The domestic steel market saw uptrend in prices during week 7 ( 13 February-18 February, 2023). Semi-finished steel prices increased in the range of INR 700-2,250/tonne (t).

Domestic induction furnace-finished long steel offers witnessed an upward price trend while offers raised by up to INR 300-2,400/t w-o-w. The trade reference prices for HRC and CRC declined in the range of INR 400-1,500/t across region.

Iron ore and pellets

- SteelMint’s bi-weekly domestic pellets (Fe 63%) index, PELLEX, stood at INR 10,100/tonne (t) DAP Raipur, increased by INR 150/t compared to the last assessment on 14 February, 2023. Around 25,000 t of deals were reported in this publishing window. Trade volumes improved this week in comparison to the previous week – which was rather subdued.

- National Mineral Development Corporation (NMDC) conducted an auction for 222,600 t of iron ore from its Bacheli mines in Chhattisgarh on 17 February, 2023. 21,000 t of DRCLO (10-40mm, Fe67%) were booked at INR 5,864-5,874/t and 105,000 t of Bacheli fines (Fe64%) were booked at INR 3,960-3,970/t. However, ROM remained unsold. All prices exclude royalty, DMF, and NMET charges.

- Odisha Mining Corporation’s (OMC’s) conducted an iron ore auction on 16 February, 2023. Out of 574,000 t of fines put up for auction, only 5,59,000 t or 97% of the total quantity received bids. The bid price for fines increased by up to INR 1,100/t against the last auction on 17 January, 2023. The company has raised bid prices by up to INR 1,100/t over base prices.

- Vedanta conducted an auction for the sale of 16,000 t of iron ore lumps (Fe57%) from its A. Narrain mines in Karnataka’s Chitradurga district on 15 February, 2023. According to sources, the entire quantity was booked at the floor price of INR 3,726/t. The price was exclusive of royalties, DMF, and NMET charges.

- SteelMint’s India pellet (Fe 63%, 3% Al) export index FOB east coast was recorded at $118/t, stable w-o-w due to weak demand for pellets this week. The index also remained stable on the overall downtrend seen in the market. According to market sources, the stability in iron ore prices globally and limited buying interest kept the Indian pellet export trade muted.

Coal

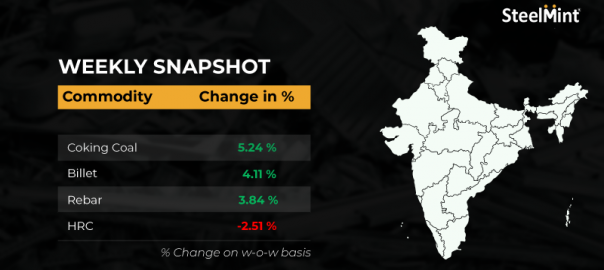

- Australian premium hard coking coal prices rose by $20/t w-o-w to $390/t FOB and $402/t CNF on 18 February, 2023. Prices rose amid supply tightness caused by disruption in supplies. In addition, there was strong interest to buy.

- Portside prices of South African RB3 (4800 NAR) thermal coal at Vizag Port recorded a fall to INR 10,600/t, down by INR 500/t w-o-w ex-port.

- RB1 (6000 NAR) grade prices have been majorly stable at $143/t FoB and RB3 prices flat at $95-96/t FOB.

Ferrous Scrap

- Indian participants are on a wait-and-watch mode. In fact, Indian ferrous scrap prices remained downwards with lesser enquires from the buyer side, as market participants assumed uncertainty for the time being and dynamics are not clear for further decisions of bigger volume bookings.

- Prior bulk consignments are being received at several ports in the country. The container market in India saw almost dull activities but some mini mills booked minimal volume for their prompt requirement to fulfill the target before the closing of FY22.

- SteelMint’s assessment for imported shredded scrap in containers is at $455/t CFR, down $10-14/t w-o-w.

Ferro Alloys

- As on 17 February 2023, Indian silico manganese prices inched down 1% w-o-w to INR 77,000 exw Durgapur and INR 76,500/t exw Raipur. Lack of demand both domestically and internationally caused prices of silico manganese to drop.

- Indian ferro manganese prices remained nearly stable w-o-w to around INR 80,500/t exw Durgapur and INR 79,700/t exw Raipur. Ferromanganese prices remained steady as a result of moderate demand and fluctuating raw material costs.

- Due to strong export demand and supply disruptions in major producing countries such as South Africa and Turkey, India’s ferro chrome (HC60%) prices increased by INR 3,650/t w-o-w to around INR 125,100/t exw Jajpur. Furthermore, high chrome ore prices due to high demand and limited supply also supported prices.

- According to SteelMint’s assessment on 17 February, a Guwahati-based producer was offering ferro silicon (70%) at around INR 125,500/t exw with marginal fluctuation for three consecutive weeks. Bhutan’s offers remained firm at INR 126,000/t, remained unchanged w-o-w due to a slower-than-expected recovery in demand.

Semi finished

- Indian semi-finished steel prices increased as per SteelMint’s assessment. On top of that domestic billet prices increased by INR 1,000-2,250/t across region with a major increase of INR 2,250/t seen in Mumbai. Similarly, sponge iron prices also increased by INR 700-1,850/t w-o-w.

- Vizag Steel has floated an ocean sale export tender for 30,000 t of steel blooms (150x150mm, 3SP/4SP) on FOB ST delivery against 100% advance payment terms. The last date of bid submission is 22 February, 2023. The delivery is scheduled for 15 April, 2023.

- SAIL-BSP conducted an auction for 10,100 t of full-length commercial rails (60 kg and 52 kg) on 17 February, 2023. About 6,500 t of 60 kg rails were sold at INR 41,500/t ex-works while 100 t of 52 kg rails received bids at INR 72,000/t ex-works.

- Rourkela Steel Plant (RSP) held an auction for 2,500 t of steel grade pig iron on 17 February, 2023. The entire quantity was booked in the range of INR 41,400-41,500/t exw.

Finished Long

India’s induction furnace-route finished long steel market witnessed an uptick in prices w-o-w as demand improved across all the regions. Prices were earlier on the lower side due to limited buying before mid-week. But after that, sales escalated quickly as bulk purchasing was observed in the market from the distributors’ end. Mills also reported smooth lifting of materials along with sufficient bookings.

- Rebar steel prices rose by up to INR 300-2,400/t across the regions, SteelMint’s assessment showed. The trade reference price of Fe 500 grade rebar manufactured via the IF-route for 10-25 mm size was assessed at INR 51,200-51,600/t exw Raipur, INR 55,800-56,300/t exw Jalna.

- Trade discount given by Raipur-based heavy structural steel manufacturers is over INR 2,000/t and trade reference price of 200 mm angles stood at INR 57,100-57,600/t exw Raipur. Trade discounts in Raipur wire rod given by suppliers is over INR 1,000/t and trade reference price at INR 51,200-51,700/t exw Raipur and INR 51,300-51,700/t exw Durgapur, size 5.5 mm.

- This week trade levels prices of BF-route rebars dropped w-o-w across major markets owing to slow demand. As a result, market participants in the distribution channel network started to offload their inventories which they have stocked in January.

- SteelMint’s weekly price assessment for rebars (12-32 mm, BF-route, IS 1786, Fe500D) dropped by INR 400/t w-o-w to INR 62,800/t, exy-Mumbai, excluding GST at 18%.

Finished Flat

- Trade level prices of finished flat steel products remained mostly under pressure this week barring bare galvalume coils (BGL) that increased towards the weekend. Slow demand in the traders’ market and some sellers aggressively liquidating their old inventories led to a decline in HRC and CRC prices for the second consecutive week.

- However, towards the weekend, some major mills started informing their distributors about a possible hike in flat steel product prices for March sales. This is a result of the elevated prices of raw materials such as iron ore and coking coal and coating materials such as zinc and aluminium. Thus, it is expected that the trade level prices should start rising in upcoming weeks, shared a major distributor from the north.

- On the exports’ front, SteelMint’s India HRC (SAE1006) export index dropped by a mere $7/t w-o-w to $708/t FOB east coast this week. Indian mills have been inactive in Vietnamese market for quite some time. Meanwhile, after the decline in Chinese HRC prices in the Middle East market, Indian manufacturers who are eyeing higher realisations withdrew offers. Moreover, mills are anticipating an increase in overseas market activities post-domestic price increases in some of the importing countries.

Leave a Reply