- Firm sentiment persists amid tight supply, supportive global cues

- Elevated prices, cautious sentiment keep trade largely need-based

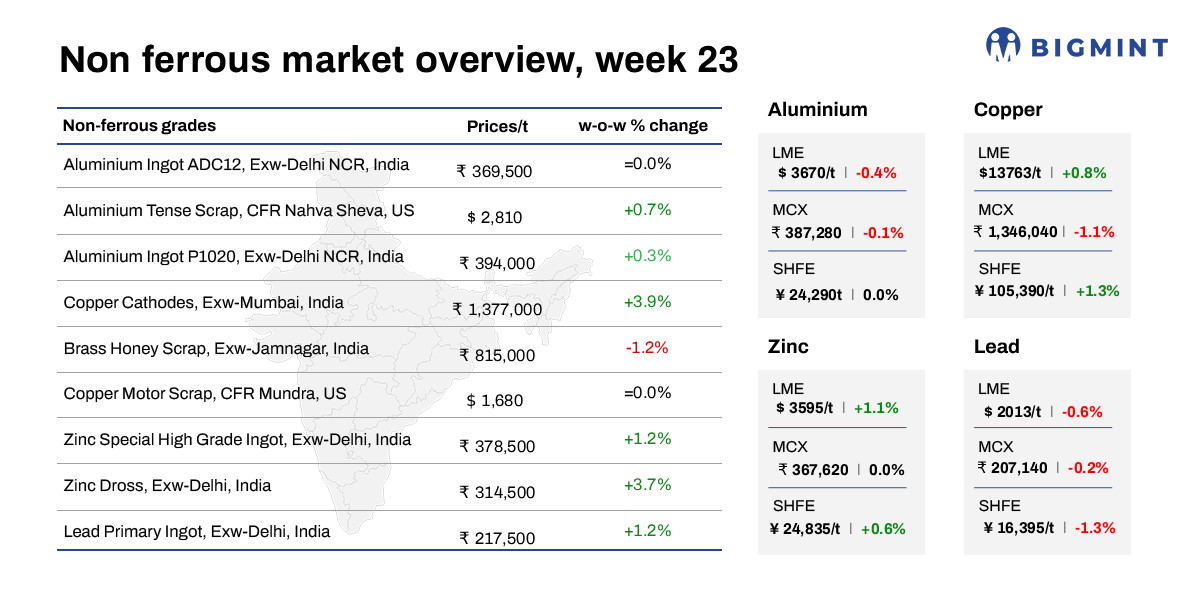

LME base metals prices showed a mixed trend in the week ended 5 June 2026, with zinc recording the highest increase of 1.08% to $3,595/t, followed by copper, which rose 0.78% to $13,763/t. Meanwhile, nickel registered the sharpest decline of 2.67% to $18,615/t, while lead and aluminium edged lower by 0.59% and 0.42% to $2,013/t and $3,670/t, respectively.

On the inventory side, copper stocks recorded the steepest decline, falling 2.62% to 379,225 t, followed by zinc inventories, which dropped 2.50% to 110,950 t. Aluminium, lead, and nickel stocks also declined by 1.42%, 1.16%, and 0.95% to 333,200 t, 310,350 t, and 274,236 t, respectively, indicating relatively tighter exchange availability across major base metals.

Aluminium

India’s imported aluminium scrap market remained firm w-o-w, supported by stable overseas scrap availability conditions and continued strength in broader domestic aluminium sentiment, although buying activity remained largely need-based amid elevated offers.

UK-origin Zorba 95-5 scrap, CFR Nhava Sheva, increased by $60/t w-o-w to $3,040/t from $2,980/t, reflecting firmer supplier offers and improved global market sentiment. Meanwhile, US-origin tense scrap (attachments 6-7%), CFR Nhava Sheva, rose by $20/t to $2,810/t from $2,790/t, indicating improved demand amid supportive market cues.

On the domestic front, aluminium prices remained firm w-o-w, supported by stronger MCX trends despite softer LME aluminium prices. P1020 ingot prices, exw Delhi NCR, increased by INR 10,000/t, or around 2.5%, to INR 403,000/t. Firm domestic sentiment and supportive producer offers continued to support prices, while buying activity remained largely requirement-based.

Overall, the imported aluminium scrap market remained firm, with higher Zorba and tense prices reflecting tighter supply conditions, improved supplier sentiment, and continued resilience in the broader aluminium complex.

Copper

India’s copper scrap market displayed a cautious to stable trend w-o-w, despite gains in London Metal Exchange (LME) copper prices. The supportive global copper trend and ongoing US tariff-related supply concerns continued to support domestic scrap values, while buying activity remained largely requirement-driven amid elevated price levels.

Demand from key consuming regions remained largely need-based, with buyers continuing to procure material cautiously despite supportive broader copper market sentiment.

The market remained supported by firmer copper prices and positive sentiment across the value chain. However, elevated price levels limited aggressive restocking, keeping trading activity largely confined to immediate requirements.

According to BigMint’s assessment, brass honey scrap prices in India declined w-o-w to INR 815,000/t, tracking correction and profit-booking in LME copper prices after the recent rally. However, steady imported scrap availability and balanced buying activity continued to keep the market largely rangebound.

Overall, supportive global copper trends continued to support domestic scrap prices during the week, although market participation remained largely requirement-driven

Zinc

India’s zinc ingot (99.995%) prices increased moderately by around INR 6,000/t w-o-w to INR 384,000/t ex-Delhi, supported by firmer global zinc prices and sustained producer pricing discipline, although downstream demand remained largely need-based.

The domestic market continued to track Hindustan Zinc Limited (HZL), which raised its zinc ingot prices by INR 7,400/t to INR 383,600//t in its latest revision.

India’s zinc dross and zinc oxide prices increased further w-o-w, supported by firm global cues and continued strength in LME zinc prices. Benchmark three-month LME zinc prices increased to $3,595/t during the week from $3,556/t a week earlier, continuing to lend support to domestic secondary zinc markets.

Lead

India’s domestic lead market remained firm w-o-w. Lead primary ingot (ex-Delhi) was assessed at INR 217,500/t, up by INR 2,500/t from INR 215,000/t a week earlier, reflecting improved domestic sentiment and stronger producer pricing despite largely need-based buying activity.

The domestic market continued to track Hindustan Zinc Limited (HZL), which increased its lead ingot prices by INR 1,900/t to INR 228,800/t in its latest revision, indicating continued producer support amid firm domestic lead market trends.

On the global front, LME lead prices declined marginally by 0.59% w-o-w to $2,013/t, while exchange inventories decreased by 1.16% to 310,350 t. Lower exchange stocks and supportive domestic pricing continued to lend support to the overall lead market sentiment despite softer LME prices.

Overall, domestic lead prices remained supported by firmer producer pricing and improved domestic market sentiment, although buying activity continued to be driven largely by immediate requirements, limiting aggressive market participation.

Leave a Reply