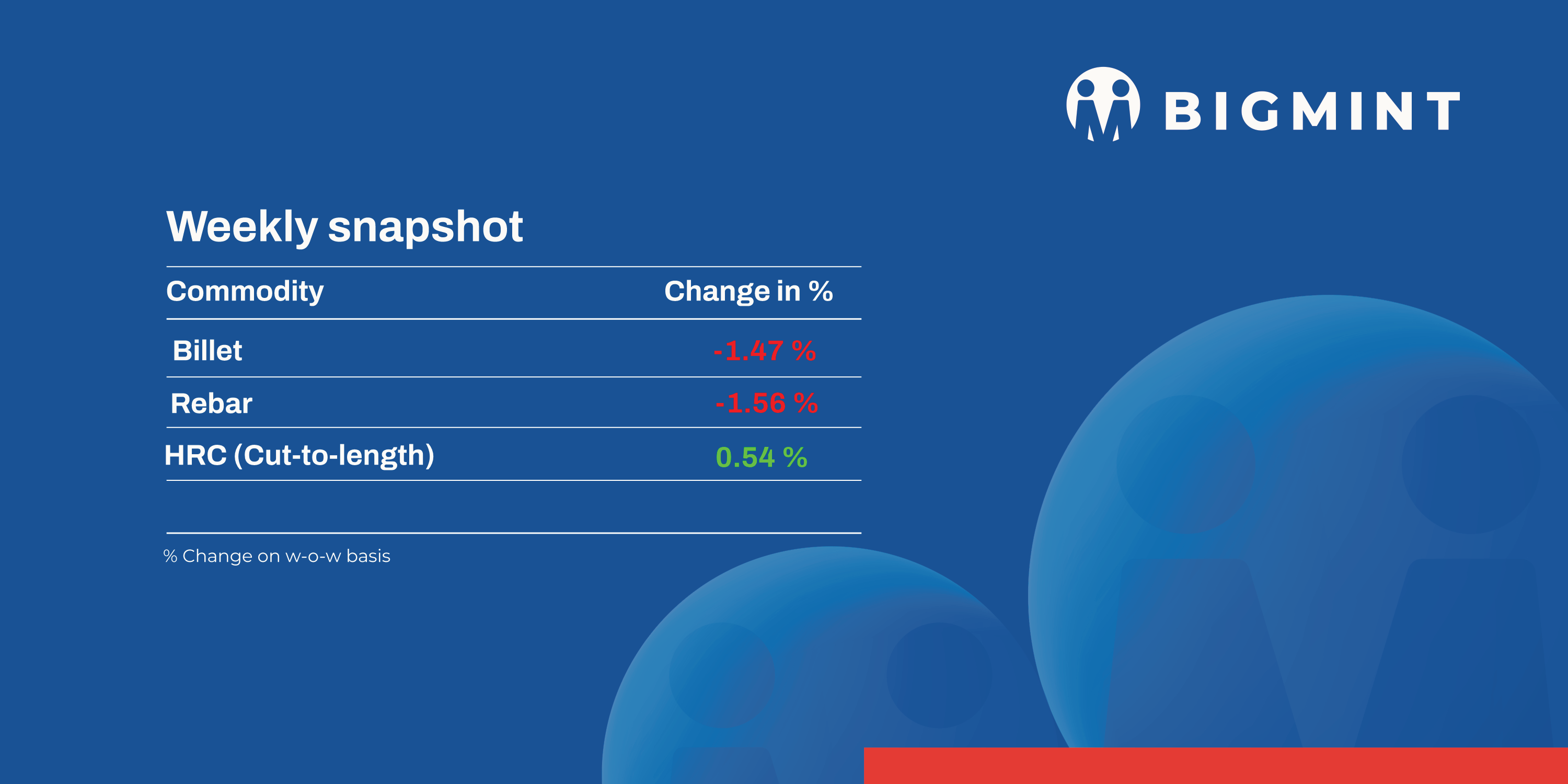

- Billet fall by 200-1,100/t across key locations

- Trade-level HRCs up by INR 1,300/t w-o-w

India’s domestic steel market witnessed a downwards trend in prices during week 18 ( 28 Apr-03 May, 2025). Semi-finished steel prices fell further in the range of INR 200-1,100/tonne (t).

Iron ore and pellet

- BigMint’s bi-weekly domestic pellet (Fe63%) index dropped by INR 150/t ($2/t) w-o-w to INR 9,800/tonne (t) ($116/t) DAP Raipur on 2 May. Raipur-based pellet producers reduced their offers for Fe63% (+/- 0.5%) material by INR 300/t ($4/t) to INR 9,600-9,700/t ($114-115/t) exw on 30 April.

- NMDC Chhattisgarh fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 7,210/t ($85/t) and of iron ore fines (-10 mm, Fe 64%) at INR 5,500/t ($65/t), an increase of INR 140/t ($2/t) and INR 440/t ($5/t), respectively on 1 May. Prices are on FOR basis from its Bacheli complex and include royalty, DMF and NMET.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index inched down by $0.5/t w-o-w to $60/t FOB east coast, India, on 1 May. Trade activity in the Indian Ocean remained thin, but a few exporters received inquiries and concluded deals ahead of market closing. Despite the weak sentiment, a few Indian miners and traders closed small deals totalling around 325,000 t of Fe50-57% material.

Coal

- South African RB2 prices dropped to INR 8,350/t at Gangavaram, with inventories rising 7.4% to 13.29 million tonnes (mnt). Despite moderate arrivals, weak demand from Indian buyers and cautious sentiment reflect concerns over the current market stagnation, with limited buying interest due to declining sponge iron prices.

- Domestic coal prices held steady at INR 4,500/t for 4500 GCV and INR 4,950/t for 5000 GCV. SECL auctions saw only 10-20% of coal sold, signalling weak demand. With most buyers holding sufficient stock, market sentiment remained cautious, expecting little change unless demand significantly shifts.

- BigMint’s premium hard coking coal index rose $3/t to $206/t CNF Paradip, with recent deals at $205-209/t CFR India. Despite the rise, market sentiment remained cautious, with mixed expectations in price movements. Some buyers predict a decline due to fluctuating market conditions and supply uncertainties.

- Imported US pet coke dropped to $106/t CFR east coast India. Nayara and MRPL reduced prices by INR 1,070/t and INR 1,240/t, respectively. The sentiment remains bearish with subdued demand, reflecting cautious market behaviour as refiners and traders adjust to lower consumption and weak buying interest.

- India’s met coke prices weakened in eastern markets due to falling pig iron prices and muted demand. Prices in Jajpur dropped by INR 450/t to INR 33,650/t exw, while Gandhidham remained steady at INR 32,200/t. Weaker steel output and higher scrap usage weighed on buying interest, keeping sentiment under pressure.

Ferrous scrap

- India’s imported ferrous scrap market remained stable this week, with UK-origin shredded steady at $370/t CFR Nhava Sheva, nearly unchanged from last week’s $371/t. Buyers stayed cautious amid falling Turkish prices, seasonal slowdown, and weak domestic steel demand. Shredded bids held at $365/t reflecting a consistent gap between buyer and seller expectations, keeping trade limited. HMS 80:20 offers from the UK, West Africa, and South Africa ranged between $345-360/t CFR, but high freight and full inventories further suppressed buying interest.

- Pre-monsoon hesitation and tight liquidity dampened trade. UK suppliers kept shredded offers firm, dockside supply tight and collection costs above EUR 230/t FOB, but Indian buyers were hesitant. Buyers focused on short-haul or on-water cargoes, waiting for clearer price direction before committing.

- Around 22,000-23,000 t of imported scrap were booked in India this week. This included 6,000-7,000 t of HMS 80:20 at $347-365/t CFR and 2,000-3,000 t of shredded scrap priced at around $365/t CFR. The balance comprised HMS 1, LMS bundles, and approximately 11,000 t of busheling scrap, which traded at $385/t CFR.

Ferro alloys

- Silico manganese: Indian silico manganese prices remained largely steady with a slight decline of INR 225/t ($3/t) w-o-w to INR 70,250-70,700/t ($831-834/t) in the key regions of Durgapur, Raipur and Vizag. Steel mills, with sufficient inventories, have adopted a cautious approach to procurement. This has put pressure on smelters to offer competitive prices to secure deals.

- Ferro manganese: Indian ferro manganese (HC 70%) prices fell by INR 700/t ($8/t) w-o-w to INR 73,000/t ($863/t) exw in Durgapur. Meanwhile, prices, exw-Raipur decreased by INR 800/t ($9/t) to INR 73,200/t ($865/t). Prices fell amid soft demand in the downstream market.

- Ferro silicon: Indian ferro silicon prices were largely steady with a slight rise of INR 300/t ($4/t) w-o-w to INR 95,300/t ($1,127/t) exw-Guwahati. However, prices in Bhutan dipped by INR 300/t ($4/t) to INR 95,500/t ($1,129/t) exw. Limited market activity was observed, as most sellers were sold out for the month. Additionally, Bhutan announced its prices at INR 95,500/t ($1,129/t) for May 2o25.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices held steady with a slight decline of INR 100/t ($1/t) w-o-w to INR 100,400/t ($1,187/t) exw-Jajpur. The slight drop in prices can be attributed to the decline in bids at Vedanta-FACOR’s ferro chrome auction, which concluded at INR 99,500/t ($1,175/t) exw for the bigger lot of 10-150 mm.

Semi-finished

- Indian semi-finished steel prices showed negative trends as per BigMint’s assessment. Domestic billet prices in almost all key locations decreased by INR 200-1,100/t across regions with a major decrease of INR 1,100/t seen in Hindupur. However, sponge iron prices showed a downtrend in almost all key locations, moving down by INR 100-1,100/t, with a major decrease of INR 1,100/t seen in the Raipur market.

- Indian DRI export offers decreased by $8/t CPT Raxaul, to $347/t while CPT Benapole offers decreased by $10/t to $350/t.

Finished longs

- IF-rebar:India’s induction furnace route finished long rebar prices declined on a w-o-w basis. Trading activity remained slow across most regions, with buyers procuring only as per immediate requirements. In response, manufacturers reduced trade offers to boost sales. However, buyers-particularly retailers-remained hesitant to place bulk orders, preferring to wait for clearer price direction amid ongoing uncertainty. Overall, market participants anticipate prices to remain range-bound in the near term.

- On a weekly basis, in rebar steel prices decreased in the range of INR 300-1,000/t across the regions as per BigMint assessment shows. The trade reference price of Fe 500 grade rebar manufactured via the IF route for 10-25 mm size was assessed at INR 44,100-44,500/t exw Raipur, INR 48,500-49,000/t exw Jalna.

-

Trade reference price of heavy structural steel for base size 150mm channel stands at INR 45,600-45,900t exw Raipur.

-

Trade reference prices of wire rod hovering at INR 44,500-45,000/t ex Raipur.

- BF-rebar: Trade-level blast furnace (BF) rebar prices in key domestic markets remained largely range-bound over the week, as demand in the spot market continued to be need-based. Market participants adopted a cautious approach, opting to wait for clarity on mill pricing for May 2025.

- Trade-level BF rebar prices edged down by INR 100/t w-o-w to INR 56,800/t exy-Mumbai, as per BigMint’s assessment on 2 May 2025. Prices are exclusive of GST at 18%.

- In the projects segment, prices hovered at around INR 55,500-56,500/t FOR Mumbai.

Finished flats

- Trade-level prices of hot-rolled coil (HRC) rose by up to INR 1,300/t ($6/t) w-o-w to INR 51,500-53,800/t ($603-616/t) across markets. Cold-rolled coil (CRC) prices also increased by up to INR 1,100/t ($9/t) w-o-w to INR 59,600-60,300/t ($661-702/t).

- Participants are taking a cautious approach, opting to undertake a need-based buying approach. The market is abuzz with speculation of hike in list prices by the mill to the tune of INR 1,500-2,000/t.

- India’s bulk imports of HRCs and plates touched 2,83,840 t as of 28 April, based on vessel line-up data from BigMint. Another 94,919 t are expected to arrive next month.

- Indian mills have reduced their HRC (S275) FOB offers for EU shipments from key Indian ports, which are currently quoted at $585-590/t. According to sources, the ongoing weakness in exports is primarily due to the unfavourable euro-dollar parity. Trade activity in the EU remains subdued as buyers adopt a cautious stance. Meanwhile, Indian mills are refraining from active offers to the Middle East market due to aggressive Chinese pricing and better domestic realisations. W-o-w, Indian HRC export offers to the EU have dropped by $10/t to $635-640/t CFR Antwerp ($585-590/t FOB east coast India), compared to last week’s $645-650/t CFR.

Leave a Reply