly by INR 100/t ($1/t) to INR 72,600/t ($791/t) in Raipur. Prices remained largely stable, as subdued trading activity, cautious buying, and the lack of major spot deals kept market sentiment steady.

- Ferro silicon: Indian ferro silicon (Si 70%) prices remained largely stable, with a slight drop of INR 200/t ($2/t) to INR 93,600/t ($1,020/t) exw-Guwahati. Bhutan prices stayed unchanged at INR 93,700/t ($1,022/t) exw. Trading activity was muted due to the month-end, as most sellers were out of stock and market participants awaiting February prices from Bhutan.

- Ferro chrome: Indian high-carbon ferro chrome (60%, Si: 4%) prices rose by INR 7,400/t ($81/t) w-o-w to INR 120,000/t ($1,308/t) exw-Jajpur. The increase was driven by stronger bids at recent OMC and Vedanta-FACOR auctions, pushing prices to a three-month high last seen in late October 2025.

- Vedanta-FACOR’s 28 January auction saw the larger lot (Cr: 56%, 10–150 mm) booked at INR 121,500/t ($1,325/t), up INR 7,500/t ($82/t) from base price, while OMC’s 27 Jan’26 1,500 t lot (Cr: 60–64%, Si: 4%, 10–100 mm) sold at INR 115,800/t ($1,264/t), up INR 11,300/t ($123/t) from base price.

Semi Finished

- India’s semi-finished steel market presented a mixed picture during the week, with regional price divergence reflecting uneven demand conditions and varied cost dynamics. As per BigMint’s assessment, domestic billet prices in the eastern, central, and western regions declined by INR 200-700/t ($2-7/t) w-o-w, pressured by subdued finished steel offtake and persistent caution from buyers. In contrast, south India recorded price gains of INR 300-700/t ($3-7/t), supported by firm local offers and relatively better supply dynamics. Market participants indicated that transactions remained largely need-based throughout the week, as limited downstream demand capped procurement appetite.

- The sponge iron market also reflected mixed sentiment. Prices in Raipur, Raigarh, and Jharsuguda increased by INR 550-650/t ($6-7/t) w-o-w, supported by improved buying activity following the holiday period and competitive pricing versus alternative metallic inputs such as scrap and pig iron. However, the Durgapur region bucked the broader trend, with sponge iron prices declining by INR 100-200/t ($1-2/t) w-o-w, weighed down by weak regional demand and ample availability.

- SAIL’s Rourkela Steel Plant (RSP) conducted an auction on 28 January, successfully selling 1,000t of steel-grade pig iron at an average price of INR 37,150/t ex-works. This represented a decline of INR 950/t compared with the previous auction on 5 January, when 3,500t was sold at INR 38,100/t, reflecting softer pricing amid moderate domestic demand.

- SAIL-BSP held an auction for 4,940 t of steel-grade pig iron on 23 January, of which the entire quantity was booked at an average price of INR 36,850/t exw. Bids increased by INR 2,950/t from the previous auction, conducted on 27 December for 910 t of steel-grade pig iron in which the entire volume was booked at an average price of INR 33,900/t exw.

- NMDC Nagarnar’s pig iron auction held on 29 January, prices eased marginally amid cautious buyer sentiment and selective purchasing activity, though booking volumes improved. Out of the 10,000 t of steel-grade pig iron offered, 2,000 t were booked at an average of INR 36,500/t ex-works, down INR 100/t from the 24 January auction, which saw 900 t sold at INR 36,600/t ex-works.

- On the export front, Indian DRI offers fell slightly by $2-6/t w-o-w, with prices assessed at $330/t CPT Raxaul for Nepal and $338/t CPT Benapole for Bangladesh. Despite the downward price adjustment, enquiries and demand from both destinations remained muted.

Finished Long Steel

- IF-rebar: IF-route rebar prices exhibited a largely mixed trend w-o-w across regions. Buying activity remained moderate to need-based, indicating continued market participation. Mills were trying to hold prices at higher levels, though in some regions manufacturers lowered their prices to liquidate material and boost sales, while traders managed sales at lower price levels in line with their profit margins. In some regions, price stability and upside were supported by firm raw material costs, particularly sponge iron and billets. Overall, market participants indicated no major downward revision, lending support to near-term price stability. Furthermore, expectations surrounding the upcoming Union Budget on 1 February may keep sentiment supported.

- On a weekly basis, rebar prices varied in the range of INR 100-1,000/t w-o-w across regions except Raigarh, Mandi and Bangalore where prices remained stable, as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 44,000-44,400/t exw Raipur, INR 48,500-49,500/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 46,200-46,600/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 44,500-45,000/t ex-Raipur.

- Bf-rebar: Indian Tier-I mills increased rebar prices by up to INR 1,000/t ($11/t) this week, sources informed BigMint. Post-revision, list prices stood at INR 55,500-57,000/t ($604-620/t) on landed basis. After the hike by mills, trade-level blast furnace (BF) rebar prices (distributor to dealer) increased w-o-w across major Indian markets. Seamless material lifting and lower availability of material has kept sentiments firm this week, market participants informed.

- Trade-level BF-rebar (distributor to dealer) prices rose by INR 2,100/t ($23/t) w-o-w to INR 57,400/t ($624/t) exy-Mumbai as per BigMint’s assessment on 30 January. Prices are excluding GST at 18%.

In the projects segment, prices hovered at around INR 56,000-57,500/t ($610-626/t) FOR Mumbai. Robust demand from the infrastructure and construction segments led to a material shortage at mills, supporting prices. Some offers were heard even higher than these levels due to supply shortages.

Flat Steel

-

- Trade-level prices of hot-rolled coils (HRC) in India showed an uptick w-o-w on 27 January amid positive market sentiments, with HRC prices assessed in the range of INR 50,600-53,200/t ($552-580/t). Reflecting this trend, cold-rolled coil (CRC) prices also edged up w-o-w, with prices assessed at INR 55,200-60,000/t ($602-655/t).

- Indian trade-level HRC prices saw a modest uptick this week, driven by positive market sentiment. Additionally, tight supply conditions further supported the upward trend following mill-announced price hikes, although demand remained moderate.

- India’s bulk imports of HRCs touched 196,113 t as of 23 January, based on vessel line-up data. Around 1,14,789 t of additional cargoes are expected by early-February.India’s bulk exports of HRCs touched 51,753 t as of 23 January and around 62,425 t of additional cargo are being shipped.Meanwhile, indicative offers were heard for Europe (EU), but no firm offers and trade activities were concluded. “There has been no business activity with Europe over the last few weeks,” a domestic mill official informed.

Leave a Reply