Domestic induction furnace-finished long steel prices showed positive trends this week even as the focus shifted towards the secondary steel market.

- Iron ore and pellet

BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, remained stable w-o-w at INR 9,200/tonne (t) DAP Raipur on 29 March. Only 4,000 deals were recorded in the Raipur region due to weak market sentiments amid the festive season and the financial year coming to an end. The local plants from the Raipur kept their pellet offers stable compared to last week - In the NMDC auction from Chhattisgarh conducted on 29 March, 42,000 t of iron ore DRCLO (10-40 mm, Fe 67%) got booked at the base price of INR 7,030/t and 105,000 t of iron ore fines (Fe 64%) got booked at INR 5,140/t against the base price of INR 5,100/t from Bacheli mines. However, 12,600 t of ROM (10-150 mm, Fe 65.5%) from Bacheli and 84,000 t of ROM (10-150 mm, Fe 65.5%) from Kirandul received no bid. Prices were set on FOR basis, including royalty, DMF, and NMET.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) inched down by $3/tonne (t) to $93/t on 27 March. The seaborne market for Indian material continued to face bearish sentiments as bids dropped further this week amid a lack of buying interest. Pellet manufacturers remained in wait-and-watch mode amid sluggish market sentiments for high-grade material in China.

- Asia-Pacific Supramax dry bulk (50,000-55,000 t) freight rates for an iron ore vessel from the east coast of India to China recorded a drop of $0.7/tonnes (t) this week at $13.77/t on 27 March, as per BigMint assessment. Dry bulk iron ore freight rates have declined this week in key routes. Weak demand from Chinese buyers amid constant increases in port stocks and the availability of vessels in major routes have weighed on freight rates. However, Australian miners have floated inquiries that have contributed to maintaining the tonnage demand. Notably, market participants have enquired about smaller vessels from the Indian Ocean, but inquiries are under negotiation.

Coal

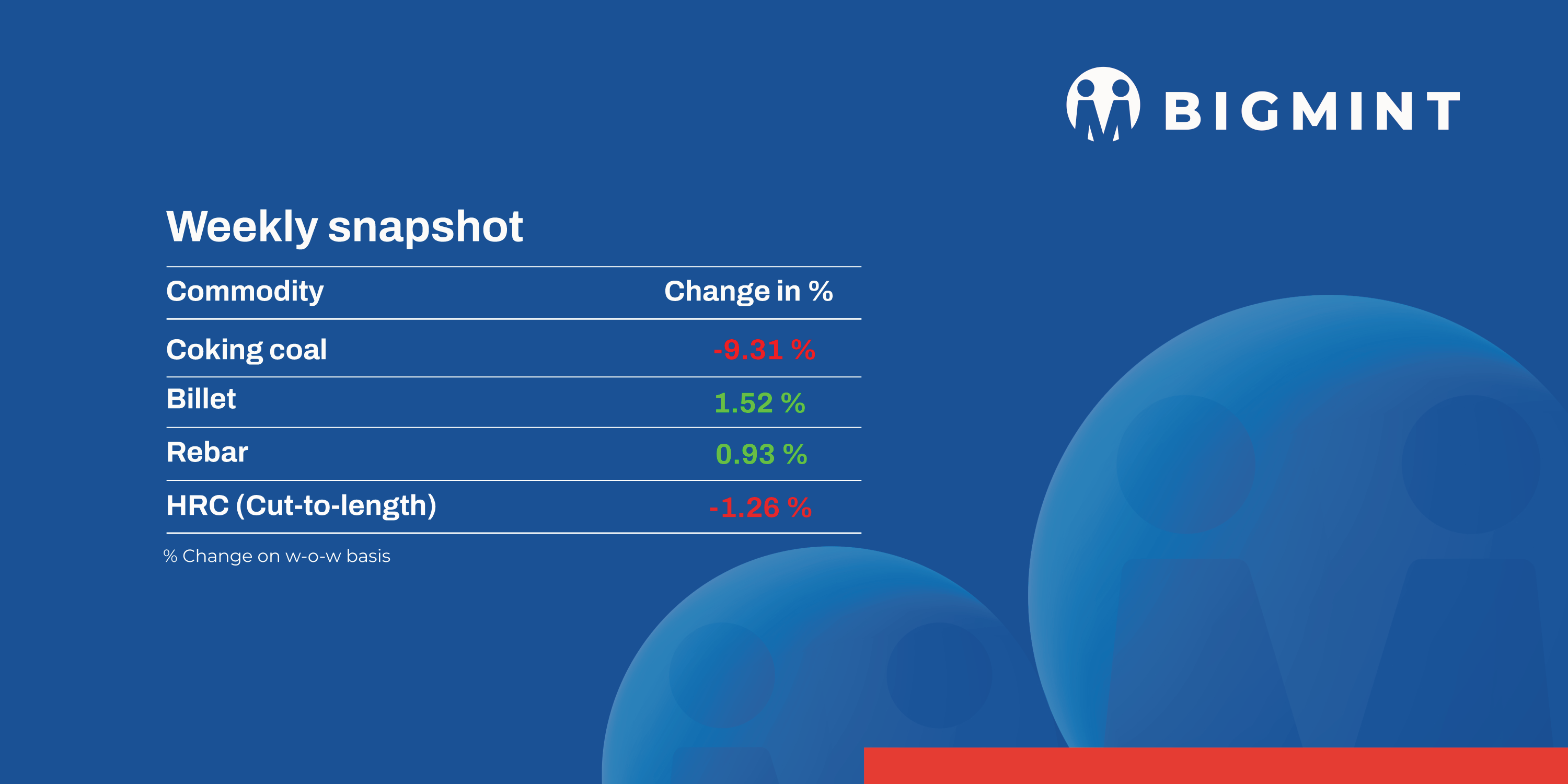

- Australian premium hard coking coal prices remained unchanged w-o-w at $245/t FOB and $263/ t CNF on 30 Mar’24 amid tepid demand.

- RB1 (6000 NAR) coal prices remained stable w-o-w to $98/t FOB. Similarly, RB3 remained unchanged w-o-w at $66/t FOB Richards Bay, South Africa.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port recorded at INR 8,000/t,stable w-o-w.

Ferros Scrap

- Indian buyers exhibited minimal interest in purchasing fresh scrap from the international market due to disparities in bid-offer prices, as well as the availability of more cost-effective domestic alternatives such as local scrap and sponge iron. Moreover, with a week-long holiday during the Holi festival, key participants were in a holiday mood, further dampening market activity.

- On a weekly average, shredded scrap offers from Europe and the US were priced at $416/t CFR and $408/t CFR, marking an increase of $9/t and $7/t respectively. Additionally, HMS (80:20) scrap offers saw a marginal uptick of $10/t to $398/t CFR for the week. The rise in offers was due to firm stance from suppliers due to higher collection costs and active buying from Turkiye, the largest scrap importer.

- Throughout the week, approximately 1200-1300 t of shredded scrap were contracted from the US within the price range of $405-408/t CFR. Additionally, around 1000 t of HMS (80:20) scrap were secured from Yemen and West Africa at prices ranging from $365-375/t CFR.

Ferro Alloys

- Indian silico manganese prices were stable with a marginal rise in prices of INR 250/t ($3/t), as per BigMint data. On 29 March, silico manganese (60-14) was trading at around INR 65,800-65,900/t ($789-$790/t) exw Durgapur, Raipur, and Vizag.

- Ferro Manganese: Ferro manganese (HC70%) prices remained rangebound with a marginal hike seen. Ferro manganese prices in Raipur and Durgapur on 29 March were at INR 67,100/t ($805/t), up by INR 100/t ($1/t), and INR 67,200 ($806/t), up by INR 200/t ($2/t), respectively.

- Ferro Silicon: As of 29 March, BigMint reported ferro silicon prices in India at INR 100,600/t ($1,206/t) exw-Bhutan, down by INR INR 400/t ($5/t) and INR 100,500/t ($1,205/t) exw Guwahati, down by INR 1,100/t ($13/t). Prices fell as demand remained at a moderate level and there was enough material available to meet market requirement.

- Ferro Chrome: On 29 March, Indian ferro chrome (HC 60%, Si:4%) prices fell by INR 800/t ($10/t), reaching INR 113,200/t ($1,358/t) exw-Jajpur. Market participants continued to wait for clarity regarding the direction of prices.

Semi-Finished

- Indian semi-finished steel prices increased, as per BiglMint’s assessment. Domestic billet prices increased by INR 100-650/t in all key regions, with a major increase of INR 650/t seen in the Durgapur market. Similarly, sponge iron prices in almost all key locations increased by INR 300-700/t, with a major increase of INR 700/t seen in the Durgapur and Ramgarh markets. However, sponge iron prices in Bellary fell by INR 50-100/t.

- SAIL’s Durgapur Steel Plant (DSP) held an auction for 2,000 t of steel-grade pig iron on 27 March. The total quantity was booked at an average price of INR 37,400/t exw.

- Indian DRI (Direct Reduced Iron) export offers increased by approximately $1-4/t, reaching $363/t CPT Raxaul and $372/t CPT Benapole.

Finished long steel

- BF-rebar: Trade-level prices of blast furnace (BF) rebars witnessed an uptick w-o-w across markets amid moderate buying activities. Prices remained supported for the past couple of weeks as mills opted for production cuts due to mounting inventories at their yards and announced interim price hikes. There was slight improvement in activities this week ahead of financial year-end.

- This week, rebar prices (12-32mm, Fe500D) in the trade segment rose by INR 300/t w-o-w to INR 52,700/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the projects segment, prices are hovering around INR 50,000-50,500/t landed Mumbai basis.

Finished flat steel

- Hot-rolled coil (HRC) (IS2062, Gr E250, 2.5-8mm) prices fell across markets this week, with trade activities taking a backseat with the fiscal year coming to a close. Some markets viz. Chennai (- 2,200/t), Bangalore (- INR 1,000/t), and Kolkata (- INR 1,000/t) showed steel declines in prices w-o-w. However, cold-rolled coil (CRC) coil (IS513, Gr O, 0.9mm) prices remained rangebound across most markets this week with the exception of Delhi (- INR 1,300/t), and Kolkata (- INR 1,000/t).

- Trading activities remained subdued amid low buying appetite, and clearance of MOUs with the financial year drawing to a close. Market sources expect tight liquidity conditions ahead of the general elections and are exercising caution in maintaining inventory levels. The Holi holidays had kept the market inactive for over a week.

- BigMint’s India HRC (SAE 1006) export index (for the Middle East and Vietnam) stood unchanged at $575/t FOB east coast India after having dropped $15/t in the preceding week.

- Weekly assessed imported hot rolled coil (HRC) prices dropped in Vietnam and the Middle East because of subdued demand and competitive domestic prices. Chinese HRC export offers receded by $10-25/t, while offers from India also edged down. Indian HRC (S275, 3mm+) export offers for Europe remained steady, with reduced activity levels amid the Easter holidays.

- India’s exports of bulk HRC and plates were 597,885 t till 27 March, according to vessel line-up data tracked by BigMint.