- NMDC auction witnesses poor participation

- Imported scrap trade muted despite competitive offers

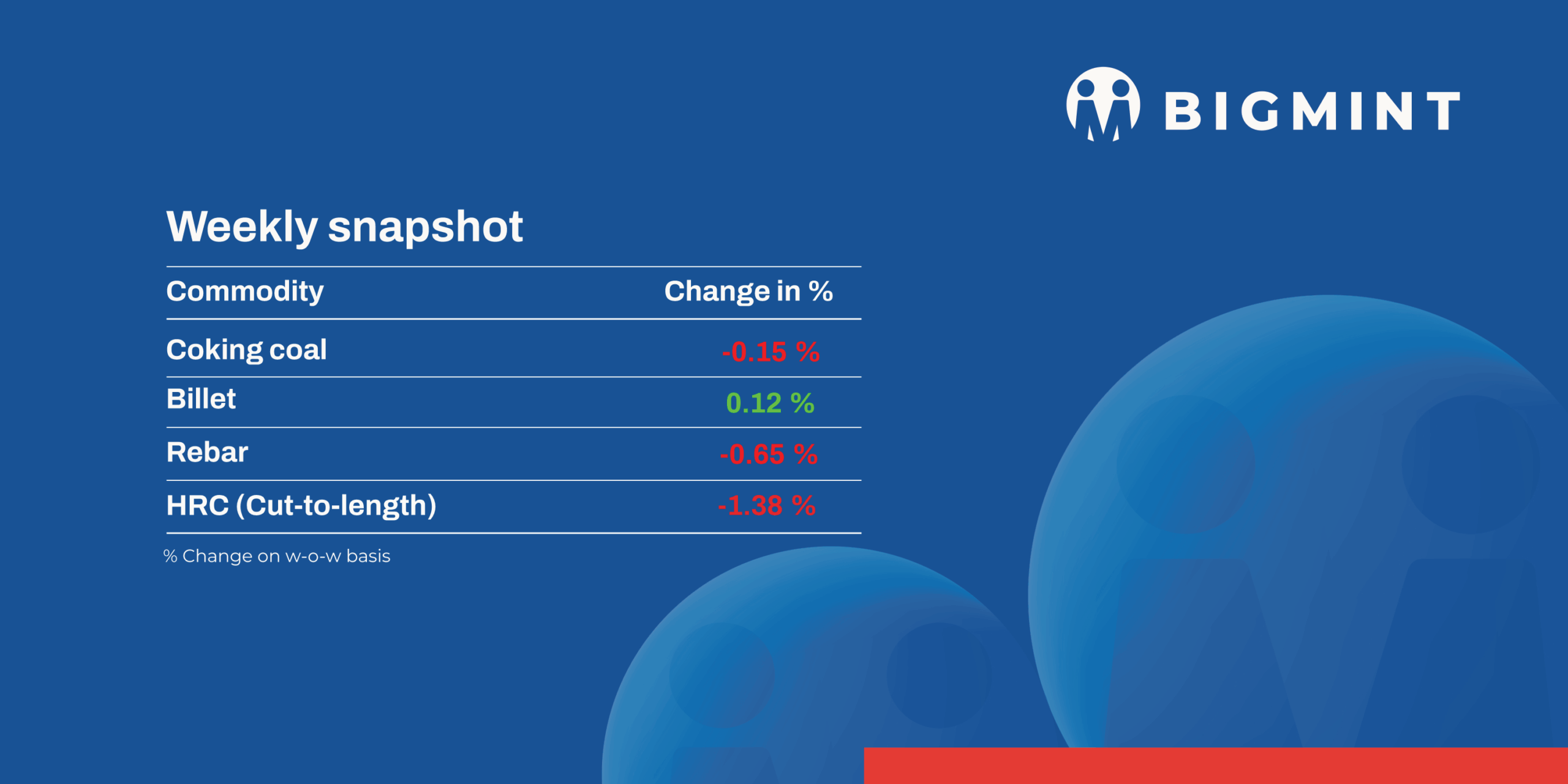

Domestic steel and raw material markets remained under pressure this week as weak construction activity, cautious procurement, soft export demand, and ample inventories weighed on prices of pellets, scrap, alloys, semi-finished, long, and flat steel segments.

Iron ore and pellet

- PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, fell by INR 350/t ($3.5/t) to INR 10,050/t ($106/t) DAP on Friday as compared to last week. Raipur-based producers reduced their offers for 62.5/63% (+/-0.5%) material by INR 300/t ($3/t) to INR 9,900-10,000/t ($104-105/t) exw recently. The downward revision follows persistent weakness in sponge iron and semi-finished steel prices, coupled with sluggish market sentiment and limited buying interest from downstream sectors.

- NMDC Chhattisgarh conducted an iron ore auction on 30 April, offering 375,600 t, of which only 47,300 t was sold. At Bacheli, 25,800 t of DR CLO (10–40 mm, Fe 67%) was booked at a premium of INR 1,550/t over the base price of INR 5,950/t, while 170,300 t of Fe 60% fines remained unsold. At Kirandul, 21,500 t of Fe 64% fines (FOR basis) was sold at the base price of INR 4,540/t, whereas 158,000 t of Fe 64% fines (FOT basis) did not receive bids. All prices are on a FOR/FOT basis and exclude royalty, DMF, and NMET charges.

- In Odisha auctions conducted this week, JSW Steel booked 39,500 t of CLO (5–18 mm, Fe 61–63%) at base prices of INR 6,900–7,900/t. SAIL sold 20,000 t of dump fines (Fe 60.4%) from Bolani mines at INR 4,560/t. In AMNS auction, around 24,000 t iron ore was booked, including 4,000 t of CLO (Fe 62.5%, 5–18 mm) at INR 7,225/t (base) and 20,000 t of low-TI CLO (Fe 58.58%, 10–40 mm) at INR 4,675/t against a base of INR 4,125/t.

Ferrous Scrap

- India imported scrap market remained largely subdued during the week, despite firm offer levels from global suppliers. HMS offers were mostly heard at $380-395/t CFR, while shredded ranged at $410-425/t, supported by tight scrap availability in the US and EU. However, workable levels stayed significantly lower, with buyers indicating around $375-380/t for HMS and close to $400/t for shredded, keeping trade activity limited. The lack of bulk arrivals at ports like Kandla and Chennai further highlighted weak import demand.

- At the same time, selective variations in offers were seen across origins, with Australia bulk HMS indicated lower at $360-365/t CFR (grab loading), UK/EU HMS at $370-390/t depending on impurity, and shredded around $395-415/t. Despite these relatively competitive offers, buyers remained cautious due to poor finished steel demand and weak margins, resulting in slow negotiations and minimal deal closures.

- The rupee weakening to INR 95/USD reduced import affordability, keeping buyers inactive and widening the bid-offer gap.

Ferro Alloys

- Silico manganese: Indian silico manganese (60-14) prices continue to fall by INR 2,275/t ($24/t) w-o-w to INR 78,200-78,600/t ($824-828/t) across key markets. Prices declined due to weak steel demand, sluggish exports, and surplus domestic supply, as reduced export opportunities diverted material into local markets, intensifying downward pressure across key hubs.

- Meanwhile, HC 65-16 silico manganese export prices decreased by $14/t to $923/t FOB Vizag/Haldia.

- Ferro manganese: Indian ferro manganese (70%) prices continue to fall w-o-w by INR 1,300/t ($14/t) to INR 81,700/t ($861/t) in Raipur and by INR 1,100/t ($12/t) to INR 81,700/t ($861/t) in Durgapur. Prices fell due to weak demand, need-based buying, ample supply, and limited trader activity, leading to continued downward pressure across key markets like Raipur and Durgapur. Meanwhile, export prices for the 75% grade dipped by $20/t w-o-w to $925/t FOB Vizag/Haldia.

- Ferro silicon: Indian ferro silicon (Si 70%) prices remained flat w-o-w at INR 107,500/t ($1,133/t) ex-works Guwahati, while Bhutan prices held steady at INR 107,500/t ($1,133/t), correcting slightly by INR 500/t ($5/t). Prices remained stable as underlying market fundamentals showed no significant change, with most participants staying on the sidelines in anticipation of May offers from Bhutan.

- Ferro chrome: Indian high-carbon ferro chrome (HC 60%, Si 4%) prices were at INR 118,000/t ($1,244/t), unchanged w-o-w ex-works Jajpur. Prices were supported by stable offers from sellers and routine trading activity. Additionally, Tsingshan has lifted its ferro chrome tender price by RMB 100/t ($15/t) m-o-m to RMB 8,495/t ($1,243/t) DAP, including taxes, for May’26 deliveries. The increase appears to be driven mainly by elevated chrome ore costs and firm producer offers, even as weak downstream demand and cautious market sentiment continue.

Semi Finished

- India’s semi-finished steel market witnessed mixed sentiment this week, with billet prices displaying regional divergence. As per BigMint’s assessment, prices declined by INR 200-800/t ($2-8/t) in the western and southern regions, while the central and eastern markets registered gains of INR 50-300/t ($0.5-3/t), supported by improved booking activity during the week. The uptick in central and eastern regions was supported by better bookings and demand, while the western and southern markets remained under pressure due to weak finished steel offtake.

- Sponge iron prices continued to decline across regions, falling by INR 100-1,000/t ($1-10/t) w-o-w. The sharpest correction was observed in Chennai, where muted demand and limited enquiries weighed on spot prices. In other key regions, prices softened moderately, as balanced supply and cautious buying behaviour prevented sharper corrections.

- On the export front, Indian DRI offers declined significantly, reflecting weak overseas demand. Offers to Nepal dropped by $9/t to $336/t CPT Raxaul, while Bangladesh-bound prices fell by $10/t to $345/t CPT Benapole. Limited enquiries and cautious buying sentiment in export markets led to limited activity, with transactions concluded at lower price levels.

Finished Long Steel

- IF-rebar: Induction Furnace (IF) rebar prices declined this week across most markets. At the start of the week, market sentiment was weak due to slow demand for finished steel, which kept trading activity subdued. However, by mid-week, some improvement was seen in the central and eastern regions, where buying activity picked up slightly. In other regions, purchases continued to remain largely need-based, with buyers showing caution.

- On the supply side, manufacturers faced pressure due to rising inventory levels, with stock levels averaging around 10-12 days. To manage this, many producers offered discounts to push sales, although a few tried to hold prices steady. Overall, the market remained under pressure, with limited demand recovery and cautious participation from buyers.

- W-o-w, rebar prices declined by INR 100-2,600/t, with the sharpest drop observed in the Jalna market.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 45,800-46,200/t exw Raipur, INR 48,700-49,300/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 47,700-48,000/t exw-Raipur.

- Trade reference prices of wire rod stood at INR 45,800-46,300/t ex-Raipur.

- BF-rebar: Trade-level BF-rebar prices (distributor to dealer) remained unchanged w-o-w at INR 59,700/t ($629/t) exy-Mumbai, as per BigMint’s assessment on 1 May. Buying interest remained weak this week in the trade channel, with buyers largely staying on the sidelines and restricting purchases to immediate requirements. Distribution channel participants reported comfortable inventory levels due to slower material offtake in recent days.

- Rebar project prices were workable in the range of INR 58,500-59,500/t ($617-627/t) on a landed basis, as per sources. Demand remained weak with limited inquiries as buying slowed. Election-related labour shortages disrupted construction activity, delaying procurement. Buyers adopted a cautious stance amid price volatility & uncertainty.

Flat steel

-

- BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) declined by INR 600/t ($7/t) w-o-w to INR 57,800/t ($609/t) as of 1 May, compared to INR 58,400/t ($616/t) on 24 April.

- Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 65,200/t ($688/t), marking a w-o-w decrease of INR 300/t ($3/t) from INR 65,500/t ($691/t) in the same period last week.

- Market sentiment stayed cautious this week. Buyers held back, while sellers lowered offers to move stocks. Transactions remained muted, with most participants adopting a wait-and-watch approach and avoiding fresh commitments.

- India’s bulk imports of HRCs touched 343,475 t as on 27 April. Around 103,840 t of additional cargoes are expected by mid-May.

- India’s bulk exports of HRCs touched 122,721 t on 27 April. Around 8,800 t of additional cargoes are expected.

- Indian HRC export activity remained subdued, with limited activity heard across key overseas markets, including the EU and the Middle East. While offers to Europe held steady on a w-o-w basis, the lack of concluded deals and the continued absence of offers to the Middle East reflect cautious sentiment among market participants.

Leave a Reply