- Ample domestic supply pressures imported prices

- Portside thermal coal stocks rise 4.3% in week 24

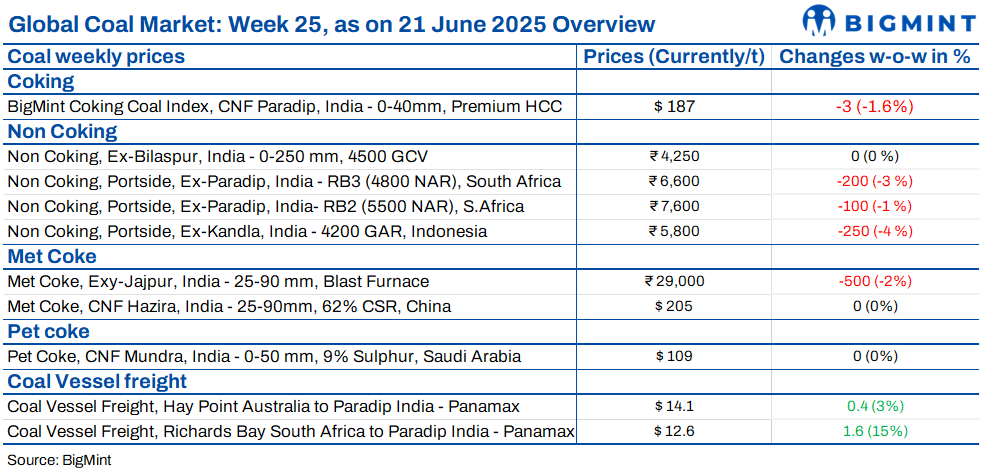

India’s coal market remained subdued this week due to weak demand from key sectors such as steel and cement. Ample domestic supply and cautious buying limited activity across both imported and domestic segments. Traders continued to operate conservatively, with monsoon conditions and high stock levels further dampening sentiment across coal grades and ports.

Portside Indonesian coal prices fall amid weak demand, ample supply

Indonesian thermal coal prices dropped across Indian ports this week as weak demand, strong domestic coal availability, and higher vessel arrivals dampened market activity. Industrial buyers from sectors such as steel, cement, and textiles limited purchases to immediate needs. Domestic coal remained preferred by power plants, further reducing import interest.

BigMint assessed the 5000 GAR grade down by INR 250/t w-o-w to INR 7,450/t at Kandla and INR 7,350/t at Vizag. The 4200 GAR grade dropped INR 250/t to INR 5,800/t at Kandla, and the 3400 GAR grade slipped INR 200/t to INR 4,300/t at Navlakhi. Global benchmarks also declined amid oversupply and weak Chinese demand. Outlook stays bearish on poor buying sentiment.

South African coal prices dip amid weak demand, rising stocks

South African thermal coal prices dropped again at Indian ports this week due to sluggish demand and increased stock levels. RB2 (5500 NAR) fell by INR 100/t w-o-w to INR 7,600/t exw-Gangavaram, while RB3 dropped by INR 200/t to INR 6,600/t. At Vizag, both RB2 and RB3 declined by INR 200/t to INR 7,450/t and INR 6,450/t, respectively. Sellers faced pressure to clear inventories, and some traders reportedly made low offers to influence index levels.

Portside coal stocks rose by 4.3% to 16 mnt in week 24 of CY’25, supported by improved vessel arrivals. Export prices also fell, with RB2 down to $67.50/t FOB. Meanwhile, Transnet has scheduled a 12-day rail maintenance in South Africa next month.

Sentiment in India remains weak for now. Additionally, export prices may stay soft unless freights or global demand picks up.

Domestic coal prices hold steady amid subdued demand

Domestic coal prices remained stable w-o-w, with muted demand and adequate stock levels keeping the market quiet. BigMint assessed 5000 GCV at INR 4,700/t and 4500 GCV at INR 4,250/t exw-Bilaspur. SECL’s recent auction saw limited participation, as buyers refrained from active bidding amid stagnant prices and weak industrial coal intake. Overall sentiment remained cautious in the domestic coal market.

BigMint’s coking coal index eases on weak market cues

BigMint’s PHCC index dropped by $3/t w-o-w to $187/t CNF Paradip amid weak demand and lower met coke prices. Bids remained low, with a mill source suggesting that the index should reflect $184/t CFR levels. Sellers found it tough to close deals even at $170/t FOB. Indian met coke prices dropped INR 500/t w-o-w to INR 29,000/t ex-Jajpur, while Australian PHCC prices slipped to $176/t FOB. Market sentiment was subdued.

Met coke market stays weak amid QR uncertainty, slow steel demand

Met coke prices in India fell further this week due to weak steel demand and uncertainty over the continuation of quantitative restrictions (QRs) on imports. The blast furnace grade dropped INR 500/t w-o-w to INR 29,000/t ex-Jajpur, while Gandhidham saw a decline of INR 350/t to INR 29,150/t. Clarity on QRs is awaited following recent discussions, as current restrictions are set to end in June. Globally, China’s met coke market remains under pressure due to the steel off-season and expectations of another round of price cuts. Meanwhile, Australian PHCC prices slipped $6/t to $175/t FOB.

US pet coke prices in India inch up, demand stays dull

US-origin pet coke offers in India moved up by $1/t w-o-w to $107-109/t CFR at eastern and western ports. Despite this, demand remained weak due to slower cement sector intake with the monsoon underway. Saudi-origin offers stayed stable w-o-w at $109-111/t CFR, backed by tight supply and high freight costs. Overall, market sentiment stayed muted despite the slight rise in prices.

Coal vessel freights mixed amid tight Pacific tonnage supply

Coal freights to India showed mixed trends last week, with gains seen on Australia and South Africa routes, while Indonesia-India rates dipped. The Pacific Basin experienced tight vessel availability, especially for early-July loadings, driving up Panamax freights. In contrast, Supramax rates weakened as charterers resisted higher offers. Meanwhile, Indian portside coal inventories rose by 4.3% to 16 mnt, slowing new bookings. Baltic indices reflected improving vessel demand, with the Baltic Dry Index (BDI) and Baltic Panamax Index (BPI) rising w-o-w. Notably, a SAIL Panamax vessel was booked from Australia at $16.6/t for July shipment, while Richards Bay Coal Terminal (RBCT)-Paradip rates rose $1.6/t to $12.6/t.

Leave a Reply