- NMDC’s iron ore auction fetches premium

- Tier-1 mills cut HRC prices from early-Sep’25 levels

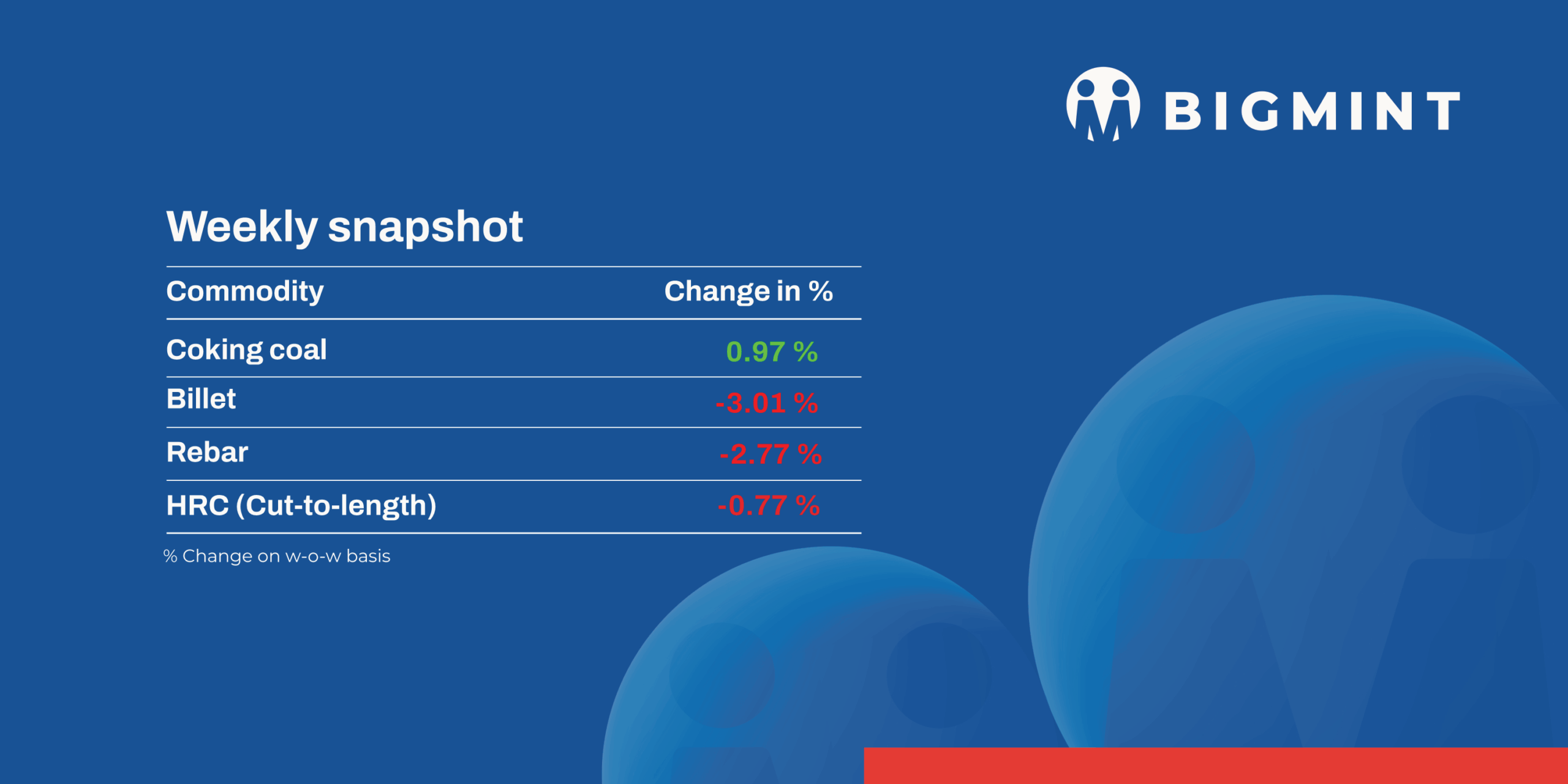

Domestic induction furnace finished long steel offers witnessed a downtrend this week as prices dropped INR 300-1,100/t. Trade reference prices for hot rolled coil (HRC) and cold rolled coil (CRC), too, fell by INR 750-1,500/t.

Iron ore and pellet

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index rose by $3/tonne (t) w-o-w to $69/t FOB east coast on 9 October. Market activity stayed muted during China’s holidays as buyers stayed away, but sentiment picked up slightly as steel mills resumed operations thereafter.

- NMDC scheduled an iron ore auction from its Bacheli mines, Chhattisgarh, on 9 October. Of the 43,000 t of fines offered, 21,500 t (Fe 64%) were sold at INR 5,290/t, and 2,000 t of ROM (Fe 65.5%, 10-150 mm, 6,000 t offered) were sold at INR 6,050/t. All 4,000 t of lumps (Fe 65.5%, 10-20 mm) received a 9.5% premium over the base price of INR 6,300/t. Prices are including royalty, DMF and NMET.

- BigMint’s bi-weekly assessment for India’s iron ore concentrates remained stable at INR 4,700/tonne (t) ($53/t) exw-Jabalpur, unchanged from the previous evaluation on 4 October, while falling by INR 100/t ($1/t) w-o-w. Prices held largely firm amid steady buying interest and limited market movement. Overall, deals for around 20,000-24,000 t were concluded at around INR 4,600-4,700/t exw.

Coal

- South African portside coal prices in India stayed stable this week, supported by steady demand after the holidays. RB2 was assessed at INR 8,200/t and RB3 at INR 7,100/t across Paradip, Vizag, and Gangavaram. Around 100,000 t of trades were reported, including two RB2 deals at INR 8,150-8,200/t ex-works. Market outlook remains firm for November amid supply concerns at Richards Bay terminal.

- India’s domestic coal market stayed quiet this week amid uncertainty over SECL’s new grade upgradation policy. Prices for 5,000 GCV coal held at INR 6,250/t ex-Bilaspur, while 4,500 GCV slipped INR 100/t to INR 5,200/t. Traders avoided fresh bookings due to delivery delays and limited lifting, leading to emerging supply concerns in the near term.

- India’s met coke market showed a mild upward trend in the week ending 9 Oct 2025. Prices in east India increased by INR 400/t w-o-w to INR 29,900/t ex-Jajpur, with a deal heard at INR 30,500/t, supported by improved post-festive steel demand and supply issues in Australia. In contrast, west India remained steady at INR 30,000/t exw-Gandhidham amid weak buying. Foundry-grade coke held firm at INR 35,600/t ex-Rajkot.

- BigMint’s premium hard coking coal (PHCC) index was assessed at $205/t CNF Paradip on 10 October, down $2/t w-o-w. A single deal of 75,000 t Australian-origin PHCC was booked at $203/t CFR India for end-Oct shipment, while bid-offer gaps limited further trades.

Ferrous scrap

- India’s imported scrap market stayed subdued through the week as Dussehra holidays and weak steel demand limited buying. Offers for shredded hovered at $355-360/t CFR, while buyers targeted $350/t and Offers for HMS 80:20 are at $325-330/t with tradable level is below $325/t , keeping trade minimal.

- A strong dollar, high freight rates, and poor domestic steel sales further dampened sentiment. Mills avoided restocking amid unviable import prices, especially for HMS and busheling grades with most buyers resisting current offers and waiting for post-festival demand clarity before resuming fresh bookings.

- In the last seven days, around 3,500-4,500 t of imported scrap were booked, including 1,000–1,500 t of HMS 80:20 at $318-325/t, while the rest comprised HMS 90:10, NTP, LMS bales, and turning scrap.

Ferro alloys

- Silico manganese: Indian silico manganese (60-14) prices increased by INR 1,050/t ($12/t) w-o-w to INR 70,300–71,000/t ($792–800/t) in key regions like Durgapur, Raipur, and Vizag. Spot market availability tightened as traders and smelters held limited inventories, compelling buyers to accept higher prices while smelters focused on fulfilling existing bulk orders.

- Ferro manganese: Indian ferro manganese (HC 70%) prices rose slightly w-o-w by INR 500/t ($6/t) w-o-w to INR 70,900/t ($792/t) exw in Durgapur. Meanwhile, prices, exw-Raipur, also inched up by INR 700/t($8/t) to INR 71,000/t ($800/t) w-o-w. Prices rose due to material shortages and supply constraints, despite weak demand from the steel sector.

- Ferro silicon: Indian ferro silicon (Si 70%) prices inched down by INR 1,300/t ($15/t) w-o-w to INR 87,000/t ($981/t) exw-Guwahati. Meanwhile, Bhutanese offers also fell slightly by INR 1,000/t ($11/t) to INR 87,000/t ($981/t). The decline followed Bhutan’s October offer release and steady imports of silicon metal and ferro silicon, which softened domestic demand.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si 4%) prices rose by INR 1,700/t ($19/t) w-o-w to INR 120,400/t ($1,357/t) exw-Jajpur. While most bulk deals settled at INR 118,000–119,000/t($1,330-1,341/t) exw levels, some reached INR 122,000/t ($1,375/t). Buyers remained cautious amid higher offers.

- Meanwhile, during Vedanta-FACOR’s ferro chrome auction on 8 October, the 10–150 mm larger lot recorded an H1 price of INR 120,800/t ($1,361/t) exw, rising INR 4,800/t ($54/t) over the base, with overall bids 3-4% higher than base levels.

Semi finished

- Indian semi-finished steel prices continued to decline this week, as per BigMint’s assessment. Domestic billet prices across key locations fell by INR 400-900/t ($4-10/t), weighed down by weak demand in both semi-finished and finished steel segments, leading to a notable w-o-w drop in spot prices. Similarly, sponge iron prices declined by INR 300-750/t ($3-8/t) across regions as limited market participation and subdued buyer inquiries prompted further correction. Although slight volatility in market sentiment supported moderate bookings in sponge iron and billet, sustained recovery remains constrained by the lack of demand from the finished steel segment.

- SAIL’s Rourkela Steel Plant (RSP) conducted an auction on 8 October for 3,200 t of steel-grade pig iron, in which the entire quantity was booked at an average price of INR 32,350/t exw. This marked a decrease of INR 250/t compared to the previous auction on 20 Sep, in which a total quantity of 5,500 t was sold at INR 32,600/t exw.

- SAIL-Bhilai Steel Plant (BSP) conducted an auction for around 692 t of CC defective billets, covering sizes up to 110 mm and above 110 mm. During the auction, approximately 206 t above 110 mm were sold at an average price of INR 38,300/t, while 210 t up to 110 mm were booked at an average price of INR 37,050/t. However, a small part of the offered quantity remained unsold

Finished long steel

- IF-rebar: India’s IF route finished long steel prices experienced a decline w-o-w, primarily driven by selling pressure in the market due to high inventory levels and subdued demand. Sluggish offtake from end-users led to an accumulation of stocks, compelling major manufacturers to opt for production cuts in various regions. Trading remained confined to immediate needs as buyers stayed cautious amid weak demand. As per given scenario, market is expected to stay volatile in the near term.

- On a weekly basis, in rebar steel prices witnessed decreased in the range of INR 200-1,000/t across the regions as per BigMint assessment shows.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 38,400-38,800/t exw Raipur, INR 42,400-43,000/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 40,800-41,200/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 38,400-39,000/t ex Raipur.

- BF-rebar: Indian primary mills have increased rebar prices by up to INR 1,000/t ($11/t) for early-October deliveries as against prices prevailing in end-September, sources informed BigMint. Post-revision, list prices stood at INR 47,000-48,500/t ($530-546/t) on landed basis.

- Trade-level BF rebar prices edged down by INR 100/t ($1/t) w-o-w to INR 47,100/t ($531/t) exy-Mumbai, as per BigMint’s assessment on 10 October 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices stood at INR 46,500-47,500/t ($524-535/t) FOR Mumbai basis for early-October dispatches.

- Rebar inventories at Tier-1 mills increased by 4% m-o-m in early-October as against inventories in early-September owing to sluggish sales last month.

Flat steel

- Leading Indian steel manufacturers have decreased prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 750-1,500/t ($8-17/t) for October sales as compared to the list prices of early-Septembe. However, from the net sales prices of end-September, prices have been raised by around INR 500/t ($6/t) for October.

- BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 200/t ($2/t) w-o-w to INR 48,300/t ($544/t) on 7 October 2025 against INR 48,500 ($546/t) on 30 September 2025. Moreover, CRC (IS513, Gr O, 0.9 mm/CTL) prices fell by INR 200/t ($2/t) w-o-w to INR 55,700/t ($628/t) on Tuesday against INR 55,900/t ($630/t). These prices are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

- India’s HRC market remained sluggish as slow demand, oversupply, and high inventories pressured prices. Buyers limited purchases to immediate needs, avoiding bulk bookings. Thin margins, heavy stocks, and festive holidays such as Durga Puja further dampened trading activity and delayed recovery prospects.

- India’s bulk imports of HRCs touched 464,694 t as of 30 September, based on vessel line-up data. Around 144,709 t of additional cargoes are expected by the first week of October.

- India’s bulk exports of HRCs touched 203,541 t as of 30 September 2025, based on vessel line-up data with BigMint. Around 10,000 t of additional cargo are in transit.

- BigMint’s Indian hot-rolled coil (HRC, S275) export index for Europe held steady w-o-w at $545/t FOB main port, with trading activity subdued and no significant discussions underway, likely due to the EU’s Carbon Border Adjustment Mechanism (CBAM).

- The India HRC (SAE 1006) export index for the Middle East and Vietnam remained stable w-o-w. Notably, “Middle East customers are likely to maintain minimal inventory levels as they near the close of their financial year (FY) in December,” as per a source.

Leave a Reply