The domestic steel market saw a positive trend in prices during week 13 ( 1-6 April, 2024). Semi-finished steel prices rose in the range of INR 1,400-2,900/tonne (t).

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, increased by INR 400/t w-o-w to INR 9,600/tonne (t) DAP Raipur on 5 April. Around 68,000 t of deals were recorded in the Raipur region in the last one week. Raipur pellet-makers recently increased offers by INR 400-500/t amid improved sponge and finished market sentiments.

- Vedanta has commenced mining of Block one iron ore mine in Bicholim, Goa, marking a resumption of pit mining in Goa after nearly six years, according to the company’s post on social media. The first to be auctioned in the state and one that was operated by its own unit Sesa Goa – quoting a revenue share of 63.55% in 2022.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) inched down by $1/tonne (t) to $92/t on 3 April. Seaborne pellet prices have continued to decline over the past few months amid bearish market sentiments and lack of transactions. Prices fell to four-year low the last time it reached such low levels was recorded in April 2020, as per data maintained with BigMint. No deals were heard in this publishing window amid a lack of inquiries from buyers and lower bids against offers. The demand for Indian raw pellets was negligible in China and other Southeast Asian countries.

- BigMint’s weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $3/t w-o-w to $55.5/t FOB east coast on 4 April. No deals were heard for standard Fe 57% fines in this publishing window amid low buying interest in the seaborne market and higher offers from sellers in the current market. Discounts have widened from 22-24% last week to 25-26% this week.

- Asia-Pacific supramax dry bulk (50,000-55,000 t) freight rates for an iron ore vessel from the east coast of India to China recorded a fall of $0.77/tonne (t) this week to $13/t on 3 April.

Coal

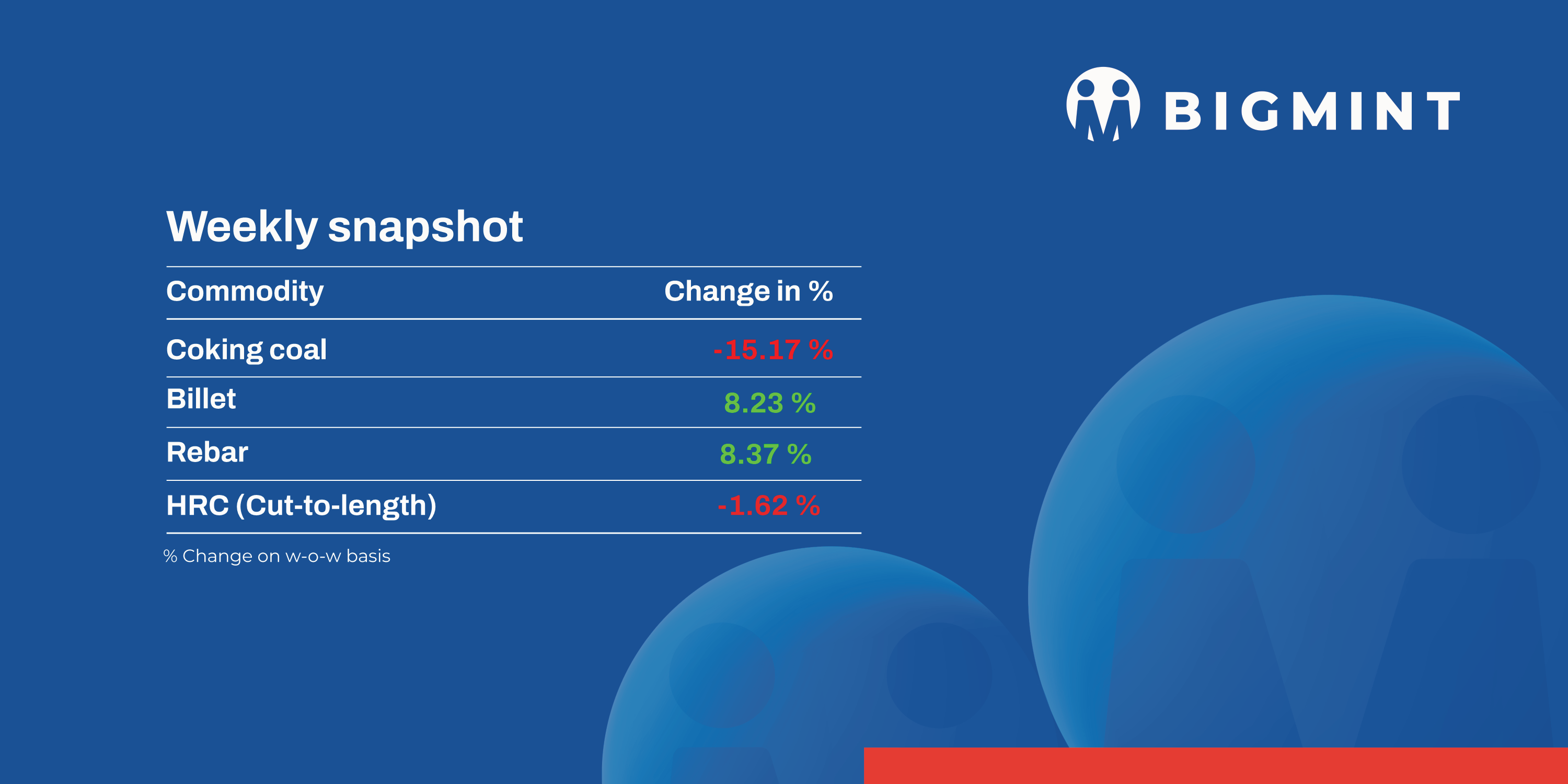

- Australian premium hard coking coal prices dropped 9% w-o-w to $224/t FOB and $241/ t CNF on 6 April amid reduced offer levels.

- RB1 (6000 NAR) coal prices rose by 4% w-o-w to $102/t FOB. Similarly, RB3 coal prices rose by 3% w-o-w to $68/t FOB Richards Bay, South Africa.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port were recorded at INR 8,000/t, stable w-o-w.

Ferrous Scrap

- In India, demand for imported scrap experienced a modest uptick this week as buyers sought alternatives amidst rising domestic scrap prices and supply shortage. While a few deals were finalised, market observers consider the recent surge in domestic prices temporary. Consequently, buyers seeking materials have begun turning to imported scrap.

- A Gujarat-based mill reportedly secured a bulk cargo deal comprising 30,000 t this week at approximately $415/t CFR, although specific details are not yet available.

- On a weekly basis, shredded scrap offers from Europe increased marginally by $2/t to $418/t CFR, up from $416/t CFR the previous week. Similarly, HMS (80:20) offers saw a slight uptick to $392/t, a $4/t rise compared to $388/t the week before.

Ferro Alloys

- Silico Manganese: As on 5 April, silico manganese prices in India increased by around INR 2,000/t ($24/t) w-o-w to INR 67,400-68,300/t ($809-820/t) exw in Raipur, Durgapur, and Vizag. The price uptick was driven by MOIL’s elevated ore offers, rising by 6% for grades above Mn44% and 3% for below Mn44% grade. Furthermore, reports of production cuts contributed to restricted material availability.

- Ferro Manganese: On 5 April, ferro manganese (HC70%) prices witnessed a w-o-w increase of INR 800/t ($10/t) and INR 900/t ($11/t) in Raipur and Durgapur, reaching INR 68,000/t ($816/t) exw, respectively. With only a few producers currently in operations and a slight uptick in demand, prices witnessed a rise.

- Ferro Silicon: On 5 April, Indian ferro silicon (FeSi:70%) prices saw a w-o-w decline of INR 500/t ($6/t), settling at INR 100,000/t ($1,199/t) exw-Guwahati. Similarly, Bhutan also experienced a drop of INR 600/t ($7/t) w-o-w, reaching INR 100,000/t ($1,199/t) exw. Following Bhutan’s announcement of new prices for the month, producers in both regions adjusted their prices accordingly.

- Ferro Chrome: On 5 April, prices of Indian high-carbon ferro chrome (HC60%, Si:4%) experienced a w-o-w decline of INR 1,600/t ($19/t) on 5 April, settling at INR 111,600/t ($1,338/t) exw-Jajpur. This drop is attributed to limited acceptance of sellers’ offers. Despite a slight increase in stainless steel prices for 304 grade, overall market volatility persisted.

Semi-Finished

- Indian semi-finished steel prices increased this week. Domestic billet prices increased sharply by INR 1,500-2,900/t in all key regions, with a major increase of INR 2,900/t in the Mandi Gobindgarh market. Similarly, sponge iron prices in all key locations also increased significantly by INR 1,400-2,750/t, with a major increase of INR 2,750/t in Jharsuguda.

- Tata Metaliks has announced a decrease of INR 1,000/t ($12/t) in pig iron (both basic and foundry grades) prices due to lack of demand at existing prices.

- Indian DRI (Direct Reduced Iron) export offers increased sharply by approximately $14-16/t, reaching $379/t on CPT Raxaul, and $386/t on CPT Benapole.

Finished long steel

- Finished long steel (IF route) prices showed continuity on rising trends this week. The hike in prices was propelled by active buying enquiries along with rising raw material prices. Such a market scenario created panic among buyers as they made sufficient bookings amid anticipation of further increase in offers. Thus, the purchase of rebar, structure and wire rod remained active throughout the week which supported price levels. Market participants are of the view that further hike in prices may impact booking volumes as traders are very cautious now about placing orders at higher rates.

- On a weekly basis, rebar prices surged in the range between 1,000-3,900/t across regions.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 46,400-46,800/t exw Raipur, and INR 50,300-50,900/t exw Jalna.

- Trade reference prices of heavy structural steel for base size 150mm channel stand at INR 48,000-48,300/t exw Raipur.

- Trade reference prices of wire rod are hovering at INR 46,300-46,800/t ex Raipur.

- BF route: Prices of IF-rebars increased sharply during the week amid improved demand and price support from semi-finished steel. This nudged primary steel manufacturers to raise rebar prices up to INR 1,000/t for early-April dispatches in order to maintain the price gap between BF-IF rebars. Following this, trade-level prices of BF-rebar increased by INR 400-1,500/t w-o-w across major markets; meanwhile, demand in the traders’ market remained subdued during the week.

- Rebar (12-32mm, Fe500D) prices in the trade segment rose by INR 700/t w-o-w to INR 53,400/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the projects segment, prices increased by INR 1,000/t against last week and are currently hovering at INR 51,000-51,500/t FOR Mumbai.

Finished flat steel

- Primary steel mills have announced an increase in list prices for hot-rolled coils (HRC) and cold-rolled coils (CRC) for April. HRC prices are around INR 53,500-54,000/t while CRC prices are INR 58,800-60,500/t ex-Mumbai. Market trends show targeted purchasing driven by specific needs, with concerns about inventory levels and liquidity constraints.

- Monthly average prices of trade-level hot-rolled coils (HRC, IS2062, Grade E250, 2.5-8mm) have registered a decline, decreasing by approximately INR 1,100/t to reach INR 52,800/t in March as opposed to the previous month’s INR 53,900/t exy-Mumbai. Simultaneously, cold-rolled coils (CRC, IS513, Gr-O, 0.9mm) have experienced a reduction of INR 400/t on a m-o-m basis, settling at INR 61,300/t exy-Mumbai in March compared to the preceding month’s INR 61,700/t.

- BigMint’s India HRC (SAE 1006) export index (for the Middle East and Vietnam) fell by $8/t w-o-w to $567/t against $575/t FOB east coast India.

- Bulk HRC export volumes have been increasing since 47,688 t recorded in December 2023, as per vessel line-up data maintained.

- Volumes of bulk HRC imports dropped to 381,794 t in March.