- Portside Indonesian, South African thermal coal prices slide

- Domestic refiners raise pet coke prices sharply in Sep’25

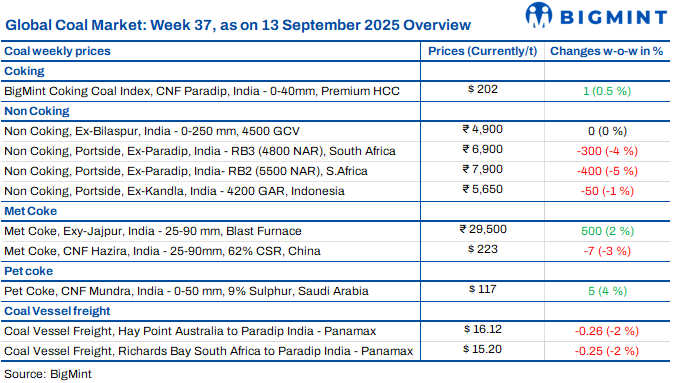

The Indian coal market remained cautious this week, with participants focusing on liquidating existing inventories ahead of the 22 September GST shift. Sellers trimmed offers to secure trades, while buyers delayed bookings in expectation of clarity on new pricing under the revised structure. Weak steel sector demand and rupee depreciation further weighed on sentiment. Internationally, South African coal was still high, but Indonesian offers softened, while fixtures were thin. Overall, the coal market is expected to stay subdued and volatile until the tax transition settles, and fresh trade direction emerges post-implementation.

Indonesian portside thermal coal prices ease w-o-w on pre-cess sell-off

Indonesian thermal coal prices at Indian ports slipped this week as traders rushed to clear stocks ahead of the cess removal on 22 September. BigMint assessed 5000 GAR at INR 6,950/t ex-Kandla and INR 6,850/t ex-Vizag, down INR 150/t w-o-w. Meanwhile, 4200 GAR eased INR 50/t and 3400 GAR dropped INR 200/t at Navlakhi. Rupee weakness and softer freights further weighed on market sentiment.

South African thermal coal prices slide as traders rush to liquidate

South African portside thermal coal prices are under heavy pressure this week as traders pushed to clear stocks before the 22 September GST change. At Vizag, RB2 slipped by INR 650/t to INR 7,750/t and RB3 fell INR 500/t to INR 6,800/t, while Gangavaram RB2 dropped INR 400/t to INR 7,900/t. Port inventories eased 7.1% w-o-w to 12.1 million tonnes (mnt). Export offers softened slightly, with RB2 at $71/t FOB and RB3 at $60/t. Sponge iron demand stayed muted, with BigMint’s C-DRI Rourkela index up by INR 150/t w-o-w to INR 26,200/t on 12 September. Market sentiment remains cautious until the GST transition passes.

Domestic thermal coal prices steady w-o-w as market stays cautious

Domestic thermal coal offers held flat this week, with buyers waiting for clarity on the GST changes due 22 September. BigMint assessed 5,000 GCV at INR 5,750/t ex-Bilaspur and 4,500 GCV at INR 4,900/t. Recent SECL auctions echoed the subdued sentiment, with bids largely unchanged and the bulk of volumes allocated to power-grade coal.

Portside US thermal coal prices rise on freight-led cost pressure

Portside US thermal coal prices in India edged up in early September, with offers assessed at INR 10,300/t exw, higher by INR 150/t w-o-w. The increase came as sellers adjusted pricing to cover freight and logistics costs, while steady demand lent support. Notably, no thermal coal imports from the US were recorded in August, as per BigMint data, underscoring reliance on existing portside supplies. Sellers maintained a firm stance, with logistics constraints adding to cost pressures in a thinly traded market.

Eastern India’s met coke market up; western India remains stable

India’s met coke market increased by INR 500/t in this week ending 13 September. BF-grade met coke was assessed at INR 29,500/t ex-Jajpur, while Gandhidham offers stayed at INR 30,000/t. Deals for around 20,000 t of met coke were concluded from eastern India at the same levels. Foundry-grade remained unchanged at INR 35,600/t ex-Rajkot.

Trading stayed cautious as buyers awaited clearer demand signals, despite seaborne coking coal inching up $2/t w-o-w to $187/t FOB Australia. Market activity stayed muted, with pig iron demand exerting pressure. However, auctions lined up earlier this week got postponed.

In the global market, China’s met coke market weakened after 8 September, with sharp rollbacks across Shandong, Luliang, and Tangshan, reflecting weak steel demand and margin stress.

Imported pet coke offers edge up w-o-w as freight costs climb up

Imported pet coke offers in India edged higher this week, supported by stronger freights. US-origin offers were assessed at $118-120/t CFR, marking a $4/t increase w-o-w, with freights on the US Gulf Coast to the west coast of India route rising by $5-7/t m-o-m to $51-53/t. Saudi-origin offers also tracked higher, assessed at $117-119/t CFR, nearly matching US-origin levels after a $5/t w-o-w rise.

Domestic refiners hike pet coke prices sharply in Sep’25

Indian refiners raised pet coke prices again in September, extending August’s firming trend, as Reliance remained absent from merchant supplies. IOC led the hikes, lifting Koyali and Panipat prices by INR 1,030/t, while Paradip and Haldia rose INR 730/t. BPCL followed with increases of INR 541/t at Bina and INR 657/t at Kochi, both constrained by reduced availability. MRPL revised prices uniformly higher by INR 530/t, while CPCL and Nayara each raised INR 560/t, with Nayara at INR 14,290/t, now up 9.4% y-o-y. Across refiners, hikes ranged between INR 530-1,030/t, driven by supply tightness and refinery-specific factors.

Coal freights under pressure as GST shift, weak demand curb fixtures

Coal shipping rates eased this week, as muted demand, high landed costs, and the looming GST revision weighed on trade. Supramax freights on the Indonesia-India routes fell $1.8/t w-o-w to $15.96/t, while Panamax rates on South Africa-India and Australia-India dropped slightly to $15.20/t and $16.12/t, respectively. Muted fixtures and limited fresh inquiries kept sentiment cautious, with sellers and traders focusing on stock liquidation ahead of the 22 September cess removal. Despite the Baltic index rising on stronger Panamax rates, overall coal freight activity stayed soft. Sources expect near-term freights to remain under pressure until post-GST clarity revives Indian imports.

Leave a Reply