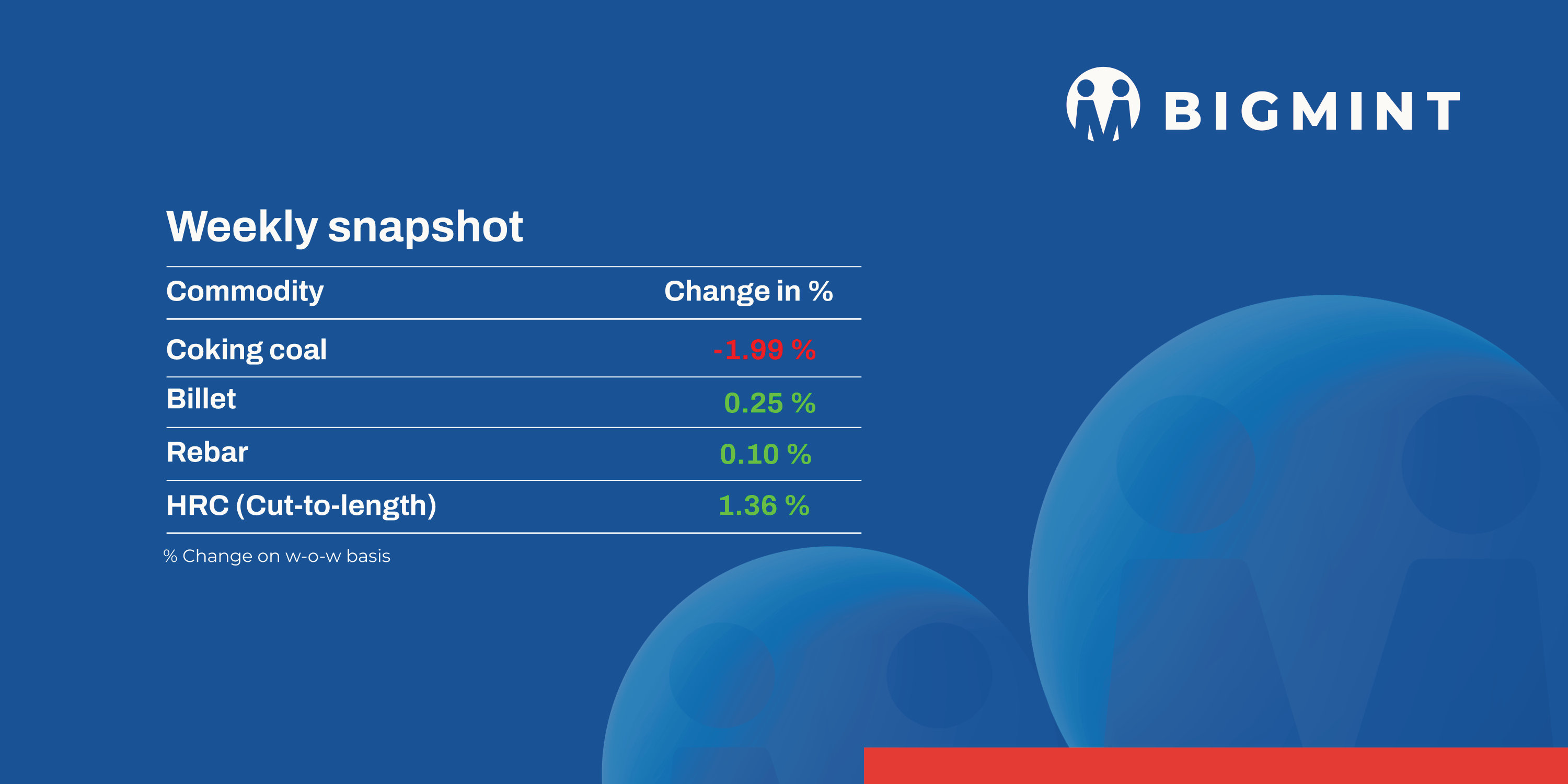

Indian semi-finished steel prices showed an uptrend this week. Domestic billet prices in almost all key locations increased by INR 100-800/t. Induction furnace-made finished long steel prices rose in the domestic market, propped up by billets and supported by tier-1 mills’ price hikes, strengthening the positive trend seen of late in the secondary market.

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe63%) index remained stable w-o-w at INR 9,850/t ($113/t) DAP Raipur on 7 March. Trading activity improved this week as Raipur buyers booked around 91,000 t of raw pellets this week. Raipur sellers kept the offers same while prices in the Odisha region slightly increased.

- BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) decreased by $6/tonne (t) w-o-w to $96/t on 5 March. Indian pellet export prices dropped by $6-7/t over the past week due to weak market sentiment and poor macro-economic indicators from China. The decline in global fines indices further pressured pellet prices in the overseas market.

- Accordingly, BigMint’s pellet export index also dropped w-o-w, to its lowest level in over a month, last seen in mid-January 2025.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index declined by $4.5/t w-o-w to $62/t FOB east coast, India, on 6 March. Odisha-based traders sold around 110,000 t of iron ore fines (Fe 57%) at $73-75/t CFR China last weekend.

- Sharp fluctuations in global prices led to fewer inquiries, with exporters awaiting price clarity before making further deals.

Coal

- Portside South African thermal coal prices ease: RB2 (5500 NAR) fell by INR 50/t to INR 8,450/t exw-Gangavaram, while RB3 (4800 NAR) remained steady at INR 7,100/t as buyers shifted preference to domestic coal, leading to further price corrections.

- India’s domestic met coke prices show mixed trends: BF-grade coke remained stable at INR 34,500/t exw-Jajpur, while Gandhidham prices increased by INR 400/t to INR 32,400/t due to lower imports and limited port inventories.

- Thermal coal inventories at Indian ports experienced a slight decline of 1%, dropping to 12.09 million tonnes (mnt) in week 9 of CY’25, compared to 13.04 mnt in the previous week, according to data from BigMint.

Ferrous scrap

- India’s imported scrap market remained sluggish throughout the week due to weak demand, tight liquidity, and a widening bid-offer gap. UK/European shredded offers stood at $375-380/t CFR Nhava Sheva, but bids remained lower at $365-370/t CFR, leading to limited deals. HMS (80:20) offers ranged between $350-355/t CFR, with buyers countering at $340-345/t CFR. No firm US-origin offers emerged due to high freight costs and unworkable price levels.

- Despite improved finished steel sales and rising Turkish scrap prices, Indian buyers resisted higher offers, citing sufficient domestic scrap availability and currency depreciation concerns. Traders reported that UK/EU-origin shredded and HMS remained unviable due to high landed costs, keeping trading activity slow. Additionally, the approach of Holi and the fiscal year-end further contributed to muted market sentiment, with minimal fresh import activity.

- Approximately 5,000-5,500 t of scrap were booked, including 2,500-3,000 t of HMS (80:20) from the UK, Chile, New Guinea, Europe, and South Africa at $352-362/t. Additionally, 5,00-1,000 t of shredded scrap from Australia traded at $375/t, and 2,50-5,00 t of PNS from the UAE at $380/t.

Ferro alloys

- Silico manganese: Indian silico manganese prices were slightly down w-o-w by INR 250/t ($3/t) w-o-w to INR 72,500-73,600/t ($829-841/t) in key regions of Durgapur, Raipur and Vizag. The slight correction in prices can be seen because of the resumption in productions and market discounts.

- However, MOIL has raised its ore offers for March 2025 by 10% for Mn>44% and by 6.5% for Mn<44%.

- Ferro manganese: Indian ferro manganese (HC 70%) prices inched down w-o-w to INR 75,700/t ($869/t) exw in Durgapur. Meanwhile, prices exw-Raipur also dropped by INR 400/t ($5/t) to INR 75,600/t ($867/t). Prices edged down due to buyers’ reluctance towards higher offers.

- Ferro silicon: Indian ferro silicon prices inched down by INR 900/t ($10/t) w-o-w to INR 99,600/t ($1,143/t) exw-Guwahati. Prices also dropped by INR 700/t ($8/t) in Bhutan to INR 99,800/t ($1,145/t) exw. Prices edged down as sellers aligned their offers with Bhutan’s March prices of INR 100,000/t ($1,147/t) exw.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices edged up INR 900/t ($10/t) w-o-w to INR 101,600/t ($1,166/t) exw-Jajpur. Prices were stable, as not much variation was seen in bids and offers, and the market witnessed regular trades.

- Additionally, at Vedanta-FACOR’s ferro chrome auction yesterday, the larger lot of 10-150 mm fetched an H1 price of INR 100,000/t exw, same as the base price. A slight hike of INR 250/t was seen from the previous auction on 24 February.

Semi-finished

- Indian semi-finished steel prices showed an uptrend as per BigMint’s assessment. Domestic billet prices in almost all key locations increased by INR 100-800/t, with a major increase of INR 800/t seen in the Hindupur market. However, sponge iron prices also moved up in most key locations by INR 100-550/t, with a major increase of INR 550/t seen in the Durgapur market.

- Indian DRI export offers decreased by $9/t, CPT Raxaul to $341/t while CPT Benapole offers decreased by $5/t to $340/t.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, conducted a steel-grade pig iron auction for 10,000 t on 3 March. About 2,500 t received bids at the base price of INR 34,500/t. In the previous approved auction, held on 31 January, out of 12,000 t, around 4,000t got booked at an average price of INR 30,500/t.

- Evonith held an auction on 5 March for 5,000 t of steel-grade pig iron. The entire volume on offer was booked at an average price of INR 35,700/t exw. Previously, on 3 March, Evonith auctioned 6,000 t of steel-grade pig iron, with the entire quantity sold at an average price of INR 35,350/t exw.

Finished long steel

- IF-rebar: India’s induction furnace-route finished long steel market gained momentum in terms of trade in the spot market. Active trading activities were observed. Buyers procured sufficient quantities, and the smooth lifting of previously-booked material kept market movement steady.

- Sellers reported reduced inventory pressure and continued to receive new bookings, reflecting healthy demand in market. However, buyers resisted higher offers. Additionally, the upcoming Holi festival may lead to labour shortages and logistical challenges, potentially prompting manufacturers to raise prices.

- On a weekly basis, rebar prices fluctuated in the range of INR 100-600/t across regions, as per BigMint’s assessment.

- The trade reference price of Fe 500 grade rebar, 10-25 mm, manufactured via the IF route, was assessed at INR 43,500-43,900/t exw-Raipur, and at INR 48,400-49,000/t exw-Jalna.

- Trade reference prices of heavy structural steel channels of base size 150mm stood at INR 44,800-45,300/t exw-Raipur.

- Trade reference prices of wire rods hovered at INR 44,200-44,700/t ex-Raipur.

- BF-rebar: Indian tier-1 mills have increased rebar list prices by up to INR 2,000/t for early-March 2025. Post-revision, list prices hovered at around INR 53,000-54,000/t on a landed basis. Following this, trade-level BF-rebar prices witnessed an increase w-o-w across markets. In addition, limited material availability across sizes of rebars in the trade segment lent support to prices.

- Current week’s rebar prices (12-32mm) in the trade segment rose by INR 1,100/t w-o-w to INR 54,300/t exy-Mumbai. Prices are exclusive of GST at 18%.

- In the projects segment, prices rose w-o-w to around INR 52,500-53,500/t FOR Mumbai basis.

Flat steel

- Leading Indian steel manufacturers have officially raised list prices of hot-rolled coils (HRCs) and cold-rolled coils (CRCs) by INR 1,100-1,500/t ($6-18/t) for March 2025 sales. Additionally, some new market entrants have announced a price increase of INR 1,100-1,400/t ($6-18/t) for the same products. While multiple mills have confirmed this price hike, official announcements from a few others are still pending.

- Trade-level hot-rolled coil (HRC) prices across India increased by up to INR 1,600/tonne (t) w-o-w to INR 48,100-50,500/t. Additionally, cold-rolled coil (CRC) prices rose by up to INR 1,000/t w-o-w, settling at INR 54,200-58,300/t ($617-671/t) across markets. The price hike was driven primarily by material shortages and speculation regarding the imminent imposition of a safeguard duty.

- India’s bulk imports of HRCs and plates touched 413,020 t in February 2025, according to vessel line-up data from BigMint. As of 3 March, imports stood at 59,358 t this month, with an additional 81,604 t expected to arrive later.

- BigMint’s India HRC (SAE 1006) export index for the Middle East and Vietnam declined by $10/t w-o-w to $495/t FOB east coast India, compared to $505/t last week. Recent export deals to the Middle East indicate a slight improvement in demand in the region. Meanwhile, European demand was subdued due to weak market sentiment and ongoing anti-dumping investigations.

Leave a Reply