- IF and BF rebar prices declined further amid weak bookings and cautious market sentiment.

- Pellet, scrap, and ferro alloy prices softened as downstream steel demand remained subdued.

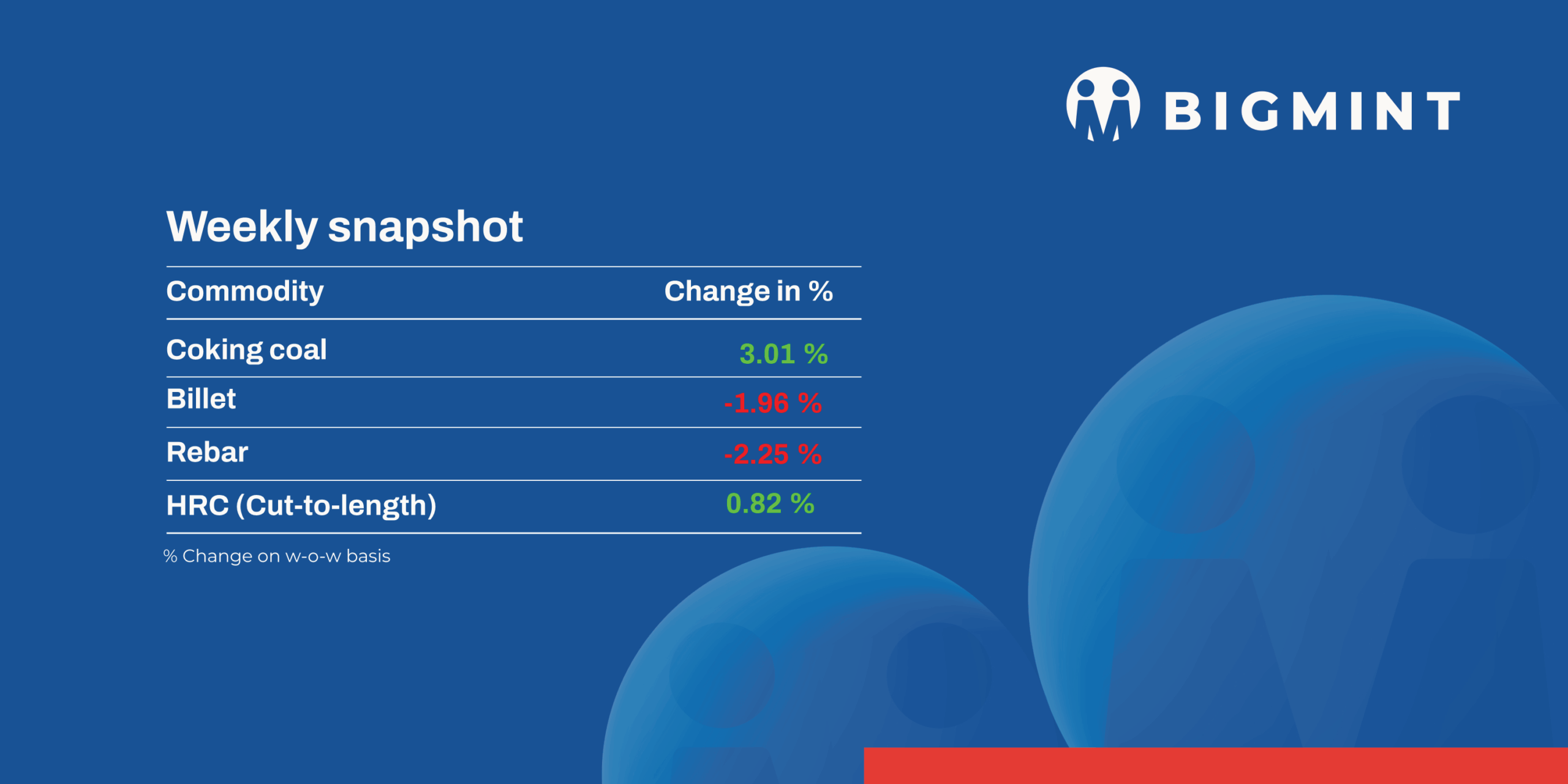

Weak steel demand, cautious buying activity, and rising inventories continued pressuring Indian ferrous markets, while raw material prices showed mixed regional trends.

Iron ore and pellet

- Dharti Dredging and Infrastructure Limited emerged as the preferred bidder for the Cavorem-Maina Mineral Block No. XVIII in Goa, securing the auction at an 88.88% premium. Located in South Goa’s Quepem taluka, the 165.4-hectare block holds around 13.88 mnt of iron ore resources with an average Fe grade of 54.26%, comprising 4.58 mnt of lumps and 9.3 mnt of fines. The mine also contains around 0.69 mnt of dump material, including 0.22 mnt of recoverable ore.

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur declined by INR 100/t ($1/t) w-o-w to INR 9,900/t ($103/t) DAP on 15 May. Pellet makers lowered offers by around INR 100-200/t at the beginning of the week, with ex-works Raipur offers for 62.5-63% (+/-0.5%) grade pellets largely heard at INR 9,700-9,800/t DAP Raipur, compared to INR 9,900-10,000/t in the previous week.

- During SAIL auctions held from Monday to Friday, around 56,000 t of iron ore (Fe 58.54-63%) was booked at prices ranging between INR 3,760-5,800/t. The prices were on an ex-mines/FOR basis, inclusive of royalty, DMF, NMET, and additional premium charges.

- JSW Steel subsidiary Bhushan Power and Steel Ltd has started iron ore production at the Netrabandha Pahar (West) mine in Odisha, nearly nine years after winning the block in the 2017 auction at an 87.15% premium. Meanwhile, Rungta Mines Limited commenced production at the Chandiposi and Pureibahal mines from 20 April, with Apr’26 ROM output at 106,000 t and 16,400 t, respectively. The ramp-up of these au

Coal

- South African thermal coal prices at Indian ports remained under pressure despite firmer global cues and higher freight costs. Ex-Paradip RB2 (5,500 NAR) prices increased INR 350/t w-o-w to INR 11,350/t, while RB3 (4,800 NAR) prices rose INR 150/t to INR 9,800/t. However, buying activity stayed weak as demand remained subdued and port inventories increased to 15.87 mnt. Buyers resisted higher landed costs due to ample domestic coal availability and weak downstream steel margins, keeping trade activity largely requirement-based.

- India’s domestic non-coking coal prices remained largely stable w-o-w, with 5,000 GCV coal assessed around INR 6,000/t and 4,500 GCV material near INR 4,300/t. Frequent CIL auctions and comfortable supply conditions reduced urgency for spot purchases, while lower premiums in recent SECL and MCL auctions continued pressuring sentiment. However, logistics concerns and diesel shortages supported cautious seller expectations.

- Imported met coke sentiment stayed stable-to-firm during the week as Indonesian suppliers increased FOB offers following DGTR’s proposal to reduce anti-dumping duty. Three deals were reportedly concluded at $269-271/t FOB, while Indonesian-origin BF-grade coke prices increased $2/t w-o-w to around $302/t CFR India. Domestic BF coke prices remained stable at INR 36,400/t ex-Jajpur and INR 33,500/t ex-Gandhidham. Rising coking coal costs and stronger imported offers supported the market, although weak steel demand and cautious downstream buying limited aggressive price movement.

- Coking coal prices remained firm during the week amid tightening supply sentiment and higher vessel freights. BigMint’s PHCC index stayed stable w-o-w at $266/t CNF Paradip, while Australian PHCC prices increased $7/t to $240/t FOB Australia. Australia-India vessel freights also rose $2.1/dmtu w-o-w to $26.1/dmtu, supported by higher bunker prices and tight vessel availability. Market sentiment stayed supported on berthing delays in Australia, although mixed steel demand continued limiting aggressive procurement from Indian buyers.

Ferrous Scrap

- India’s imported containerised scrap market remained weak throughout the week as sharp INR depreciation and widening import parity continued to pressure buying sentiment. Buyers stayed cautious with the rupee nearing 96 against the dollar, while cheaper domestic scrap availability and lower-priced sponge iron further reduced import appetite.

- Offers for Europe-origin HMS 80:20 were largely heard at $360-375/t CFR, while shredded scrap offers remained elevated at $385/t CFR. However, workable buying levels stayed significantly lower at around $350-355/t CFR for HMS and $375-380/t CFR for shredded scrap, resulting in very limited fresh bookings. High freight costs from Australia and stronger US domestic scrap prices also restricted export competitiveness.

- Weak steel demand, monsoon concerns, and unfavorable currency conditions kept Indian buyers largely away from imports despite slight support from stronger Pakistan market prices.

Ferro alloys

- Silico Manganese:Indian silico manganese (60-14) prices continue to fall by INR 5,200/t ($54/t) w-o-w to INR 74,600-75,600/t ($778-789/t) across key markets. Prices continued to weaken amid low-priced bulk transactions in both the spot market and producer auctions. Subdued steel sector demand and expectations of further corrections kept buyers cautious, limiting fresh procurement activity.

- Meanwhile, HC 65-16 silico manganese export prices decreased by $7/t to $912/t FOB Vizag/Haldia.

- Ferro Manganese:Indian ferro manganese (70%) prices decreased w-o-w by INR 2,000/t ($21/t) to INR 77,900/t ($813/t) in Raipur and by INR 2,100/t ($22/t) to INR 77,900/t ($813/t) in Durgapur. Limited bulk enquiries and slow market activity pressured suppliers to lower offers to stimulate transactions.

- Meanwhile, export prices for the 75% grade fell by $10/t w-o-w to $900/t FOB Vizag/Haldia.

- Ferro Silicon:India ferro silicon (Si 70%) prices declined by INR 500/t ($5/t) w-o-w to INR 105,500/t ($1,100/t) ex-works Guwahati, while Bhutan prices fell by INR 900/t ($9/t) to INR 104,600/t ($1,091/t). Prices declined in both markets due to rising inventories, the commissioning of new production plants, and reduced demand from end-users.Additionally, bids were lower against Bhutan’s May offers, which, coupled with sufficient supply, ultimately pushed sellers to close deals at reduced prices.

- Ferro Chrome:India high-carbon ferro chrome (HC 60%, Si 4%) prices inched up by INR 400/t ($4/t) w-o-w to INR 119,000/t ($1,241/t) ex-works Jajpur. Prices inched up amid slight improvement in market inquiries for the material.Sellers largely maintained firm offers, which supported a slight increase in domestic ferro chrome prices. Market sentiment also remained positive due to the upward movement in stainless steel prices, providing additional support to the alloy market.

Semi Finished

- India-s semi-finished steel market witnessed moderate to sharp downside this week, with billet prices showing significant regional divergence, as per BigMint’s assessment. Prices declined by INR 400-1,500/t ($4-15/t) w-o-w, particularly in Gujarat and Chennai, where weakening finished steel demand, transport disruptions, and rising operational costs severely impacted market sentiment. Meanwhile, other regions witnessed a slight recovery during mid-week, supported by short-term bookings and market volatility.

- The sponge iron market reflected mixed trends during the week. Prices in the eastern and southern region declined by INR 200-1,200/t ($2-12/t) w-o-w, while the steepest correction was observed in Chennai, where weak demand and limited enquiries pressured spot prices. In contrast, key regions such as Raipur, Raigarh, and Bellary recorded a moderate recovery of INR 100-300/t ($1-3/t), supported by balanced supply and slight improvement in bookings.

- On the export front, Indian DRI offers witnessed a sharp decline amid weak overseas demand. Export offers to Nepal dropped by $11/t to $321/t CPT Raxaul, while offers to Bangladesh fell sharply by $17/t to $328/t CPT Benapole. Enquiries remained muted as global uncertainty continued to weigh on buying sentiment.

- SAIL-BSP concluded its 11 May’26 auction for 2,990 t of steel-grade pig iron, with the entire quantity booked at an average price realisation of INR 38,500/t exw. Bids declined by INR 600/t from the 22 Apr’26 auction, where 1,950 t were fully booked at INR 39,100/t, reflecting weaker market sentiment, cautious buying activity, and continued pressure from soft downstream demand.

- NMDC’s Nagarnar Steel Plant auctioned 10,000 t of steel-grade pig iron on 15 May’26, with the entire volume booked at an average price of INR 37,250/t. Bid prices declined by INR 750/t compared to the 12 May’26 auction, where 200 t was sold at INR 38,000/t. Despite the correction, full bookings indicate healthy demand sentiment and sustained buying interest in the market.

Finished long steel

- IF-rebar: IF rebar trade prices remained volatile with a downward trend across major markets this week. Market activity stayed subdued, with trading volumes remaining limited overall. Demand continued to weaken, particularly in the finished and semi-finished steel segments, as buyers focused only on immediate requirements and adopted a cautious purchasing approach.

- Booking activity remained muted for most of the week, with only one or two days showing comparatively better volumes, while the broader market sentiment stayed weak. Producers lowered offers and provided additional discounts to facilitate material movement, with mill inventories reported at approximately 8–12 days. In the near term, market participants expect price volatility to continue amid weak booking activity in the finished steel segment.

- On a week-on-week basis, rebar prices decreased by INR 400-1,500/t across key regions as per BigMint’s assessment.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 47,300-48,000/t exw Jalna , INR 43,300-43,700/t exw Raipur.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 45,600-46,000/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 44,200-44,800/t ex-Raipur.

- BF-rebar:Trade-level BF-rebar prices (distributor to dealer) by edged down by INR 1,500/t ($16/t) w-o-w to INR 57,500/t ($600/t) exy-Mumbai, as per BigMint’s assessment on 15 May 2026. Buying activity remained moderate across key regions, while northern markets witnessed relatively subdued demand.

Flat steel

- BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5–8 mm/CTL) remained stable w-o-w at INR 58,700/t as of 15 May 2026, unchanged from the previous week.

- Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 65,500/t, holding steady during the corresponding period last week.

- Trade-level HRC and CRC prices remained under pressure this week as buyers adopted a cautious, wait-and-watch approach, while softer offers from sellers in some markets further weighed on sentiment.

- India’s bulk imports of HRCs touched 111,117 t as on 8 May. Around 1,58,900 t of additional cargoes are expected by late-May.

- India’s bulk exports of HRCs touched 69,041 t as on 8 May. Around 68,420 t of additional cargoes are expected.

- Indian HRC export activity remained subdued this week, with shipments to Europe and the Middle East constrained by regulatory uncertainty, logistical disruptions, and persistent geopolitical tensions.

Leave a Reply