- Semi-finished steel prices rise on improved buying interest and stronger billet demand across key markets

- Firm iron ore, coking coal costs offset by subdued scrap demand and cautious finished steel buying

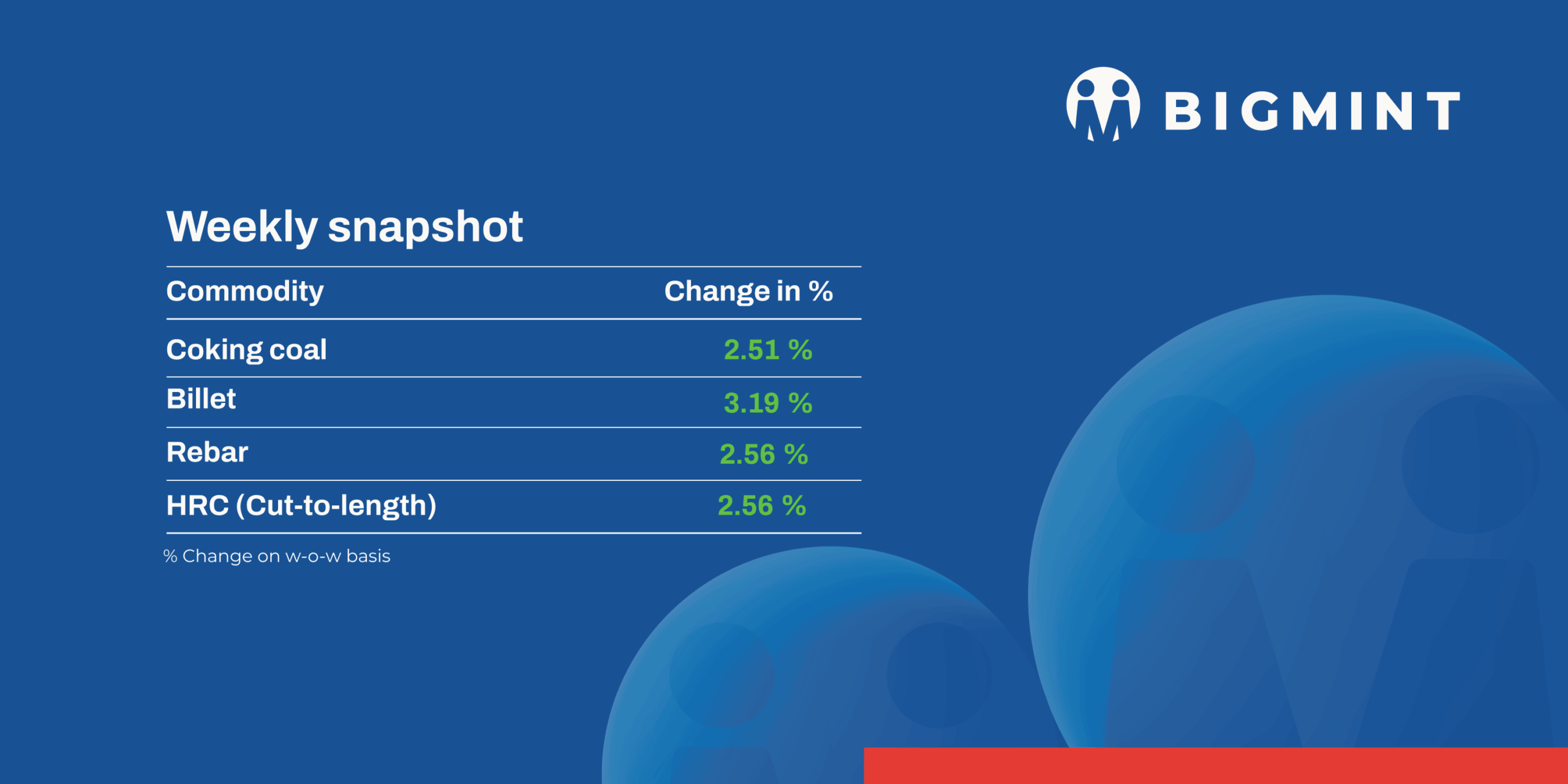

Steel prices in the domestic market rose in the week ended 19 December, as semi-finished steel prices edged up by between INR 200-1,200/tonne (t), across markets. Domestic induction furnace–route semi-finished steel offers rose in the range of INR 200-1,200 per tonne. Meanwhile, trade reference prices for HRC registered an increase amid rupee depreciation and elevated raw material costs during the week.

Iron ore and pellet

- In OMC’s iron ore fines auction for 2.22 mnt (Fe 51-62%) on 19 December, around 2.14 mnt (97%) was booked at INR 2,500-6,000/t. The lots received premiums ranging from INR 50 to 1,100/t, with INR 750/t being the average premium over base prices. Bids (weighted average) remained stable m-o-m.

- In OMC’s auction for 1.193 mnt of iron ore lumps (Fe 60-65%), the entire material was booked at INR 5,700-8,600/t, with premiums of INR 1,050-3,300/t. Weighted average bids dropped by around INR 250/t m-o-m, driven by a sharp decline in sponge iron prices. Earlier, OMC had also decreased the base prices of lumps by INR 400-750/t.

- Domestic iron ore prices in Karnataka’s Bellary region declined sharply w-o-w, weighed down by sluggish market activity and weak buying interest. BigMint’s weekly index for low-grade iron ore fines (Fe 57%) fell by INR 200/t ($2/t) to INR 2,800/t ($31/t) ex-mines, excluding taxes, as of 18 December, compared with the previous assessment on 11 December.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export prices increased by $1.5/tonne (t) w-o-w to $67/t FOB east coast on Thursday. BigMint heard approximately 100,000 t of export deals during this publishing period, which were primarily concluded over the last weekend. The discount is now floating in the market at around 19-21% for the Fe 57% fines cargo, while exporters are still targeting 18%, which is not attracting buyers for fresh deals.

Coal

- South African thermal coal offers strengthened further, but buying interest stayed weak. RB2 (5,500 NAR) was assessed at INR 8,900–8,950/t ex-Paradip, Vizag and Gangavaram, while RB3 (4,800 NAR) rose to around INR 7,550/t, up INR 50-150/t w-o-w. Higher exw offers of INR 9,200–9,250/t saw limited acceptance amid fragile sponge iron and steel demand, even as portside stocks stayed broadly stable at 13.07 mnt.

- Domestic coal prices softened again, with 5,000 GCV declining to INR 5,750/t and 4,500 GCV easing to INR 4,800/t, down INR 50–100/t w-o-w. Demand remained subdued, while supply comfort persisted after SECL’s 12 December auction, which allocated around 2.80 mnt out of the 3.22 mnt offered, reinforcing near-term availability.

- BigMint’s premium hard coking coal index rose sharply to $238/t CNF Paradip, up $11/t w-o-w and the highest in over a year. An eastern India mill booked 30,000 t at $238/t for Jan’26 loading, with another deal heard at $239/t. Australian PHCC prices climbed to $217/t FOB, while a weaker INR below 91 further lifted import costs.

- India’s met coke market showed divergence, with eastern prices steady and western markets under pressure. BF-grade met coke held at INR 32,000/t ex-Jajpur, while Gandhidham fell to INR 29,800/t, down INR 400/t w-o-w, and foundry-grade Rajkot eased to INR 35,800/t, down INR 200/t. Rising coking coal costs and weak offtake weighed on margins, while pig iron prices slipped to INR 32,100/t ex-Durgapur, down INR 150/t.

Ferrous scrap

- Imported scrap demand in India stayed subdued through the week as the rupee weakened to record lows near 91 against the dollar, pushing up import costs. Weak steel demand, year-end holidays, and cheaper domestic scrap restricted buying to urgent requirements.

- Falling steel prices, higher sponge iron usage in southern India, and ample scrap inventories in the north kept the market largely at a standstill.

- Prices remained rangebound despite weak sentiment, with EU-origin shredded at $345-350/t CFR west coast India and HMS 80:20 at $315-318/t CFR. Buyers capped shredded bids near $340/t, maintaining a wide bid-offer gap with western suppliers.

- Around 3,000-4,000 t of imported ferrous scrap was booked last week, comprising HMS 80:20 and HMS 90:10 from Somalia, Israel, and Mozambique.

Ferro alloys

- Silico Manganese:Indian silico manganese (60-14) prices edged down by around INR 175/t ($2/t) w-o-w to INR 68,500-69,400/t ($759-775/t) across Durgapur, Raipur, Vizag and Raigarh, as domestic mills continued cautious buying despite a mild improvement in steel demand. However, firm offers from key producers limited further downside.

- Ferro Manganese:Indian ferro manganese (70%) prices edged down by INR 400/t ($4/t) w-o-w to INR 71,600/t ($799/t) ex-works Raipur, while prices in Durgapur fell by INR 1,100/t ($12/t) w-o-w to INR 70,900/t ($791/t). Ample material availability and weak buyer demand weighed on prices, keeping trade activity subdued across key markets.

- Ferro Silicon:Indian ferro silicon (Si 70%) prices edged down by INR 600/t ($7/t) w-o-w to INR 97,000/t ($1,083/t) ex-works Guwahati, while prices in Bhutan declined by INR 1,600/t ($18/t) to the same level. The decline was driven by a few bulk purchases concluded at lower rates, while cautious buying sentiment continued to weigh on overall market activity.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices dropped by INR 1,700/t ($19/t) to INR 107,400/t ($1,190/t) exw-Jajpur. Limited inquiries and lower bids kept trading activity subdued, as market participants awaited the outcome of the OMC auction.

- At OMC’s chrome ore auction held on 19 Dec’25, 78,500 t were sold out of the 106,800 t offered. Bids for >40% grades declined by 5–12% m-o-m (INR 950–2,136/t), while <40% grades remained largely stable. Overall, bids were 0.4–3% (INR 100–700/t) above base prices.

- Vedanta-FACOR has scheduled an HC ferro chrome (Cr: 56% min, 0–150 mm) auction for 22 Dec’25.

Semi Finished

- India’s semi-finished steel market witnessed a significant surge this week, as per BigMint’s assessment. Domestic billet prices across major markets rose by INR 200-1,200/t ($2-11/t) w-o-w, supported by improved buying interest and a sharp increase in enquiries from neighbouring markets. Raipur, Jalna, Rourkela, and Raigarh lead the gains, recording price increases of INR 1,000-1,200/t ($11-13/t), on stronger billet bookings across the regions.

- In contrast, the sponge iron market witnessed a marginal improvement, with prices across major producing hubs increasing by INR 200-500/t ($2-5/t) w-o-w. Procurement activity remained modest for most of the week, keeping the market largely range-bound; however, a slight recovery in buying interest was observed toward the week-end, lending mild support to prices.

- SAIL-Rourkela Steel Plant (RSP) conducted an auction on 18 Dec’25 for 1,100 t of steel-grade pig iron, in which the entire quantity was booked at an average price of INR 33,750/t exw. This marks a rise of INR 1,800/t compared to the previous auction on 29 Nov’25, in which the entire quantity of 7,000 t was sold at INR 31,950/t exw.

- NMDC-Nagarnar Steel Plant held an auction on 18 Dec’25 for 10,000 t of steel-grade pig iron, of which 9,000 t were booked at an average price of INR 31,400/t exw. Bids increased marginally by INR 200/t compared with the previous auction on 9 Dec, in which 7,000 t were fully sold at INR 31,200/t exw.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for 12,000 t on 16 Dec, of which the entire quantity were booked at an average price of INR 30,300/t (by rake). However, management approval is still pending. In the previous approved auction, held on 17 Nov’25 for 12,000 t, entire quantity was booked at an average price of INR 30,000/t (by rake).

- Indian DRI export offers showed a mixed trend of ±$2/t w-o-w, assessed at $298/t CPT Raxaul for Nepal and $315/t CPT Benapole for Bangladesh. Despite stable-to-marginal price movements, export demand from both destinations remained limited amid cautious buying sentiment.

Finished Long Steel

- IF-rebar:India’s Induction Furnace (IF) route rebar prices edged higher on a week-on-week basis, supported by robust trading activity and sustained buying interest across spot markets. Mills continued to quote higher offers, supported by adequate order inflows in line with their daily production capacities. Enquiries were primarily driven by both project-based and retail consumers. Smooth execution of earlier bookings further reinforced positive market sentiment. Inventory levels at mills are currently assessed at a balanced 10–12 days across regions, and prevailing market conditions indicate a supportive outlook in the near term.

- On a weekly basis, prices in rebar steel witnessed increased in the range of INR 100-1,500/t across the regions as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 39,800-40,200/t exw Raipur, INR 44,700-45,300/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 42,000-42,500/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 40,800-41,300/t ex Raipur.

- BF-rebar:Indian trade-level BF-rebar prices moved within a narrow range in the week ending 19 December, with fluctuations limited to the INR 100-300/tonne (t) range. Prices also remained stable in some markets.

Buying activity saw marginal improvement following early-month price hikes, though overall, distribution channel demand remained subdued. Buyers also showed resistance to procuring material at higher prices, according to market participants. - Trade-level BF rebar prices were unchanged w-o-w at INR 47,500/t ($527/t) exy-Mumbai, as per BigMint’s benchmark assessment on 19 December 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered between INR 45,500-47,000/t ($504-521/t) FOR Mumbai.

Flat Steel

-

-

- India’s trade-level HRC prices registered an increase amid rupee depreciation and elevated raw material costs during the week ending 19 December, with prices hovering around INR 45,600-47,800/t ($502-526/t). Cold-rolled coil (CRC) prices were also mixed, ranging between INR 50,500 – 55,500/t ($555-610/t).

- Indian HRC market sentiments remain moderate this month, arrivals are low to moderate, supporting price stability across markets in north India informed a market participant. Overall market sentiment remains balanced, with no visible demand-driven momentum.

- India’s bulk imports of HRCs touched 125,753 t as of 12 December, based on vessel line-up data. Around 120,836 t of additional cargoes are expected by end-December.

- India’s bulk exports of HRCs touched 188,067 t as of 12 December.

- BigMint’s India HRC (S275) export index for the European Union (EU) held stable at $520/t FOB main port, with mills largely stepping back from issuing new offers amid CBAM-related uncertainty.

- BigMint’s India hot-rolled coil (HRC, SAE 1006) export index for the Middle East declined by $5/t w-o-w to $465/t compared with $470/t the previous week, as demand stayed weak ahead of the upcoming Christmas holidays in the region. A source told BigMint, “Following recent news on steel export licence requirements for Chinese companies buyers are holding back and closely monitoring the potential implications for regional supply.

-

Leave a Reply