- Monsoon-driven weak demand and high inventories pressured steel, rebar, billet and scrap.

- Infrastructure awards, exports and pig iron auctions offered limited support

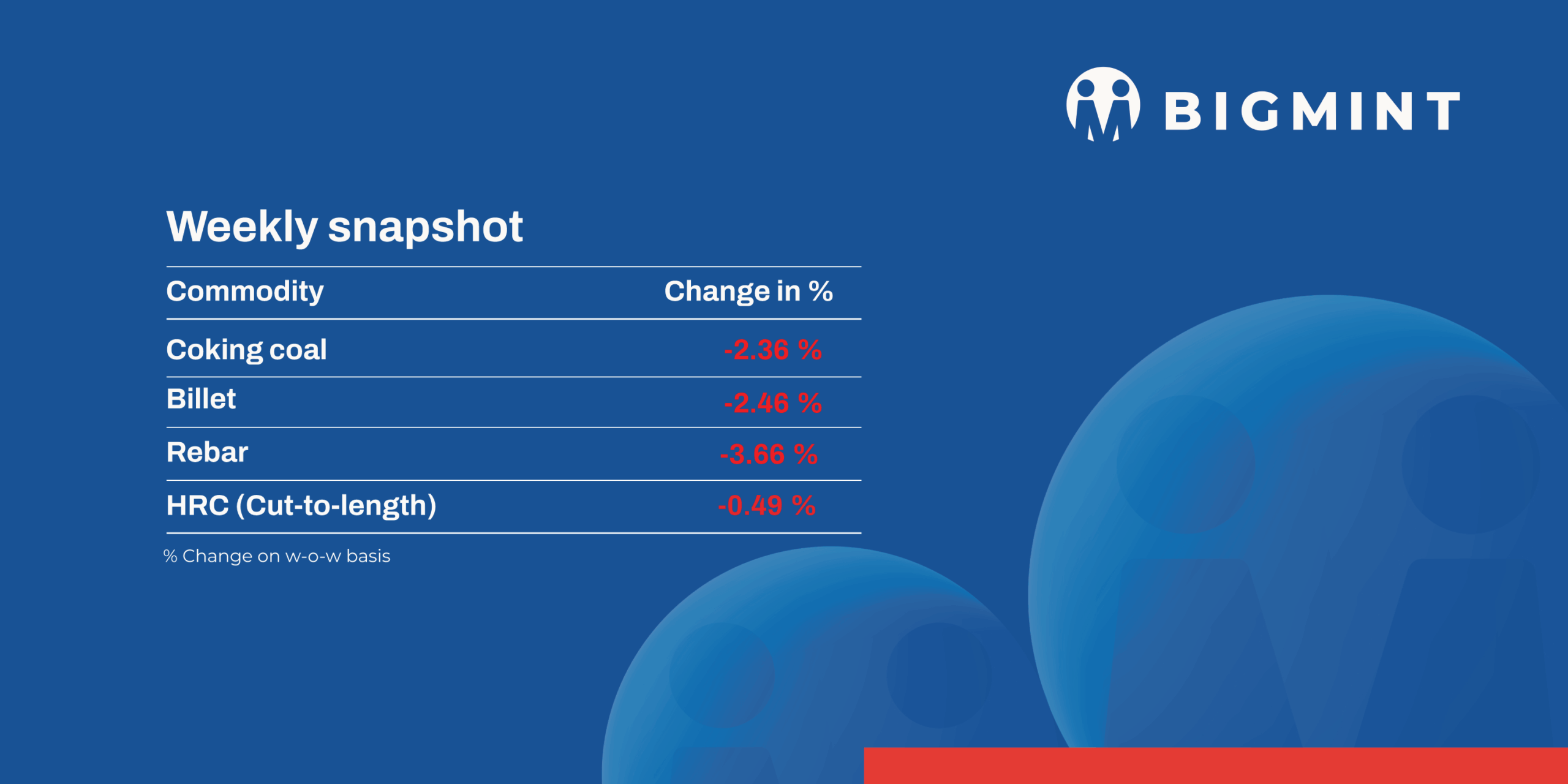

Weak construction activity, falling raw material and steel prices, cautious buying, and elevated inventories kept Indian steel markets under pressure despite infrastructure awards and improved export activity.

Iron ore and pellet

- NMDC has reduced its list prices of iron ore CLO (calibrated lump ore) and fines on 10 July 2026, BigMint learnt from sources. The miner has fixed prices of DR CLO (10-40 mm, Fe 67%) at INR 5,850/tonne (t) ($61/t) and of iron ore fines (-10 mm, Fe 64%) at INR 4,700/t ($49/t). Prices are on FOR basis from the miner’s Bacheli complex and exclude royalty, DMF, and NMEDT. Prices of all grades have decreased in the range of INR 150-500/t.

- BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index increased by $4/t w-o-w to $103/t FOB east coast on 10 Jul’26. Eastern India-based pellet-makers concluded 400,000 t pellet (Fe 63%, 3-3.5% Al2O3) export deals at $117-118/t CFR China this week for the August laycan.

The Odisha Directorate of Mines & Geology (DoMG) has intensified action against iron ore grade manipulation and dispatch irregularities, directing field officials to explain monitoring lapses after inspections found several mines dispatching ore below approved grades. Over 60 mining leases across key producing regions were flagged for deviations in Q1 FY’27, raising concerns over revenue losses from lower royalty and auction premium collections. - Pacific Iron Manufacturing Ltd. (PIML) has started commercial production and sales of iron ore concentrate from its newly commissioned beneficiation plant at the Dhaukan-Dhaurra-Urdaurra iron ore block in Prithvipur tehsil, Niwari district, Madhya Pradesh, marking a significant step towards developing an integrated iron ore value chain in central India. The beneficiation plant has an installed capacity of around 1.4 million tonnes per annum (mnt) and is expected to cater exclusively to the domestic market.

Coal

- South African thermal coal prices weakened further during the week, with ex-Paradip RB2 (5,500 NAR) declining by INR 100/t w-o-w to INR 10,450/t and RB3 (4,800 NAR) by INR 550/t to INR 8,850/t. At Vizag, RB2 fell by INR 150/t to INR 10,250/t, while RB3 dropped by INR 450/t to INR 8,850/t. Meanwhile, domestic 5,000 GCV coal remained stable at INR 5,500/t and 4,500 GCV at INR 4,050/t. Comfortable Coal India supplies, healthy participation from cement producers in CIL auctions and adequate domestic availability continued to reduce import dependence. Weak steel and sponge iron demand, coupled with the monsoon, kept buying strictly requirement-based and traders under pressure to clear inventories.

- India’s domestic met coke market recorded mixed trends during the week. BF-grade coke prices in eastern India declined by INR 750/t w-o-w to INR 35,250/t ex-Jajpur, while western India remained stable at INR 34,000/t ex-Gandhidham. Foundry-grade coke also held steady at INR 36,400/t ex-Rajkot, while Indonesian BF-grade met coke (65/63 CSR) increased by $1/t to $319/t CFR India. The expiry of the anti-dumping duty and continued uncertainty over its extension kept buyers cautious and limited spot transactions. Weak steel demand pressured domestic prices, while firm Chinese coke fundamentals and elevated coking coal costs prevented a sharper decline in international prices.

- BigMint’s premium hard coking coal (PHCC) index declined by $9/t w-o-w to $254/t CNF Paradip during the week as lower steel prices and weaker buyer bids weighed on the market. Indian primary steel mills reduced July rebar list prices by INR 1,000-3,000/t m-o-m, while HRC and CRC prices were cut by INR 1,000/t, reflecting subdued demand, rising inventories and weak construction activity. Despite softer downstream sentiment, Panamax freight from Hay Point to Paradip increased by $0.4/t to $19.3/t, while resilient Australian cargo activity provided partial support to seaborne coking coal prices, limiting further downside.

Ferrous Scrap

- Imported ferrous scrap market remained subdued throughout the week as well; mills continued need-based procurement amid weak steel demand and poor import economics. Buying interest for containerised cargoes stayed limited due to a persistent bid-offer gap and weak import viability. Sentiment weakened further toward the week-end as renewed geopolitical tensions in the Middle East revived concerns over vessel availability, freight costs and supply chain disruptions.

- Offer indications for Africa-origin LMS remained around $290/t C&F Mundra (CAD), while HMS was heard at $330/t C&F Mundra (CAD). Europe/UK-origin HMS was workable at $320-330/t CFR, while shredded scrap offers softened to $375-385/t CFR but remained above buyers’ workable levels of $350-370/t CFR. Market participants indicated workable import prices had declined by $5-10/t compared with the previous week.

Ferro alloys

- Silico Manganese:Indian silico manganese (60-14) prices declined by INR 750/t ($8/t) w-o-w to INR 74,900-75,600/t ($786-793/t) across key markets. Domestic steel mills largely restricted purchases to immediate requirements amid weak finished steel demand, limiting alloy procurement.

- Meanwhile, HC 65-16 silico manganese export prices edged down by $5/t to $918/t FOB Vizag/Haldia.

- Ferro Manganese:Indian ferro manganese (70%) prices remained largely steady with slight decline w-o-w by INR 500/t ($5/t) to INR 78,500/t ($823/t) in Raipur and by INR 400/t ($4/t) to INR 78,400/t ($822/t) in Durgapur. Prices eased marginally amid subdued domestic demand, cautious export enquiries, and adequate material availability, prompting suppliers to offer limited discounts to secure orders.

- Meanwhile, export prices for the 75% grade also dipped by $4/t w-o-w to $926/t FOB Vizag/Haldia.

- Ferro Silicon:India ferro silicon (Si 70%) prices dropped by INR 1,500/t ($16/t) w-o-w to INR 88,000/t ($923/t) ex-works Guwahati, while Bhutan prices also fell by INR 1,000/t ($10/t) to INR 88,700/t ($930/t). The market remained bearish this week after Bhutan’s July offers dropped by INR 9,000/t ($94/t) m-o-m exw, weighing on sentiment. The correction was largely expected as domestic prices had been under pressure over the past month amid cautious buying and expectations of lower offers.

- Ferro Chrome:Indian high-carbon ferro chrome (HC 60%, Si: 4%) prices remained broadly stable, edging down by INR 400/t ($4/t) w-o-w to INR 122,800/t ($1,288/t) exw-Jajpur. The market witnessed limited price movement as subdued buying interest and cautious procurement from end-users kept overall trading activity range-bound.

Semi finished

- India’s semi-finished steel prices tumble as weak demand and aggressive competition pressure spot market during the week ended 11 July’26, as weak demand and limited procurement across both the semi-finished and finished steel segments continued to weigh on prices. According to BigMint’s assessment, domestic billet prices declined by INR 300-1,900/t ($3-20/t) w-o-w across major production regions, with aggressive competition among neighbouring markets accelerating the correction in spot prices.

- Buying activity remained weak throughout the week, with most re-rollers and traders procuring only against immediate production requirements. Lower bids from buyers, coupled with an oversupply of competitively priced material from nearby markets, widened the gap between buyer expectations and seller offers, resulting in a significant drop in weekly billet trade volumes recorded compared with the previous week.

- Western India witnessed the sharp corrections, with Mumbai, Jalna and Gujarat recorded price declines of INR 1,000-1,900/t ($10-20/t) w-o-w. Weak end-user demand, particularly from the finished steel, reduced procurement by rerollers, while sellers lowered offers to remain competitive amid abundant regional material availability.

- The sponge iron market also extended its downward trend during the week. Prices across major producing regions fell by INR 100-600/t ($1-6/t) w-o-w as induction furnace operators continued to restrict purchases. Buying interest remained weak due to the availability of competitively priced sponge iron from neighbouring markets and bulk offers from traders. In several cases, local sponge iron producers maintained higher offer levels than nearby suppliers, prompting buyers to source material from alternative markets and further reducing spot demand.

- India’s direct reduced iron (DRI) export market recorded an improvement in trading activity. Lower offer levels encouraged buyers in neighbouring countries to return to the market after several weeks of subdued procurement. Pellet-based sponge iron export offers to Nepal declined by $2/t w-o-w to $267/t CPT Raxaul, while CDRI/mix sponge iron offers fell by $4/t to $295/t CPT Raxaul. Export offers to Bangladesh also eased by $1/t to $302/t CPT Benapole.

- NMDC’s Nagarnar Steel Plant auctioned 7,000 t of steel-grade pig iron on 9 July 2026, with the entire quantity sold at an average price of INR 36,500/t ex-works. In the previous auction held on 2 July, the company sold 6,000 t of steel-grade pig iron at an average price of INR 36,100/t ex-works. The latest auction recorded an INR 400/t increase in prices.

- SAIL-RSP sold the entire 3,500 t of steel-grade pig iron offered in its auction on 10 July 2026 at an average price of INR 37,650/t exw. The auction opened at INR 37,100/t and concluded at INR 38,200/t, reflecting steady bidding throughout the session, resulting in an average realisation of INR 550/t higher than the previous auction. In the previous auction held on 25 June 2026, the company had also sold the entire 3,500 t offered at an average price of INR 37,100/t exw.

Finished long steel

- IF-rebar:IF-route rebar prices declined across all major regions this week, primarily due to subdued demand following the onset of the monsoon, which slowed construction activity across key consuming markets. Trading activity remained limited as buyers continued to procure material only to meet immediate requirements, while mills and traders offered discounts to stimulate sales amid weak buying interest. Mill inventories were maintained at around 10-15 days, with order booking visibility restricted to approximately 3-5 days. In the near term, rebar prices are expected to remain under pressure as intensified monsoon activity is likely to further weigh on construction activity and overall market sentiment.

On a week-on-week basis, rebar prices declined by INR 200-1,900/t across key regions, with the sharpest fall of INR 1,900 seen in the Mumbai market, while the southern region mostly remained stable, according to BigMint’s assessment.

Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10–25 mm size) were assessed at INR 39,300-39,700/t exw Raipur and INR 43,200-43,800/t exw Jalna.

Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 42,800–43,200/t exw Raipur.

Trade reference prices of wire rod stood at INR 41,600–42,200/t exw Raipur. - BF-rebar:India’s BF-route rebar market remained bearish, with Mumbai trade prices falling INR 500/t w-o-w to INR 49,000/t ex-Mumbai, a six-month low. Weak monsoon-driven construction activity, elevated distributor inventories, and aggressive IF-route pricing continued to suppress buying interest and keep market sentiment under pressure.workable project prices were heard at INR 47,000-49,000/t on a landed basis,

Flat steel

- BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Grade E250, 2.5-8 mm/CTL) in Mumbai declined w-o-w to INR 57,900/t ($606/t) from INR 58,200/t ($610/t) in the previous assessment as of 10 July.Likewise, the benchmark assessment for CRC (IS513, Grade O, 0.9 mm/CTL) declined by INR 200 ($2/t) to INR 65,000/t ($680/t) as of 10 July.

- India’s trade-level HRC market saw a dip this week as buyers stayed on the sidelines. Major mills have now cut prices by INR 1,000/t, but that hasn’t done much to lift the mood, as inventories are piling up. Stock levels have shot up in the north, while the south has seen only a small build-up. All in all, it’s still a sluggish market, if not completely dead.

- India’s bulk imports of HRCs touched 247,754 t in June. Around 245,229 t of additional cargoes are expected by early-August.

- India’s bulk exports of HRCs touched 235,773 t in June. Around 44,250 t of additional cargoes are expected to be shipped.

- Indian HRC export activity witnessed a marginal improvement during the assessment, though overall trading remained moderate.

- Competitive Indian offers and resilient demand from Vietnam supported export bookings, while subdued domestic demand prompted mills to allocate higher volumes to overseas markets. However, EU safeguard quota restrictions continued to cap shipments to Europe, limiting the overall upside in exports.

Leave a Reply