Domestic induction furnace finished long steel offers followed mixed trends. Prices varied in the range of INR 50-500/t.

Iron ore and pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, increased by INR 150/tonne (t) w-o-w to INR 10,300/t ($117/t) DAP on 12 September. Raipur-based pellet producers raised their offers for Fe 63/63.5% (+/-0.5%) material by INR 200/t ($2/t) to INR 10,200-10,500/t ($116-119/t) exw this week. Around 80,000 t pellet deals were concluded in Raipur this week.

- NMDC Chhattisgarh conducted an auction for 66,200 t of iron ore from its Bacheli mines on 11 September. The entire 17,200-t DR CLO (Fe 67%) were booked at 6% premium (base prices INR 6,910/t); 6,000-t-sized lumps (10-20 mm, Fe 65.5%) were booked at 8.4% premium (base prices INR 6,300/t); and 43,000-t fines (Fe 64%) remained unsold against INR 5,290/t (base price). Prices were FOR basis, inclusive of royalty, DMF, and NMEDT.

- NMDC auctioned 152,000 t of iron ore from its Kumaraswamy mines in Karnataka on 10 September, in which the entire quantity was sold. 40,000-t lumps (10-40 mm, Fe 60.42%) were booked at INR 4,850/t, fetching an INR 240/t premium against a base price of INR 4,610/t, and 112,000-t fines (Fe 58.26-61.05%) were sold at base prices of INR 3,378-4,038/t. Prices are inclusive of royalty, DMF, and NMET.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index rose by $2/t w-o-w to $67.5/t FOB east coast on 11 September. Iron ore fines export prices reached their highest level in over six months since the last peak seen at the end of February. BigMint recorded nearly 525,000 t of export deals concluded by Indian exporters during the recent price rally.

Coal

- South African portside coal prices are under heavy pressure this week as traders push to clear stocks before the 22 September GST change. At Vizag, RB2 slipped INR 650/t to INR 7,750/t and RB3 fell INR 500/t to INR 6,800/t, while Gangavaram RB2 dropped INR 400/t to INR 7,900/t. Port inventories eased 7.1% w-o-w to 12.1 mnt. Market sentiment remains cautious until the GST transition passes.

- Domestic coal offers held flat this week, with buyers waiting for clarity on GST changes due 22 Sept. BigMint assessed 5,000 GCV at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. Recent SECL auctions echoed the subdued sentiment, with bids largely unchanged and the bulk of volumes allocated to power-grade coal.

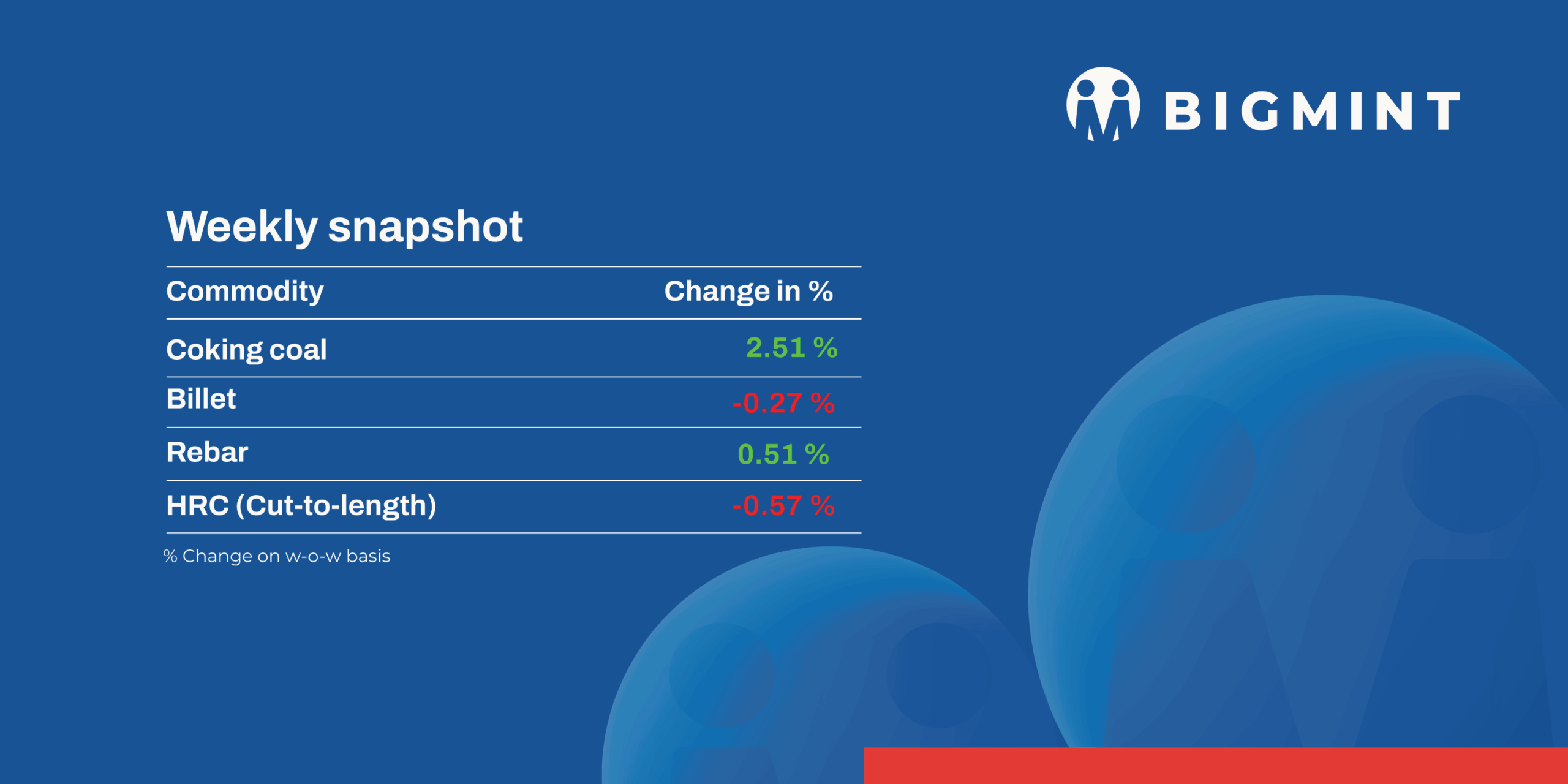

- India’s met coke market held steady in the week ending 11 Sept’25. BF-grade met coke was assessed at INR 29,500/t ex-Jajpur, while Gandhidham offers stayed at INR 30,000/t. Foundry-grade remained unchanged at INR 35,600/t ex-Rajkot. Trading stayed cautious as buyers awaited clearer demand signals despite seaborne coking coal inching up $2/t to $187/t FOB Australia.

Ferrous Scrap

- India’s imported scrap market stayed subdued, with UK/EU-origin shredded prices steady at $363/t CFR, nearly unchanged from $364/t last week. Weak steel demand, monsoon disruptions, and rupee volatility limited buying appetite, though Chennai’s domestic sentiment showed slight improvement.

- Containerised shredded bids stood at $350-355/t CFR Nhava Sheva against firm offers of $365-370/t. Small trades in African HMS at $340/t and Australian shredded at $364-366/t failed to lift sentiment.

- During the week, an estimated 3,700-4,500 t of imported scrap was booked, including 1,000-1,500 t of HMS 80:20 at $340-350/t, alongside 1,500-2,000 t of NTP bales and HMS-LMS bundle scrap.

Ferro alloys

- Silico manganese: Indian silico manganese prices (60-14) dipped by INR 100/t ($1/t) w-o-w to INR 69,100-69,500/t ($783-787/t) in the key regions of Durgapur, Raipur, and Vizag. Domestic silico manganese prices declined due to weak steel sector demand and monsoon disruptions affecting transport and material movement nationwide.

- Ferro manganese: Indian ferro manganese (HC 70%) prices remained flat w-o-w at INR 70,300/t ($796/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, edged down by INR 200/t($2/t) to INR 70,400/t ($798/t) w-o-w.Stable demand in Durgapur and slight oversupply in Raipur likely caused the minor price dip in Raipur this week.

- Ferro silicon: Indian ferro silicon prices increased by INR 2,900/tonne (t) ($34/t) w-o-w to INR 88,900/t ($1,007/t) exw-Guwahati, while Bhutanese offers also went up by INR 1,500/t ($17/t) to INR 87,500 ($991/t). Rising prices driven by robust domestic and export demand, limited producer activity, tight supply, and Bhutanese sellers diverting material abroad.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices rose by INR 4,400/t ($50/t) w-o-w to INR 118,100/t ($1,338/t) exw-Jajpur. Prices rose following trades concluded at higher offers, which sellers had raised earlier. Tight supply, stemming from some suppliers staying away from the market, has led to the sharp uptrend in recent weeks.

Semi Finished

- Indian semi-finished steel prices showed positive trends, as per BigMint’s assessment. Domestic billet prices in all key locations showed an uptrend in the range of INR 50-500/t ($1-$6) as improved buying interest and moderate bookings, bolstered by slightly positive cues from neighbouring markets, supported billet across regions except in Raipur, Jalna and Mumbai where prices fell by INR 100-300/t ($1-$3). Sponge iron prices also witnessed an uptrend, moving up by INR 50-400/t ($1-$4) across regions. Driven by regional demand recovery and rising trade volumes, sponge iron prices are expected to maintain a mildly bullish yet region-specific trend in the near term.

- Indian DRI (Direct Reduced Iron) export offers increased marginally by $1 stood at CPT Raxaul, at $330/t while, CPT Benapole offers decreased by $1/t to $338/t.

Finished Long Steel

- IF-rebar: India’s induction furnace (IF) route rebar recorded a w-o-w price rise, as manufacturers have been quoting higher offers in recent weeks. However, bookings remained moderate, with buyers largely limiting purchases to immediate requirements while opting to wait and watch for further clarity. Current mill inventories are estimated at 12–14 days, while dispatches of previously booked material are moving smoothly. Market participants anticipate near-term volatility to persist.

On a weekly basis, rebar prices surged in the range of INR 100-800/t across regions except in Mumbai where prices decreased by INR 400/t.

The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 39,500-39,900/t exw Raipur, INR 43,700-44,300/t exw Jalna.

Trade reference price of heavy structural steel for base size 150mm channel stands at INR 41,800-42,200/t exw Raipur.

Trade reference prices of wire rod hovering at INR 40,200-40,700/t ex Raipur. - BF-India’s trade-level blast furnace (BF) rebar prices dropped w-o-w across major markets. Major mills either increased their discounts or reduced list prices due to subdued market sentiments.

- Trade-level BF rebar prices edged down by INR 100/t w-o-w to INR 47,200/t exy-Mumbai, as per BigMint’s assessment on 12 September. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered between INR 45,500-47,000/t FOR Mumbai.

Finished Flat Steel

- Trade-level prices of hot-rolled coils (HRCs) in India remained range-bound w-o-w at INR 49,500/tonne (t) ($562/t), as of 5 September. Cold-rolled coil (CRC) prices saw a marginal dip of INR 100/t ($1/t) w-o-w to INR 56,700/t ($643/t) from INR 56,800/t ($645/t).

On an m-o-m basis, HRC prices rose by INR 500/t ($6/t) to INR 49,900/t ($566/t) in August 2025, up from INR 49,400/t ($560/t) in July. CRC prices also saw an uptick of INR 600/t ($7/t), reaching INR 56,900/t ($646/t) in August against INR 56,300/t ($639/t) the previous month. - India’s bulk imports of HRCs totalled 394,083 t in August, down 37% y-o-y from 624,179 t in August 2024, as per BigMint data. Imports also declined 19% m-o-m from 484,879 t in July.

- South Korea, China, and Japan were the top bulk HRC exporters to India during the month, shipping 134,503 t, 102,957 t, and 78,864 t, respectively. Imports from South Korea declined 26% y-o-y, while volumes from China and Japan fell by 28% each.

Leave a Reply