- Coking coal prices hold firm, though met coke falls

- Portside Indonesia, SA thermal coal remains stable

The Indian coal market remained subdued this week, with muted demand from the industrial sector and steady prices across most domestic and imported grades. Limited buying interest, cautious trader sentiment, and sufficient portside stocks kept market activity sluggish. Despite occasional upticks in sponge iron and freights, overall momentum stayed weak, reflecting uncertainty in short-term demand recovery.

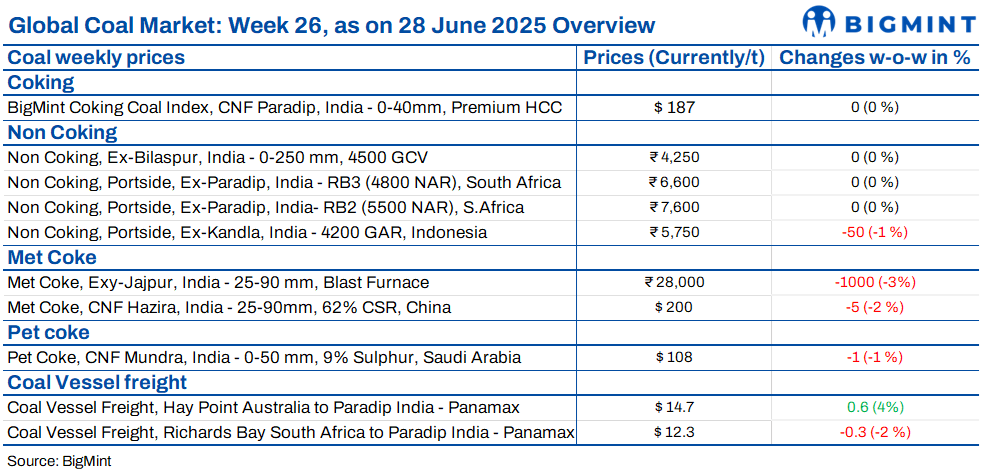

BigMint’s coking coal index remains flat w-o-w in absence of active trades: BigMint’s premium hard coking coal (PHCC) index was assessed at $187/tonne (t) CNF Paradip, India, on 27 June 2025, stable w-o-w. High port stocks, lower bids, and falling met coke prices were the primary reasons behind the absence of active trades.

India’s met coke prices fall again as buying stays low: Met coke prices in India dropped further this week amid weak steel sector demand and ongoing policy uncertainty. As per BigMint’s assessment on 25 June, the 25-90 mm BF grade slipped by INR 1,000/t w-o-w to INR 28,000/t ex-Jajpur, while prices in Gandhidham edged down by INR 150/t to INR 29,000/t. Limited buying and lack of clarity regarding the QR policy kept market sentiment subdued despite signs of stability in China’s coke market.

Portside Indonesian coal prices hold steady amid weak demand: Indonesian coal prices stayed under pressure across Indian ports during the week ending 27 June due to weak demand from sectors such as steel and textiles. The 5000 GAR and 4200 GAR grades slipped INR 50/t w-o-w, while 3400 GAR held steady. Despite lower indexed prices, local values remained mostly stable amid controlled stock replenishment and muted industrial buying. Overall sentiment stayed cautious due to the start of the monsoon season.

South African coal portside prices remain stagnant: South African portside coal prices held steady this week despite an uncertain market. RB2 (5500 NAR) was assessed at INR 7,600/t and RB3 (4800 NAR) at INR 6,600/t exw-Gangavaram. CNF deals were heard at $76/t for RB2, with FOB deals at $66-68/t. Domestic coal prices also remained flat amid poor demand, while portside stocks dipped slightly. Sponge iron prices showed marginal gains, but overall market sentiment stayed cautious.

Domestic coal prices in India flat w-o-w: Domestic coal prices remained unchanged this week, with 5000 GCV and 4500 GCV grades assessed at INR 4,700/t and INR 4,250/t exw-Bilaspur, respectively, as per BigMint. Market activity stayed subdued due to poor industrial demand. SECL’s recent auctions witnessed limited buyer participation, reflecting ongoing caution and uncertainty in the market amid the monsoon season and sluggish offtake.

India’s pet coke prices stay firm, but monsoon clouds demand: Imported pet coke prices in India were largely unchanged this week. US-origin offers were assessed at $107-109/t CFR across both eastern and western ports. Saudi-origin offers eased slightly by $1/t w-o-w to $108-110/t CFR. Freights from the US Gulf Coast to the western coast of India remained steady at $35-36/t for Panamax vessels. Demand stayed subdued and may drop further as the monsoon spreads across key regions.

Leave a Reply