- Ample domestic coal supply pressures import demand

- Indonesian coal prices rise on tight supply, weak rupee

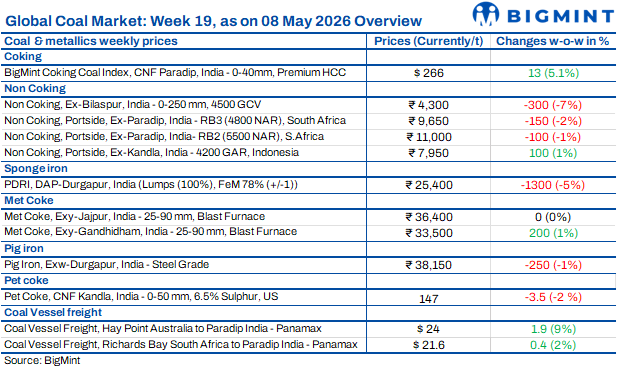

Indian coal market sentiment remained mixed during the week, with weak sponge iron and steel demand continuing to limit aggressive buying activity across imported coal segments. Domestic coal availability stayed comfortable, keeping pressure on South African and pet coke markets despite firm international cues and higher freight costs. However, portside Indonesian coal prices strengthened on tighter supply and currency pressure, while met coke remained stable amid firm import parity. Overall, buyers largely continued requirement-based procurement amid elevated inventories and uncertain downstream demand conditions.

Indonesian coal prices strengthen

Indian portside Indonesian thermal coal prices increased sharply w-o-w as of 8 May 2026 due to tight Indonesian cargo availability and rupee depreciation near INR 95/$, which raised import costs. Stronger Chinese buying also supported the market, with Indonesia’s coal exports to China rising 28.5% m-o-m to 5.8 mnt in April.

As per BigMint’s assessment, 5,000 GAR coal prices rose by around INR 200/t to INR 10,300/t at Kandla and INR 10,200/t at Vizag. Meanwhile, 4,200 GAR prices increased to INR 7,950/t and INR 7,850/t, respectively. Lower-grade 3,400 GAR coal gained around INR 350/t to INR 5,850/t at Navlakhi. However, India’s portside inventories increased 3.7% w-o-w to 15.14 mnt, limiting aggressive buying activity.

South African coal stays weak

South African thermal coal prices at Indian ports declined w-o-w as on 8 May 2026 amid weak demand and high inventories. As per BigMint’s assessment, ex-Paradip and ex-Vizag RB2 5,500 NAR dropped by INR 100/t to around INR 11,000/t, while RB3 4,800 NAR declined by INR 150/t to around INR 9,650/t.

India’s imports of South African non-coking coal declined sharply by 43.4% m-o-m to 1.97 mnt in April from 3.48 mnt in March. Meanwhile, PDRI DAP-Durgapur prices dropped by INR 1,300/t w-o-w to INR 25,400/t as on 8 May 2026, weakening coal demand further. India’s portside non-coking coal inventories also increased 3.7% w-o-w to 15.14 mnt, while cheaper domestic coal continued limiting imported coal buying interest.

Domestic coal prices decline

India’s domestic non-coking coal prices declined by around INR 250-300/t w-o-w amid lower premiums in recent SECL auctions and weak buying activity. As per assessments, 5,000 GCV coal prices dropped to around INR 6,000/t, while 4,500 GCV prices eased to nearly INR 4,300/t. Demand remained subdued due to weak sponge iron and steel market sentiment, with buyers continuing requirement-based procurement. Lower auction premiums and comfortable coal availability kept overall domestic coal prices under pressure.

US coal gains traction

US North Appalachian (NAPP) thermal coal strengthened its position in India’s cement sector as high petcoke prices pushed buyers towards cheaper fuel alternatives. US-origin petcoke offers were heard at $158-160/t CFR India in April, while 5,500 NAR thermal coal was available at $103-105/t CFR, making coal more economical. Petcoke imports declined sharply to 707,000 t in Q1CY’26 from 2.47 mnt a year earlier.

US NAPP coal offers were heard at $135-140/t CFR India, with some deals concluded near $135/t. More than 3.1 mnt of US coal is heading towards Indian ports by mid-June. Consequently, portside prices softened to INR 13,200-13,500/t ex-Kandla in early May amid rising arrivals and approaching monsoon-led demand slowdown.

US pet coke prices fall

US-origin imported pet coke prices in India declined w-o-w amid weak buying interest and cheaper coal availability. Pet Coke CNF Vizag 6.5% sulphur US fell by around $3/t to $152/t, while CNF Kandla declined by $3.5/t to $146.6/t.

As per BigMint’s assessment, US-origin 6,000 NAR thermal coal at Kandla stood around $125/t, making coal a cheaper alternative to imported pet coke. Confirmed Oman-origin tender deals were heard at $140-143/t, while unconfirmed Saudi-origin deals were near $140/t. US-origin offers also softened towards $145/t. Weak cement demand, comfortable coal availability, and approaching monsoon season kept sentiment subdued, with participants expecting further price corrections ahead.

BigMint’s coking coal index hits 3-month high

BigMint’s premium hard coking coal (PHCC) index was assessed at a three-month high of $266/t CNF Paradip, India, on 8 May 2026. The index rose by $13/t w-o-w amid long shipment delays and looming supply issues in Australia.

Met coke prices stay firm

India’s BF-grade metallurgical coke prices remained largely stable w-o-w as of 7 May 2026, supported by firm import parity and higher Indonesian offers. BF coke prices stayed at INR 36,400/t ex-Jajpur in the east, while western India prices increased marginally by INR 200/t to INR 33,500/t ex-Gandhidham. Foundry-grade coke prices remained stable at INR 36,400/t ex-Rajkot.

As per BigMint’s assessment, Indonesian-origin BF-grade coke increased by $9/t w-o-w to around $300/t CFR India. Meanwhile, Australian PHCC prices rose by $9/t to $240/t FOB Australia, supporting coke production costs. However, weaker downstream demand capped further gains, with pig iron prices in Durgapur declining by INR 250/t w-o-w to INR 38,150/t ex-works. Market participants expected met coke prices to remain stable amid cautious procurement and firm import costs.

Coal freights show mixed trends

Dry bulk coal freight to India showed mixed trends in the week ended 8 May. Panamax routes remained firm due to tight vessel availability and steady Australian coal enquiries, while Supramax freight stayed under pressure amid weak thermal coal cargo movement and ample vessel supply in Asia. Market sentiment remained cautious as charterers resisted higher freight ideas.

Bunker prices increased sharply by $48/t w-o-w to $827/t, adding cost pressure on freight markets. However, Brent crude futures declined by $10.03/bbl to $100.78/bbl. The Baltic Index increased by 348 points to 3,034, mainly supported by stronger Panamax activity, while the Supramax index slipped marginally. Market participants expect Panamax freight to stay supported in the near term, while Supramax routes are likely to remain weak.

Leave a Reply