- Indonesian thermal coal prices remain firm amid tight supply

- South African coal prices decline as buyers delay fresh purchases

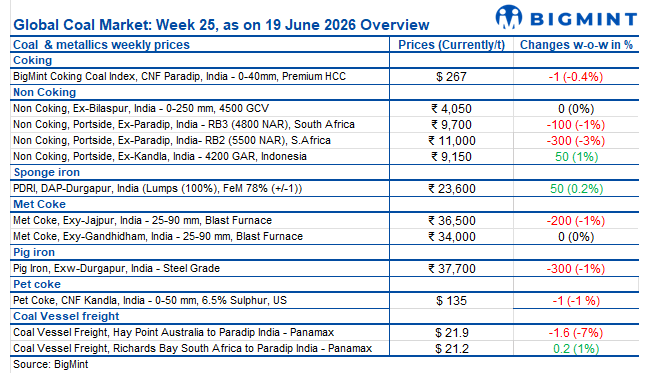

India’s coal market remained subdued during the week ended 19 June 2026, with buyers limiting purchases to immediate requirements amid comfortable inventories and the approaching monsoon season. Indonesian thermal coal prices stayed firm due to tight high-CV supply, while South African coal prices weakened as buyers awaited lower offers. Domestic non-coking coal prices remained stable despite weak e-auction participation. Meanwhile, falling petcoke prices reduced NAPP coal’s competitiveness in the cement sector, while imported met coke prices strengthened on firmer global fundamentals. Overall, cautious procurement behaviour and ample fuel availability continued to cap significant price movements across coal segments.

Indonesian thermal coal prices remain resilient despite weak spot demand

Indian portside prices of Indonesian-origin thermal coal remained largely stable during the week ended 19 June 2026, as limited availability of higher-calorific coal and firm supplier offers provided support despite subdued buying interest from end-users. The market remained balanced, with buyers adopting a cautious approach due to sufficient domestic coal availability and expectations of softer international prices.

5,000 GAR Indonesian coal prices remained steady w-o-w at around INR 11,000/t at Kandla and INR 10,900/t at Vizag. Meanwhile, 4,200 GAR coal increased marginally by around INR 50/t to approximately INR 9,150/t at Kandla and INR 9,050/t at Vizag, while 3,400 GAR coal remained stable at around INR 7,100/t at Navlakhi.

International thermal coal prices witnessed a marginal correction during the week, marking the first decline after an extended 11-week upward trend, as Indonesian benchmarks softened across grades.

South African coal prices decline as buyers delay fresh purchases

South African thermal coal sentiment weakened during the week ended 18 June as buyers remained cautious and waited for further price adjustments. Despite lower freight rates and easing geopolitical concerns, demand remained limited due to comfortable inventories and sufficient alternative fuel availability.

BigMint assessed RB2 (5,500 NAR) at INR 11,000/t ex-Paradip, down INR 50/t w-o-w, while RB3 (4,800 NAR) declined by INR 200/t to INR 9,700/t. At Vizag, RB2 prices fell to INR 10,800/t, while RB3 declined to INR 9,750/t. Portside coal inventories across major Indian ports declined by 5.7% w-o-w to 14.72 mnt, indicating improved evacuation activity. However, lower spot demand continued to weigh on supplier sentiment, with CNF Gangavaram RB2 assessed at $113/t, down $5/t w-o-w. Market participants reported vessel offers near $110/t, reflecting increasing pressure on sellers to remain competitive.

Domestic non-coking coal market stable amid weak auction participation

Domestic non-coking coal prices remained stable during the week, supported by sufficient availability and cautious buying behaviour. BigMint assessed 5,000 GCV coal at INR 5,500/t and 4,500 GCV coal at INR 4,050/t, both exw-Bilaspur. Eastern Coalfields Ltd (ECL) recorded limited participation in its 11 June e-auction, allocating only 106,400 t against nearly 0.8 mnt offered, resulting in an allocation ratio of just 13.3%.

The weak response highlighted subdued spot demand despite adequate supply availability. Lower-grade Rajmahal-origin coal dominated the auction basket, but buyers showed limited interest due to cautious procurement strategies and comfortable inventory positions.

BCCL-JSW steel deal marks milestone in coal washery monetisation

Bharat Coking Coal Limited (BCCL) transferred its 2 mnt/year Dugda Coal Washery to JSW Steel, marking India’s first coal washery monetisation initiative. The development represents a significant step towards improving coal beneficiation capacity, enhancing washed coal availability, and encouraging private participation in coal infrastructure. The initiative is expected to support better utilisation of existing assets while strengthening the supply chain for the steel industry.

NAPP coal faces pressure as falling petcoke prices shift cement sector economics

The Indian cement industry is reassessing fuel procurement strategies as declining petroleum coke prices reduce the cost advantage previously enjoyed by US Northern Appalachian (NAPP) coal. Earlier in 2026, high petcoke prices encouraged cement producers to increase NAPP coal usage.

However, the sharp correction in petcoke prices has changed the economics, with buyers now balancing petcoke, imported coal, and domestic fuel options. CFR India pet coke prices, which had reached around $160/t in early April, have corrected to the low-to-mid $130s/t range due to improved refinery availability, higher exports, and easing supply concerns.

NAPP and Illinois Basin (ILB) coal inventories at Kandla and Tuna increased to approximately 406,000 t, compared with 349,000 t a week earlier. Although weekly lifting improved to around 129,000 t, market participants indicated that consumption was largely driven by routine requirements rather than fresh buying interest. NAPP coal offers are currently reported around INR 13,500-14,000/t ex-works, but buyers remain reluctant to build additional inventories amid expectations of further softening.

Imported met coke prices strengthen while domestic market remains stable

India’s imported met coke market improved during the week ended 18 June, supported by firm international coke prices and rising raw material costs. Indonesian BF-grade met coke (65/63 CSR) increased by around $3/t w-o-w to approximately $318/t CFR India, reflecting stronger supplier offers.

In contrast, the domestic BF-grade met coke market remained stable due to comfortable availability and balanced demand-supply conditions. Eastern India prices declined slightly to INR 36,500/t ex-Jajpur, while western India remained steady at INR 34,000/t ex-Gandhidham. The divergence between imported and domestic markets highlights stronger global cost pressures, while domestic supply conditions continue to limit price increases.

Coal freight market shows mixed trends amid regional imbalances

India-bound coal freight markets remained mixed during the assessment week ended 19 June. The Panamax segment remained under pressure due to weak Pacific cargo activity and ample vessel availability. However, tighter tonnage availability and steady Atlantic demand provided some support. The Supramax segment remained relatively stable due to balanced Indian Ocean fundamentals despite slower Asian activity.

Outlook

The Indian coal market is entering a more balanced phase as buyers remain cautious ahead of the monsoon season. While supply constraints continue to support certain imported coal grades, weak spot demand and comfortable inventories are limiting price growth.

The Indian coal market is expected to remain largely stable in the coming week, with demand recovery dependent on industrial activity, power sector requirements, and global fuel price movements.

Leave a Reply