- Raw materials and semi-finished steel prices strengthened amid improved demand and sentiment.

- Finished steel markets stayed weak with mixed prices due to slow demand

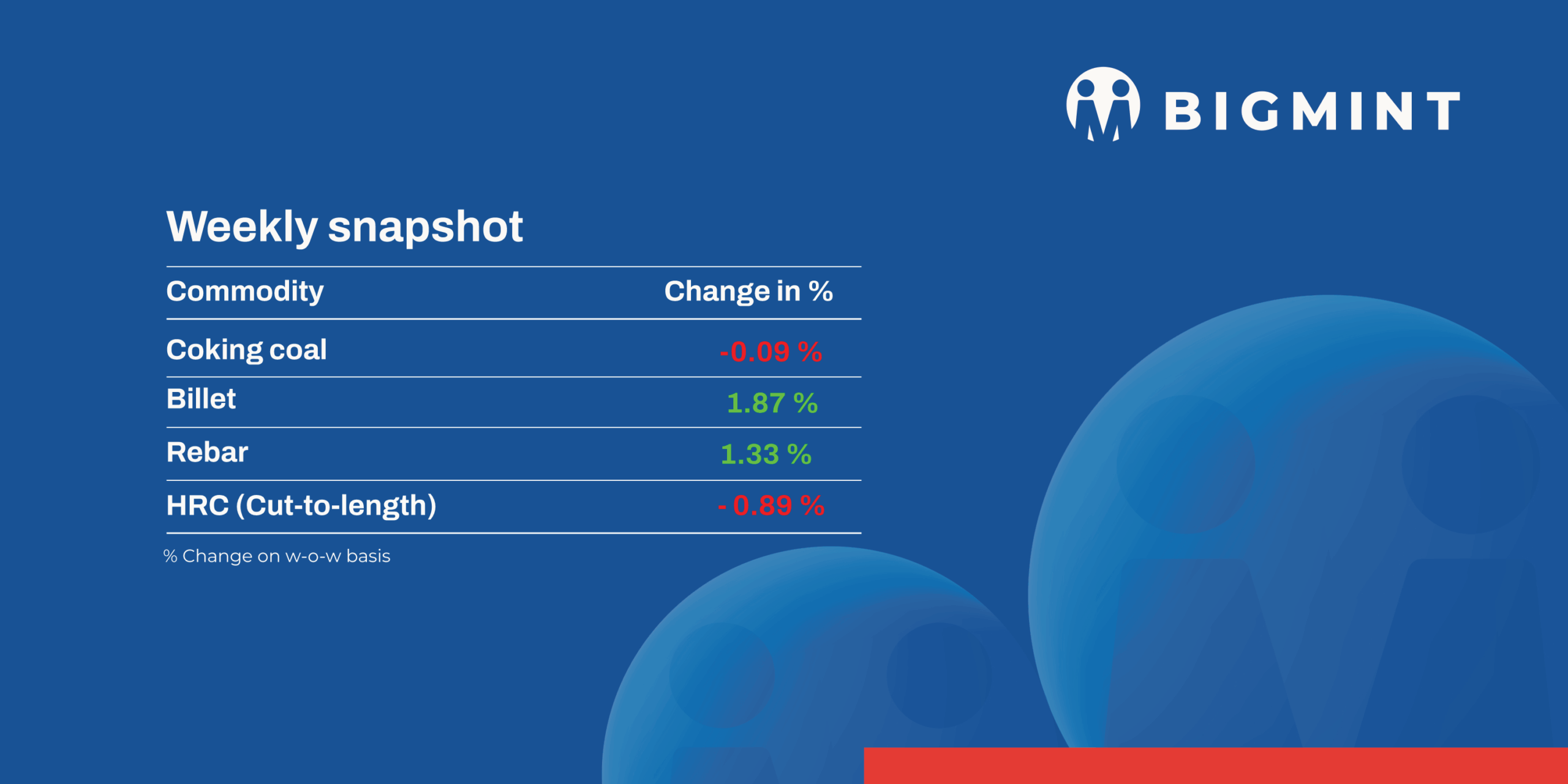

India’s domestic steel market saw strong momentum in the week ended 46, with semi-finished prices rising by between INR 200-900 per tonne, amid improved demand and steadily strengthening market sentiment this week.

Iron ore and pellet

- NMDC has revised its list prices of iron ore CLO (calibrated lump ore) and announced fines prices on 15 November 2025, BigMint learnt from sources. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 6,250/tonne (t) ($71/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,750/t ($54/t). Prices are on FOR basis from the miner’s Bacheli complex and include royalty, DMF, and NMEDT. DR CLO prices have been increased by INR 50/t while fines tags have been kept unchanged. Notably, the miner had last revised prices on 22 October 2025. PELLEX, BigMint’s bi-weekly domestic pellet (Fe63%) index for Raipur, fell by INR 300/t ($4/t) w-o-w to INR 9,700/t ($109/t) DAP on 14 November. Deals for around 160,000 t were concluded by buyers from local and Odisha based pellet sellers. Earlier, Raipur-based pellet producers reduced their offers for 63/63.5% (+/-0.5%) material by INR 300/t ($4/t) to INR 9,600-9,900/t ($108-111/t) exw on 8th Nov.

- NMDC Chhattisgarh auctioned 69,900-t iron ore from Bacheli on 13 Nov’25, with around 40,400 t booked. 12,900-t DR CLO (10-40 mm, Fe 67%, base INR 6,250/t) and 6,000-t lumps (10-20 mm, Fe 65.5%, base INR 5,700/t) were sold at 15% and 14.5% premiums, respectively. Of 43,000-t fines (Fe 64%), 21,500 t were sold at base price INR 4,790/t. 8,000-t ROM (10-150 mm, Fe 65.5%) remained unsold. Prices were on FOR basis, including royalty, DMF, & NMEDT.

- BigMint’s bi-weekly export index for Indian low-grade iron ore fines (Fe 57%) dropped by $3.5/t w-o-w to $67.5/t FOB east coast as of 13 November. Export prices softened amid subdued buying interest from seaborne customers and weakening fundamentals in the Chinese market. Around 325,000 t of iron ore export deals were recorded in this publishing window. Discounts widened for Fe 57% fines, averaging 16-17% against the benchmark index.

Coal

- South African thermal coal prices firm w-o-w at Indian ports, with RB2 rising to INR 8,300/t at Paradip, INR 8,350/t at Vizag and INR 8,400/t at Gangavaram, while RB3 moves to about INR 7,200/t. The increase follows stronger FOB values – RB2 at $75-76/t and RB3 at $60-61/t – supported by vessel shortages, higher Feb-Mar forward freight and steady Chinese buying. Portside stocks eased to 12.57 mnt, yet local demand remains weak as buyers resist higher offers. Prices are likely to stay supported, though meaningful buying may not return until the bid-offer gap narrows.

- Domestic coal prices stayed unchanged w-o-w, with 5,000 GCV at INR 6,350/t and 4,500 GCV at INR 5,250/t ex-Bilaspur. The recent SECL auction saw stronger bidding despite limited volumes, as traders held low stocks and competed more actively. SECL has also withdrawn the grade guidelines issued in October. The upcoming SECL auction on 20 Nov’25 will offer 784,000 t of non-coking coal across G3-G9 and G11, likely drawing firm participation amid tight spot availability.

- BigMint’s PHCC index moves to $213/t CNF Paradip, up $2 w-o-w, supported by two concluded Australian cargo deals of 30,000 t each — one at 98.5% index and another on a 50:50 index-fixed basis. Market indications hover around $213-215/t as mills note a gradual correction.

- Met coke prices show a mixed pattern this week, with the east seeing modest gains and the west holding stable. BF-grade met coke reached INR 31,500/t ex-Jajpur, rising INR 500/t w-o-w, supported by firmer demand and higher coking coal costs. Gandhidham stayed unchanged at INR 30,000/t, while foundry-grade met coke in Rajkot moved to INR 35,700/t, up INR 200/t.

Ferrous scrap

- India’s imported scrap market saw moderate activity, driven mainly by selective buying from East and West Coast mills. Two major bookings emerged — an Australian lot at $347–348/t CFR and a UK-origin parcel at $315/t CFR.

- Shredded scrap offers held at $350–354/t CFR, while HMS 80:20 was quoted at $320–325/t, though workable bids were $5–8/t lower. Mozambique HMS 1% was offered at $330/t against $325 bids, Poland HMS at $325/t, and Ireland-origin turning (3% impurities) at $310/t against $295 bids. Shredded remained unappealing, with buyers targeting sub-$350 levels.

- Domestic finished steel prices remained range-bound, keeping mills cautious.

- Roughly 26,000 t were booked in total — about 15,000 t of HMS grade at $315–353/t and 10,000 t of shredded at $347-353/t, with the remainder in HMS 60:40, PNS, and NTP, all on a CFR Chennai, Mundra, Pipavav, and Vizag basis.

Ferro alloys

- Indian silico manganese (60-14) prices remained largely stable, easing by INR 350/t w-o-w to INR 71,300-71,500/t in Durgapur, Raipur, and Vizag. Weak buying interest and limited support from the finished steel sector kept demand subdued, preventing any price gains and causing a slight softening.

- Ferro Manganese:Indian ferro manganese (HC 70%) prices inched down by INR 500/t ($6/t) w-o-w to INR 72,700/t ($820/t) exw-Durgapur, while prices in Raipur went up by INR 600/t ($7/t) w-o-w to INR 73,700/t ($831/t). The decline in Durgapur was driven by weaker local buying, whereas Raipur saw gains due to tighter regional supply and slightly stronger procurement.

- Ferro Silicon:Indian ferro silicon (Si 70%) prices increased by INR 2,300/t ($26/t) w-o-w to INR 90,000/t ($1,015/t) exw-Guwahati, while Bhutan’s prices rose by INR 3,500/t ($39/t) to INR 91,500/t ($1,032/t). Prices strengthened as most sellers raised their offers amid a slight supply shortage,with some key Bhutanese suppliers ran out of stock.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si 4%) prices declined by INR 2,000/t ($23/t) w-o-w to INR 115,500/t ($1,302/t) exw-Jajpur. The market remained quiet, with limited inquiries and weak end-user demand.

- Meanwhile, at Vedanta-FACOR’s ferro chrome auction on 13 Nov’25, the larger lot (Cr 52–55% min, 10-150 mm) fetched an H1 price of INR 110,100/t ($1,241/t)exw, down by INR 5,000/t ($56/t)from the previous auction. The smaller lot of the same grade and size closed at INR 112,800/t ($1,272/t) exw.

Semi Finished

- Indian semi-finished steel prices strengthened this week, as per BigMint’s assessment, Billet Index-Raipur increased by INR 650/t ($7/t) w-o-w. However, domestic billet prices raised by INR 200-750/t ($2-8/t) across major markets. The uptrend was backed by marginal improvement in demand in both semi-finished and finished steel segments, lifting spot prices w-o-w. Sponge iron prices also increased by INR 150-950/t ($1-10/t) across key regions, supported by a moderate pickup in bookings. However, Durgapur and Chennai witnessed slight declines of INR 100-300/t ($1-3/t) w-o-w, reflecting regional differences in buying behaviour.

- NMDC’s steel plant in Nagarnar, Chhattisgarh, auctioned 5,000 t of steel-grade pig iron on 7 Nov’25, with the entire quantity booked at an average price of INR 30,850/t (by road). However, management approval is still pending. Bids improved compared to the previous auction on 30 Oct, which saw an average price of INR 30,500/t (by road).

- SAIL-BSL in Bokaro, Jharkhand, held a steel-grade pig iron auction on 12 Nov’25, offering 6,000 t. Buyers booked the entire quantity at an average price of INR 31,450/ t. Bids increased by INR 750/t from the previous auction on 28 Oct, where out of the 9,000 t offered, 4,200 t were booked at an average price of INR 30,700/ t.

- SAILs Rourkela Steel Plant (RSP) conducted an auction on 14 Nov’25 for 2,500 t of steel-grade pig iron, in which the entire quantity was booked at an average price of INR 32,150/t exw. This marks an increase of INR 450/t compared to the previous auction on 3 Nov, in which the entire quantity of 4,000 t was sold at INR 31,700/t exw.

- Indian DRI (Direct Reduced Iron) export offers increased by $2–4/t w-o-w, assessed at $314/t CPT Raxaul for Nepal and $326/t CPT Benapole for Bangladesh. Supported by improved bookings, particularly from Bangladesh, where enquiries strengthened. In contrast, demand from Nepal remained subdued, with limited buying interest despite the slight upward adjustment in offers.

Finished Long Steel

- IF-rebar: The Induction Furnace route rebar market saw a mid-week improvement in trading activity, with a modest rise in buying. Manufacturers observed that bookings were made at lower price levels. Following consistent bookings and improved liquidity, sellers raised their price quotes. However, buyer resistance at higher prices slowed sales. Market participants also noted better dispatch and lifting of previously booked material. Despite this progress, inventories remain around 12 to 15 days. In the near term, the market is expected to fluctuate slightly and remain range-bound until new bookings from mills support price increases.

- BF-rebar:India’s trade-level blast furnace (BF) rebar prices dropped w-o-w across major markets owing to slow demand. Some primary mills either offered price support or reduced list prices amid weak market sentiments.

- Trade-level BF rebar prices dropped by INR 500/tonne (t) ($6/t) w-o-w to INR 47,300/t ($533/t) exy-Mumbai, as per BigMint’s benchmark assessment on 14 November 2025.

- In the projects segment, prices hovered between INR 45,500-46,500/t ($513-524/t) FOR Mumbai.

Flat Steel

- Trade-level prices of hot-rolled coils (HRCs) in India showed mixed trends w-o-w. Some markets saw a downtrend, while others remained firm. HRC prices hovered between INR 46,500-48,300/t ($525-546/t) across regions, while cold-rolled coil (CRC) prices ranged between INR 52,000-56,500/t ($588-538/t).

- Domestic HRC market sentiment remained subdued amid weak demand and slow trade. Moreover, liquidity constraints continued to pressure transactions, while distributors struggled to secure workable prices, making it difficult to conclude deals.

- India’s bulk imports of HRCs touched 62,440 t as of 8 November 2025, based on vessel line-up data. Around 137,500 t of additional cargoes are expected by the end of November and India’s bulk exports of HRCs touched 86,992 t as of 8 November 2025, and around 61,000 t of additional cargo are in transit.

- BigMint’s Indian hot-rolled coil (HRC, S275) export index for Europe fell by $5/t w-o-w to $540/tonne (t) FOB main port. Notably, an unconfirmed deal was heard concluded for November shipments at slightly lower levels. The Indian HRC (SAE 1006) export index for the Middle East and Vietnam remained steady w-o-w. This stability in prices is attributed to slow demand in both the regions.

Leave a Reply