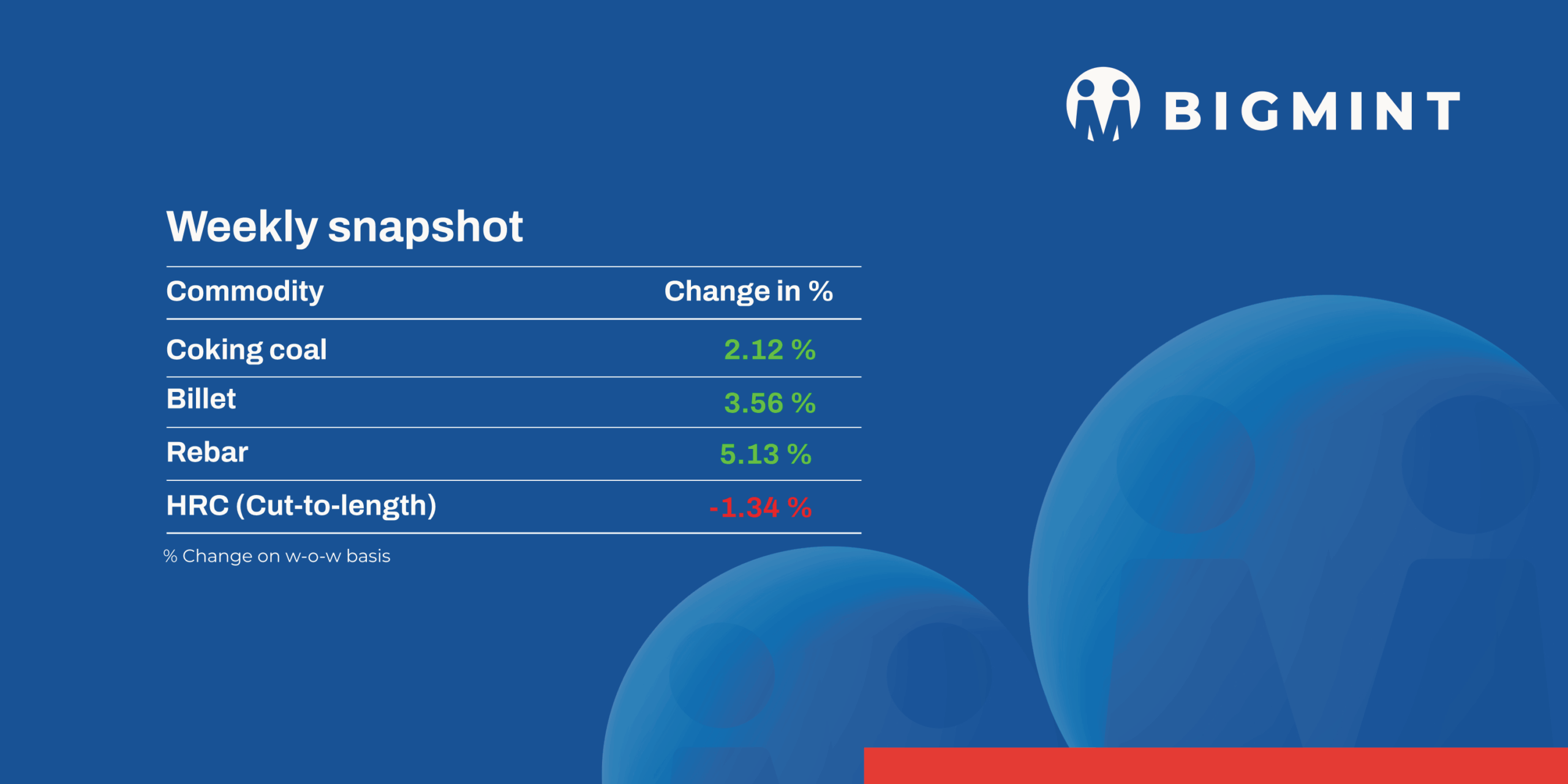

The domestic steel market saw a positive trend in prices during week 30 ( 21 July- 26 July, 2025), as semi-finished steel prices edged up by INR 300-1,700/tonne (t).

Iron ore and pellet

- OMC conducted auctions for 2.249 mnt of iron ore (0.901 mnt of lumps and 1.348 mnt of fines) on 19 July. Around 1.304 mnt (97%) was booked at INR 2,550-5,350/t ex-mines, with a premiums of INR 50-850/t. 100% of lumps material was booked at INR 5,350-7,650/t, with premiums of up to 27% on base price. Bids (weighted average) increased by INR 150/t m-o-m and INR 175/t for fines and lumps, respectively. Earlier, OMC had lifted up base prices by INR 150/t m-o-m for few lots.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, rose by INR 200/t ($2.5/t) w-o-w to INR 9,900/t ($114/t) DAP Raipur on 18 July. Raipur-based pellet producers raised their offers for 63% (+/-0.5%) material by INR 200/t ($2.5/t) to INR 9,700-9,800/t ($112-113/t) exw.

- An India-based pellet maker recently concluded an export deal for 50,000 t of material (Fe63%, Al2O3+SiO2: 8%) through a tender at $109-109.5/t FOB India this week, as per sources. Another 50,000-t deal (Fe61%) was reportedly closed at $102.5-103/t FOB India at the start of the week.

- NMDC auctioned 185,000-t iron ore from Kumaraswamy, Karnataka, on 23 July. The entire quantity was booked, commanding premiums of up to INR 1,180/t for lumps and INR 1,510/t for fines. Specifically, 77,000-t lumps (10-40 mm, Fe 57.37-64.17%) were sold at INR 4,002-6,181/t against base prices INR 3,531-5,401/t. Meanwhile, 108,000-t fines (Fe 58.15-62.61%) were booked at INR 3,359-5,683/t against base prices INR 3,170-4,173/t. Prices include royalty, DMF, NMET.

Coal

- South African portside thermal coal offers in India rose again this week, with RB2 (5500 NAR) assessed at INR 7,800/t and RB3 (4800 NAR) at INR 6,800/t exw-Gangavaram – both up INR 150/t w-o-w. The increase stemmed from extended maintenance at RBCT and key rail link outages. However, demand remained tepid as buyers resisted firm offers. Portside stocks rose slightly to 16.13 mnt.

- Domestic 5000 GCV coal prices increased by INR 150/t w-o-w to INR 4,850/t exw-Bilaspur, while 4500 GCV held steady at INR 4,250/t. The rise was supported by a surge in sponge iron demand, with P-DRI prices jumping INR 1,700-1,800/t w-o-w. However, overall coal demand remained weak as SECL’s switch to end-user-only sales curtailed trader participation and kept spot market activity muted.

- BigMint’s PHCC index rose by $9/t w-o-w to $195/t CNF Paradip on 25 July, supported by a Panamax booking at similar levels for Aug shipment. Though Indian demand stayed low amid price uncertainty, sellers held back on hopes of further gains. Meanwhile, rising Chinese spot buying and firmer futures added to the positive sentiment.

- India’s met coke market shows stability as import activity stays limited due to pending approval of import quotas under the QR system. Prices stayed flat across Jajpur and Gandhidham at INR 29,000-29,100/t on steady demand and lack of fresh cargoes. Global cues were supportive as Australian PHCC edged up $3/t w-o-w and Chinese producers announced a second round of met coke price hikes.

Ferrous Scrap

- India’s imported scrap prices stayed stable this week as buyers resisted high offers due to soft finished steel demand and improved domestic scrap availability. No offers from UK/EU as Suppliers held back material as they secured higher prices of $20-22/t more from other markets such as Pakistan.

- Lastly heard offers for UK-origin shredded offers heard at $360-365/t CFR and HMS 80:20 at $335-340/t.

- Approximately 8,500-9,000 t of imported scrap has been booked to India over the past seven days, including 6,000 t of HMS 80:20 at $330-350/t. The remaining volume comprises LMS bundle mix, turning scrap, and HMS-LMS bundle mix.

Ferro alloys

- Silico Manganese:Indian silico manganese prices (60-14) remained largely stable with slight down by INR 150/t ($2/t) w-o-w to INR 72,300-72,800/t ($836-842/t) in the key regions of Durgapur, Raipur, and Vizag. Domestic silico manganese prices slipped week-on-week, pressured by weak demand from steel mills and limited new inquiries. A large domestic deal at reduced rates further pushed prices down.

- Ferro Manganese:Indian ferro manganese (HC 70%) prices remained steady with slight drop by INR 50/t ($1/t)w-o-w to INR 71,100/t ($822/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, were unchanged to INR 71,100/t ($822/t) w-o-w. Ferro manganese prices stay stable amid balanced supply-demand, steady steel production, and consistent buying from manufacturers maintaining market equilibrium.

- Ferro Silicon:Indian ferro silicon prices rose by INR 7,100/t ($82/t) w-o-w to INR 92,800/t ($1,073/t) exw-Guwahati. Meanwhile, Bhutanese prices increased by INR 5,700/t ($66/t) to INR 92,000/t ($1,064/t) exw. The recent price surge is driven by supply disruptions from power cuts at Meghalaya plants and a concurrent uptrend in imported silicon metal prices from China, tightening availability in the market.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices were largely stable with slight decline by INR 300 ($3/t) w-o-w at INR 99,300/t ($1,149/t) exw-Jajpur. Prices held steady following the recent Odisha Mining Corporation (OMC) chrome ore auction, in which no major variations were seen in bids.

- At OMC’s chrome ore auction on 19 July, 51,050 t were sold of the 73,100t offered. Bids showed mixed trends m-o-m, dropping by 0.1-2% (INR 10-465) for most grades and rising by 1-3% (INR 213-290/t) for some. As compared to the base prices, final bids fetched premiums of up to 4%.

Semi Finished

- Indian semi-finished steel prices showed increasing trend as per BigMint’s assessment. Domestic billet prices in all key locations improved by INR 300-1,300/t across regions. Major uptrend caught in Mumbai region by INR 1300/t. Sponge iron prices showing upward trend, almost all key locations moved up by INR 300-1,700/t and while major up shown in Jharsugda region.

- Indian DRI (Direct Reduced Iron) export offers increased by $4 stood at CPT Raxaul, at $329/t while, CPT Benapole offers seen decreased by INR 5/t and stands at $327/t.

- SAILs Rourkela Steel Plant (RSP) conducted an auction on 22 Jul’25 for 2,500 t of steel-grade pig iron in which the entire quantity was booked at an average price of INR 32,450/t exw – an increase of INR 250/t compared to the previous auction on 11 Jul in which the total quantity of 3,500 t was sold at INR 32,200/t exw.

Finished Long Steel

- IF-rebar:India’s induction furnace route finished long rebar prices rose this week, driven by active trading. Buyers have secured sufficient quantities, contributing to the upward trend. The primary reason behind the price hike in finished steel is the tight supply of key raw materials like sponge iron and billets. Manufacturers have received healthy forward bookings and report steady lifting of previously booked orders. In the near term, market participants expect prices to remain firm and well-supported.

On a weekly basis, in rebar steel prices witnessed surged in the range of INR 400-2,000/t across the regions as per BigMint assessment shows. - The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 40,800-41,200/t exw Raipur, INR 42,700-43,300/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 43,400-43,800/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 42,000-42,500/t ex Raipur.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 40,800-41,200/t exw Raipur, INR 43,700-44,300/t exw Jalna.

- BF-rebar:Trade-level blast furnace (BF) rebar prices declined w-o-w due to subdued demand across key Indian markets. Weak market sentiment, cautious buying, and monsoon-related disruptions kept buyers on the sidelines. While most market participants remain uncertain about a near-term price recovery, some believe prices may have reached a bottom, suggesting limited downside from current levels.

- Trade-level BF rebar prices declined by INR 900/t w-o-w to INR 47,500/t exy-Mumbai, as per BigMint’s assessment on 25 July 2025. Prices are exclusive of GST at 18%.

- In the projects segment, rebar prices increased w-o-w to INR 46,500–47,500/t FOR Mumbai basis, supported by improved bookings last week.

Flat Steel

- Trade-level prices of hot-rolled coils (HRCs) in India declined by up to INR 800/tonne (t) w-o-w to INR 48,800-50,600/t ($565-586/t) across markets. Moreover, cold-rolled coil (CRC) prices dropped by INR 500/t w-o-w to INR 54,500-59,000/t ($631-683/t).

- The Indian domestic HRC market is currently experiencing a significant slowdown in demand, influenced by a generally bearish market sentiment and sluggish sales activity. As buying interest continues to fade, both steel mills and traders are increasingly focused on clearing their existing inventories. To maintain some sales volume, they are reportedly even considering offering price support with talks of INR 2,000-2,500/t reductions, though unconfirmed.

- India’s bulk imports of HRCs touched 361,505 t as of 19 July, based on vessel line-up data. Around 236,660 t of additional cargo are expected by the first week of August.

- Indian HRC export offers to the EU declined amid reduced inquiries during Northern Europe’s summer holidays, with most buyers staying on the sidelines and waiting for clearer market direction post-holiday season.

- Moreover, Indian mills withheld offers amid firm domestic demand and rising competition in overseas markets.

Leave a Reply