The domestic steel market witnessed a mixed trend during week 4 ( 23 – 28 January, 2023). Semi-finished prices fluctuated in the range of INR 50-500/tonne (t).

Domestic induction furnace-route finished long steel offers witnessed a seesaw trend, as offers varied by INR 100-1,600/t w-o-w. The trade reference prices for HRCs and CRCs increased by a wide range of INR 300-2,200/t accross regions.

Iron ore and pellets

- SteelMint’s bi-weekly domestic pellets (Fe 63%) index, PELLEX, stood at INR 10,250/t, stable compared to the last assessment on 24 January, 2023. No deals were reported in the current publishing window. The market was mostly silent and participants were looking for more clarity.

- India’s largest merchant iron ore mining company, NMDC, increased list prices of iron ore recently. The company raised prices of lump ores by up to INR 300/t and fines by INR 500/t, effective from 28 January. NMDC fixed prices for lump iron ore (65.5%) at INR 4,800/t, DR CLO (Fe 67%, 10-40mm) at INR 5,820/t and iron fines (64% – 10mm) at INR 3,910/t (FoR prices from Bacheli complex, excluding royalty, DMF and NMET).

- India’s pellet export trades remained stable compared to last week. SteelMint’s India pellet (Fe 63%, 3% Al) export index FOB east coast was assessed at $118/t, stable w-o-w. Prices increased slightly last week on restocking needs ahead of the Lunar New Year holidays.

- Goa is notifying 5 leases on the back of a successful auction in December where premiums crossed the 100% mark. The five new mines include three that will not need fresh environment and forest clearances or mining plans and can operate with the earlier limits. The last date for the purchase of tender document is 17 March, 2023 and last date for bid submission is 27 March, 2023.

- Vedanta conducted an auction for 28,000 t of iron ore lumps (Fe57.5%, 6-20 mm) from its A. Narrain mines in Karnataka on 24 January, 2023. According to sources, the entire quantity was booked at INR 4,126/t. The floor price was set at INR 3,696/t (excluding royalty, DMF, and NMET).

Coal

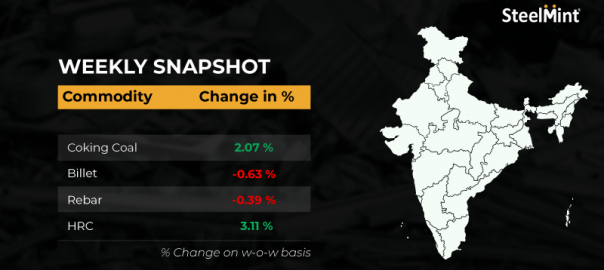

- Australian hard coking coal prices increased by $7/t in a week’s time to $332/t FOB and $345/t CNF India. The rise came amid supply tightness for February-March cargoes due to rains and improved demand from the Southeast Asia market.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port remained range-bound w-o-w at around INR 11,500/t ex-port.

- RB1 (6000 NAR) grade prices have come down by $13/t to $158/t FoB. The prices came down amid slowed demand from Europe and India.

Ferrous scrap

- Indian steel industry players were mostly quiet this week, with limited quantity deals heard from Middle East-originated suppliers. Steel producers are waiting for the upcoming Budget 2023-24, which is scheduled on 1 February. Interestingly, market players kept their eyes on global market activities, as prices moved up in recently-concluded deals from Turkish buyers.

- However, suppliers are cautious and try to sell their material at increased prices to Turkish and Indian buyers, in the absence of scrap buyers from Pakistan and Bangladesh. Prices remain high due to low scrap generation and material scarcity.

- SteelMint’s assessment for UK-origin shredded is at $455/t CFR, down by $5/t w-o-w.

Ferro alloys

- As on 27 January 2023, Indian silico manganese prices fell by 2% w-o-w to INR 77,000 exw-Durgapur and INR 77,000/t exw-Raipur. Prices dropped as a result of diminishing domestic demand, growing liquidity problems, and a bearish foreign market.

- On a weekly basis, Indian ferro manganese prices dipped by 1% w-o-w to around INR 78,600/t exw-Durgapur and INR 79,300/t exw-Raipur, as assessed on 27January 2023. The price of ferro manganese was slightly lowered as a result of the constrained demand for special steel and the mismatch between supply and demand.

- According to SteelMint’s assessment on 25 January, ferro chrome prices were hovering at around INR 111,100/exw-Jajpur. Domestic buyers remained muted as they were waiting for purchase tender price announcement by major Chinese stainless steel giants.

- Indian ferro silicon prices remained range-bound owing to moderate demand. According to SteelMint’s assessment on 27 January, ferro silicon prices were at around INR 124,000-125,000/t exw-Guwahati.

Semi-finished

- Semis trades slowed down this week as domestic billet prices decreased by INR 100-500/t in all locations except Jalna and Mumbai which increased by INR 100-200/t. While sponge prices showed mixed trends with prices falling by INR 100-400/t in several locations, and rising by INR 50-300/t in northern and central regions.

- SAIL-Bhilai Steel Plant (BSP) held an auction for 5,000 t of steel grade pig iron on 21 January. The entire quantity was booked at an average price of INR 43,550/t exw, sources informed.

- Vedanta’s Goa plant has received the consent for expansion of its blast furnace capacity by 0.16 mnt/year. After expansion, its total pig iron capacity will increase to 1 mnt/year.

Finished longs

- India’s induction furnace-route finished long steel market witnessed a slight price correction this week. Weak demand at higher offers as well as a price drop in semi-finished steel across various regions were the major factors that prompted manufacturers to decrease offers. Despite the decline in prices, limited trades were observed in the spot market. Traders are currently procuring rebar, structure and wire rods as per need to avoid piling up inventory due to uncertainty in market directions.

- On a weekly basis, rebar showed mixed trends — decline of INR 100-800/t in some markets while others remained stable and showed a marginal increase of INR 100-400/t except in the Mumbai market where a sharp hike of INR 1,600/t was registered, as per SteelMint assessment.

- The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 51,500-51,900/t exw-Raipur, and at INR 57,100-57,600/t exw-Jalna.

- Trade discounts given by Raipur-based heavy structural steel manufacturers were at around INR 2,000-2,500/t and trade reference prices of 200 mm angles stood at INR 57,300-57,700/t exw-Raipur.

- In Raipur, trade discounts in wire rods, given by traders, were at around INR 500-700/t and trade reference prices stood at INR 51,000-51,500/t exw-Raipur and INR 51,300-51,700/t exw-Durgapur, for size 5.5 mm.

- Trade level prices of BF-route rebars rose w-o-w across all markets following hike in list prices by up to INR 1,000/t by primary mills. Increase in raw material prices like iron ore, coking coal and IF-route rebars have supported the trade level prices of BF-route rebars. Furthermore, mills are likely to announce hike in prices for February sales in the coming days.

- SteelMint’s weekly price assessment for rebars (12-32 mm, BF-route, IS 1786, Fe500D) increased by INR 1,100/t w-o-w to INR 62,000/t, exy-Mumbai, excluding GST at 18%.

Finished flats

- Trade reference prices of flat steel products have continued their rally this week. Major mills announced another hike in their flat steel list prices earlier this week. Increasing raw material costs and decent export bookings remain the reasons behind the increase in prices by mills. Coated flat steel prices have hit an eight-month high mark, hovering close to the levels last seen in June 2022.

- In the aftermath of the export duty removal, Indian mills have been enjoying more opportunities for exports along with rising global export offers. Major end-user industries like automobile, white goods, infrastructure and construction will continue to pose demand amid improvement in activities and will keep prices buoyed in the near term, highlighted a source.

- On the exports front, SteelMint’s HRC (SAE1006) export index increased steeply by $47/t w-o-w at $680/t FOB east coast this week. Global market sentiments remain improved, especially in the Middle East and European markets. Furthermore, participants opine that the Chinese mills will come up with higher export offers post-Lunar New Year holidays.

Leave a Reply