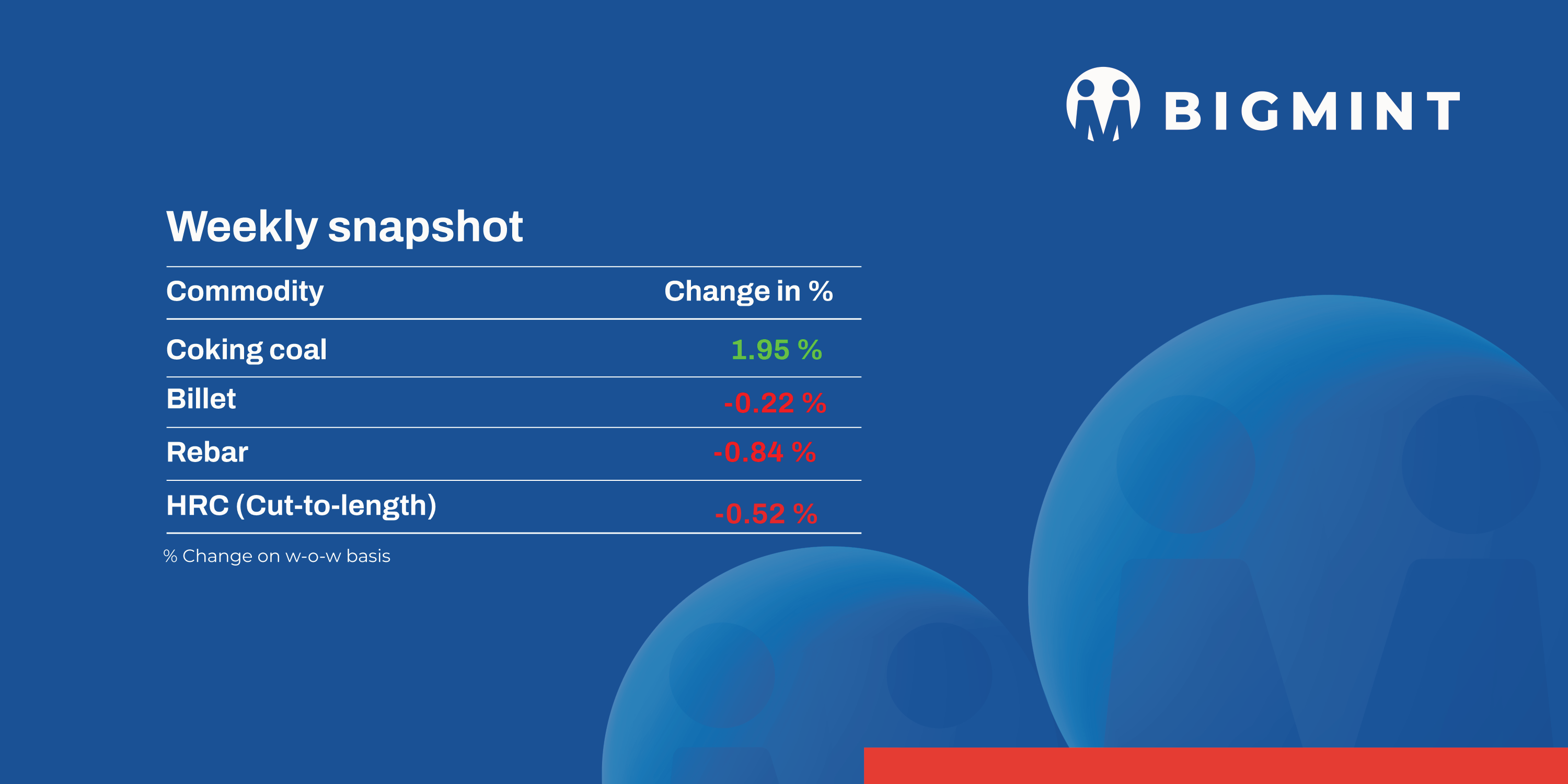

The domestic steel market saw seesaw trend in prices during week 19 ( 6-11 May, 2024). Semi-finished steel prices varied in the range of INR 100-1,400/tonne (t).

Iron ore, pellet

- BigMint’s bi-weekly domestic pellet (Fe 63%) index, PELLEX, inched down by INR 50/t w-o-w to INR 10,350/tonne (t) DAP Raipur on 9 May. Around 176,000 t deals were recorded in the Raipur region in the last one week. The buyers in Raipur are getting deals concluded from the nearer cities and Odisha region recently as they preferred to book outside region material to get decent steel margin in the last couple of days.

- SMIORE conducted an auction for 71,000 t of iron ore lumps (5-40mm, Fe 55-58.20%) from its Sandur mines, Karnataka on 9 May, 2024 in which 7,000 t of lumps (5-20 mm, Fe 55.6-56.1%) got booked at INR 4,700-5,010/t, 15,000 t of lumps (10-40 mm, Fe 58.2%) got booked at INR 5,120-5,140/t and 20,000 t of lumps (20-40 mm, Fe 56.52-57.75%) got booked at INR 5,100-5,470/t . Prices include royalty, DMF, and NMET.

- BigMint’s weekly Indian low-grade iron ore fines (Fe 57%) export index remained stable w-o-w at $66/t FOB east coast on 9 May 2024.Three deals of a total of 160,000 t were recently heard for standard Fe 57% fines at $65-67/t FOB east coast India also three cargo deals of Fe 54/55% at $65-66/t CFR China were recorded this week. The Indian sea market remained supportive this week following active deals at decent discount. Moreover, active buying interest for the lower-grade ore from China was noted post-holiday.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) remained stable w-o-w at $106/t on 8 May, 2024. The export market remained sluggish in the last one week following weak buying interest as Chinese participants were away for the week-long Labour Day holidays. However, markets resumed this week but no successful transaction was concluded from India amid lack of firm bids. A South India-based pellet producer floated an export tender for exports of 50,000 t of iron ore pellets (Fe 63%, 8% Al2O3+SiO2). The bid responses are expected to be declared on 9 May and are only for the company’s empanelled customers.

- Asia-Pacific Supramax dry bulk (50,000-55,000 t) freight rates for an iron ore vessel from the east coast of India to China rose by $0.5/tonne (t) w-o-w this week to $15.5/t on 8 May, as per BigMint’s assessment.

Coal

- Australian premium hard coking coal (PHCC) prices edged up by $3/t w-o-w to $243/t FOB and $261/ t CNF on 10 May, 2024 amid increased appetite from Chinese buyers on rising domestic coal prices.

- RB1 (6000 NAR) grade prices dropped by $1 w-o-w to $107/t FOB. However, RB3 remained stable w-o-w at $82/t FOB Richards Bay, South Africa.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port recorded at INR 8,400/t, stable w-o-w.

Ferro alloys

- Silico manganese: Silico manganese prices in India remained largely stable by with a slight decline by INR 600/t ($7/t) to INR 92,500-94,700/t ($1,107-1,134/t) exw across major markets of Raipur, Durgapur, and Vizag. This slight decline was noticed because less acceptance was there for high priced materials.

- Ferro manganese: Ferro manganese (HC70%) prices rose by INR 1,400/t ($17/t) w-o-w in Raipur, reaching INR 96,400/t ($1,154/t) exw, and while in Durgapur prices remained unchanged at INR 96,300/t ($1,153/t). Prices rose on limited supply and improved demand.

- Ferro silicon: Indian ferro silicon (FeSi:70%) prices rose by INR 1,350/t ($16/t), settling at INR 101,600/t ($1,216/t) exw-Guwahati on 10 May, up by INR 1,000/t ($12/t). Meanwhile, Bhutan prices were also up by INR 1,700/t ($20/t), reaching INR 101,400/t ($1,214/t) exw. Prices went up as demand saw an uptick, particularly in the global markets, which contributed to domestic price increases as well.

- Ferro chrome: Prices of Indian high-carbon ferro chrome (HC60%, Si:4%) inched down by INR 1,000/t ($12/t) on 10 May, settling at INR 106,900/t ($1,280/t) exw-Jajpur. Prices inched down as market sentiments have weakened post-FACOR’s auction.

Semi-finished

- In terms of price, India’s induction furnace route-finished long steel saw a mixed trend w-o-w. Spot trade activity was minimal due to the fluctuations in billet and sponge iron prices. Buyers opted wait and watch mode to procure material in bulk at upper price levels and such scenario compelled sellers to reduce the offers in order to escalate sales. As per the participants, prices are likely to remain range-bound in the near-term.

- On a weekly basis, in rebar steel prices showed a mixed response by INR 100-1,400/t across the regions except few locations were stable as per BigMint’s assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 47,000-47,400/t exw Raipur, INR 52,600-53,200/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 50,000-50,400/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 47,700-48,300/t ex Raipur.

Finished long steel

- IF Route: In terms of price, India’s induction furnace route finished long steel saw a mixed trend w-o-w. Spot trade activity was minimal due to the fluctuations in billet and sponge iron prices. Buyers opted wait-and-watch mode to procure material in bulk at upper price levels and such scenario compelled sellers to reduce the offers in order to escalate sales. As per the participants, prices are likely to remain range-bound in the near-term.

- On a weekly basis, in rebar steel, prices showed a mixed response by INR 100-1,400/t across the regions except few locations were stable as per BigMint’s assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 47,000-47,400/t exw Raipur, INR 52,600-53,200/t exw Jalna.

- Trade reference price of heavy structural steel for base size 150mm channel stands at INR 50,000-50,400/t exw Raipur.

- Trade reference prices of wire rod hovering at INR 47,700-48,300/t ex Raipur.

- BF-rebar: Trade-level BF rebar prices increased w-o-w by INR 400-1,200/t across markets as leading primary mill announced interim price hike of INR 500/t during the week, sources informed. Lower inventories and shortages in some sizes in the market have led to rise in price levels, while demand in the trade channel remained slow.

- Current week’s rebar prices (12-32mm, Fe500D) in the trade segment increased by INR 1,000/t w-o-w to INR 58,800/t exy-Mumbai. Prices are exclusive of GST at 18%. In the projects segment, prices were hovering around INR 57,500-58,000/t FOR Mumbai.

Finished flat steel

- The tier-I steel mills announced an increase in their list prices of hot-rolled coil (HRC), HR-Plates and, cold-rolled coils (CRC) by up to INR 1,500/tonne (t) for May 2024 sales.

- The effective list price levels for May 2024 sales are as below for public and private mills:

- HRC (IS2062, Gr- E250 BR, 2.5-8mm)- INR 54,500-55,000/t exy-Mumbai

- CRC (IS513, Gr-O/1, 0.9mm)- INR 59,800-61,500/t exy-Mumbai basis

- Coil-to-coil prices, INR 750/t extra for cut to length (CTL). Excludes GST at 18%.

- BigMint’s benchmark evaluation (bi-weekly) for HRC (2.5-8mm, IS2062, Gr E-250 Br) notched up to INR 54,500/t exy-Mumbai as on 10 May 2024. This is higher by INR 300/t against the previous assessment on 3 May 2024. Taking note of the same period, CRC prices increased by INR 100/t to INR 61,300/t exy-Mumbai. These prices mentioned above exclude GST at 18%, and are for cut-to-length (CTL) form.

- Despite a price increase in the traders’ market, actual buying activity transpired at lower levels. This coincides with reports of strained raw material supply and subdued demand in certain markets.

- The import of Bulk HRC (Hot Rolled Coil) and plates surged to 4,22,132 t in April 2024, compared to 3,81,794 t in March 2024 and 4,65,276 t in February 2024. This uptick in imports may exert downward pressure on domestic prices.

- In May 2024, three major private mills are thinking about taking one HSM each for a maintenance run. The production loss in May is expected to be around 310,000 t. Moreover, one of the mills’ tenure shall extend till late June resulting in a loss of another 180,000 t, shared some reliable industry participants.

- Indian HRC export offers for Southeast Asia and the Middle East (ME) continued to remain on hold for yet another week. Mills are currently prioritising the domestic market, where offers have been further increased by INR 1,500/tonne (t) for May deliveries.

- Indian steel mills continued to hold their HRC export offers (S275, 3mm) to Europe this week as well. However, mills are expected to start offering this week for June-July 2024 shipments, hinted market sources.