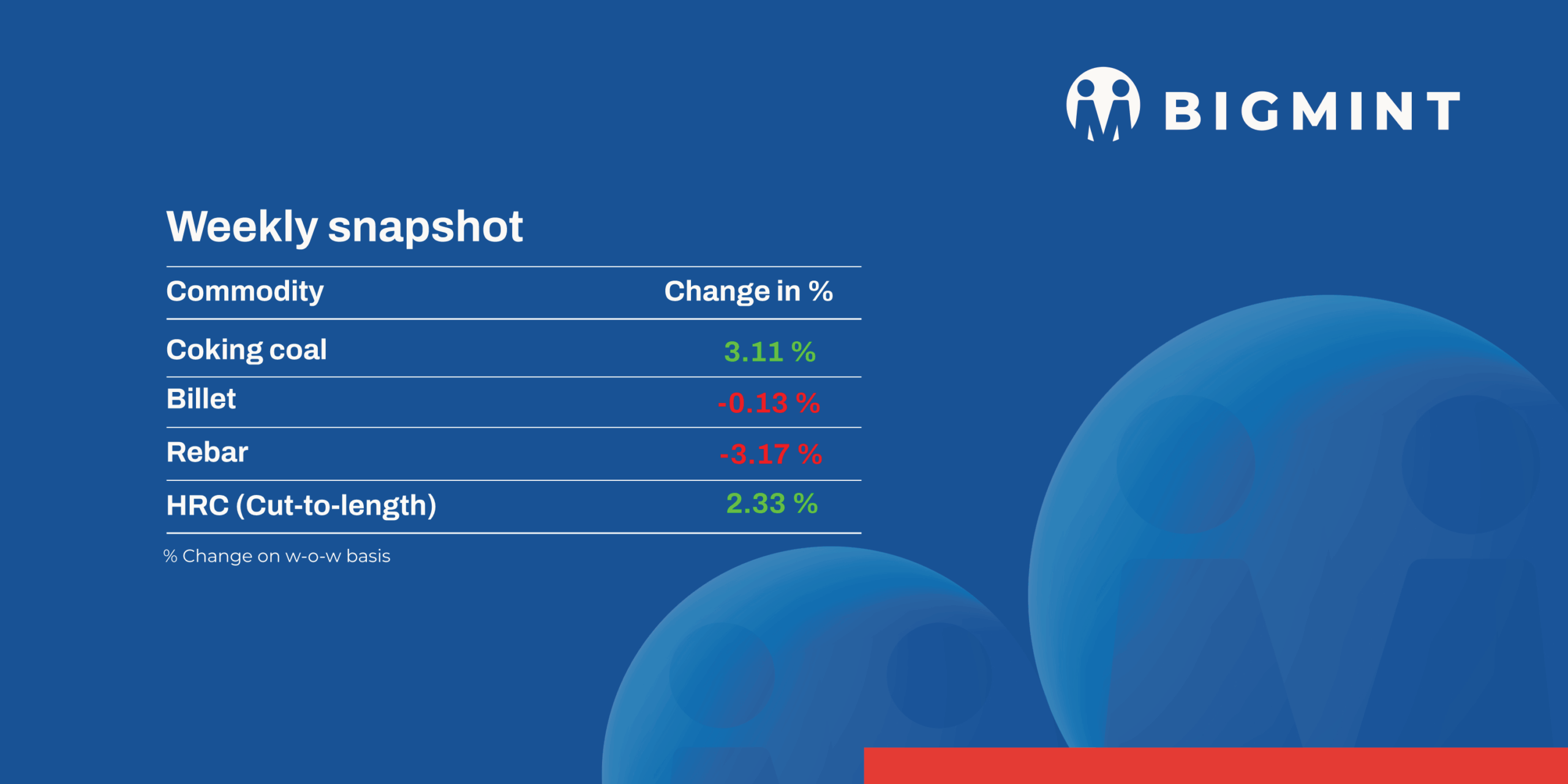

The domestic steel market witnessed a negative trend in prices during week 30 (28 July-2 Aug, 2025). Semi-finished steel prices fell in the range of INR 50-700/tonne (t).Trade reference prices for hot rolled coil (HRC) and cold rolled coil (CRC) rose up to INR 1,000/t.

Iron ore and pellet

- NMDC increased its list prices of iron ore calibrated lump ore (CLO) and fines for August deliveries on 1 August, BigMint learnt from sources. The miner fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 6,850/t ($78/t) and of iron ore fines (-10 mm, Fe 64%) at INR 5,250/t ($60/t), an increase of INR 450/t ($5/t) and 400/t ($4.5/t), respectively. Prices are on FOR basis from the miner’s Bacheli complex and include royalty, DMF, and NMET.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, rose by INR 150/t ($2/t) w-o-w to INR 10,050/t ($115/t) DAP Raipur on 1 August. Raipur-based pellet producers raised their offers for 63% (+/-0.5%) material by INR 200/t ($2.5/t) to INR 9,900-10,000/t ($114-115/t) exw. Deals were concluded on need basis amid cautious buying behaviour.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index fell by $2/t w-o-w to $64/t FOB east coast on 31 July. Around 165,000 t of Fe 55-57% fines were sold at $72-76/t CFR China in this publishing window. Trade activity remained subdued over the past few days as market participants grappled with negative price fluctuations in the seaborne market.

Coal

- South African thermal coal offers surged at Indian ports this week amid rising freights and tight supply. RB2 was assessed at INR 8,100/t and RB3 at INR 7,050/t exw-Gangavaram, up INR 300/t and INR 250/t w-o-w. Vizag saw sharper d-o-d hikes of INR 650/t (RB2) and INR 350/t (RB3), driven by Panamax freight rise and low August availability. Sponge buyers started booking for September amid firm price outlook.

- Domestic coal prices have moved up this week despite a lacklustre market. BigMint assessed 5000 GCV at INR 5,000/t and 4500 GCV at INR 4,400/t exw-Bilaspur – both up INR 150/t w-o-w. SECL’s lower e-auction frequency during the monsoon has trimmed market availability, lending support to prices. However, demand from traders and industries remains muted as most buyers are waiting for clearer signals on post-monsoon recovery.

- BigMint’s PHCC index slipped $1/t w-o-w to $194/t CNF Paradip as of 1 Aug. Bids remained below $195/t while offers from Australian suppliers held at $197-200/t CFR, causing limited trade. A recent FOB deal for Goonyella was heard at $188.82/t. Canadian offers hovered lower at $182-185/t CFR. With no confirmed trade in the index window, cautious sentiment continues amid widening bid-offer gaps.

- India’s met coke prices remained steady this week with better trade activity. BF-grade met coke held at INR 29,000/t in Jajpur and INR 29,800/t in Gandhidham. Imports stayed paused as quota approvals under the QR system remain pending. Chinese met coke prices continued rising for the fourth straight time, driven by firm demand and low coke stocks and to launch a fifth round of price increases.

Ferrous Scrap

- India’s imported scrap market saw a modest price gain this week, with shredded averaging $368/t, up 2% from last week’s $361/t. UK-origin shredded was heard at $360-365/t CFR, while HMS hovered near $345/t CFR, though procurement stayed limited as suppliers diverted cargoes to Pakistan and domestic demand remained weak.

- Firming iron ore and sponge iron prices lent support, with EU-origin shredded offers climbing to $370-375/t CFR and UK HMS to $340-345/t. Expectations of higher finished steel prices in August lifted sentiment, but Indian mills continued to book selectively.

- Around 5,700-6,500 t of imported scrap was booked for India over the week, including 2,500-3,000 t of HMS 80:20 at $330-345/t, with the balance comprising HMS-LMS bundles, LMS, and HMS-PNS mix.

Ferro alloys

- Silico Manganese:Indian silico manganese prices (60-14) down by INR 650/t ($7/t) w-o-w to INR 71,800-72,000/t ($823-826/t) in the key regions of Durgapur, Raipur, and Vizag. The decline is due to excess supply and demand limited to immediate requirements from steel mills, reflecting cautious buying and oversupply in the market.

- Ferro Manganese:Indian ferro manganese (HC 70%) prices remained steady with slight drop by INR 150/t ($2/t)w-o-w to INR 70,950/t ($814/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, were unaltered to INR 71,100/t ($815/t) w-o-w.Stable demand and balanced supply kept ferro manganese prices mostly steady, with minor corrections driven by limited trade activity and sufficient producer inventory in key regions.

- Ferro Silicon:Indian ferro silicon prices rose by INR 2,500/t ($29/t) w-o-w to INR 95,300/t ($1,093/t) exw-Guwahati. Meanwhile, Bhutan offers increased by INR 3,000/t ($34/t) to INR 95,000/t ($1,089/t) exw. Prices rose sharply as seller offers increased, driven by rising imported silicon metal prices from China.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices were largely stable with slight rise by INR 700 ($8/t) w-o-w at INR 100,000/t ($1,147/t) exw-Jajpur. With weak demand for stainless steel and key sellers being sold out, supplies were a bit restricted which marginally pushed up the prices.

Semi Finished

- Indian semi-finished steel prices showed decreasing trend as per BigMint’s assessment. Domestic billet prices in all key locations moved down by INR 50-700/t across regions. Except Goa region shoot up by INR 800/t. Sponge iron prices also showing diminishing trend, almost all key locations moved down by INR 100-700/t and while up rising trend shown in Mandi Gobindgarh and Chennai by INR 200-500/t region.

- Indian DRI (Direct Reduced Iron) export offers increased by $2 stood at CPT Raxaul, at $331/t while, CPT Benapole offers seen increased by INR 7/t and stands at $334/t.

Finished Long Steel

- IF-rebar: India’s induction furnace route rebar market showed a mixed trend this week amid moderate trading. With buyers having procured sufficient quantities earlier, fresh bookings were limited to immediate needs. Manufacturers, aiming to liquidate remaining stock, offered marginal price cuts or discounts. Demand from both retail and project segments improved, leading to steady dispatches and a drop in inventories to 10-12 days from the previous 15-17 days in some regions. Market sentiment remains cautiously optimistic, with near-term price direction likely to hinge on raw material trends.

On a weekly basis, in rebar steel prices witnessed varied in the range of INR 200-1,000/t across the regions as per BigMint assessment shows.The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 39,500-39,900/t exw Raipur, INR 43,400-44,000/t exw Jalna.Trade reference price of heavy structural steel for base size 150mm channel stands at INR 42,800-43,200/t exw Raipur.Trade reference prices of wire rod hovering at INR 41,500-42,000/t ex Raipur.

- BF-rebar: India’s trade-level blast furnace (BF) rebar prices witnessed an increase w-o-w across major Indian markets. Certain mills raised list prices in late-July, and market participants expect steelmakers to announce further hikes for August. This lent support to trade-level prices, improving sentiments in the segment.

- Trade-level BF rebar prices increased by INR 500/t w-o-w to INR 48,000/t exy-Mumbai, as per BigMint’s assessment on 1 August 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices stood at INR 47,000-48,000/t FOR Mumbai, an increase of INR 500/t w-o-w. Mills sold strong volumes last month, as prices bottomed out during late-July.

Flat Steel

- Trade-level prices of hot-rolled coils (HRCs) in India showed mix-trends w-o-w as some markets reported a rise of upto INR 1000/tonne (t) w-o-w to INR 48,900-50,700/t ($565-586/t). Moreover, cold-rolled coil (CRC) prices rose by upto INR 700/t w-o-w to INR 55,000-59,000/t in others.

- Currently, steel manufacturers are signalling a potential price support of INR 1,000-1,500/t in the August sales cycle.

- India’s bulk imports of HRCs touched 441,130 t as of 26 July, based on vessel line-up data. Around 243,917 t of additional cargoes are expected by the first week of August.

- India’s bulk exports of HRCs touched 65,401 t as of 26 July, based on vessel line-up data with BigMint. Moreover, around 65,000 t of additional cargo is expected to be exported by end of July month.

- An improved global market and higher Chinese export prices have led to a $5/tonne increase in BigMint’s India hot-rolled coil (HRC) export index, bringing it to $540/tonne (FOB).

- Despite this, the Middle East market remains slow. Indian mills have stopped offering HRC to the region due to strong domestic demand and stiff competition from other suppliers, even though Chinese prices have gone up.

Leave a Reply